Session 2009/2010

Sixth Report

Public Accounts Committee

Report on

Irish Sport

Horse

Genetic Testing Unit Ltd:

Transfer and Disposal of Assets

TOGETHER WITH THE MINUTES OF PROCEEDINGS OF THE COMMITTEE

RELATING TO THE REPORT AND THE MINUTES OF EVIDENCE

Ordered by The Public Accounts Committee to be printed 19 November 2009.

Report: NIA 25/09/10R Public Accounts Committee

REPORT EMBARGOED UNTIL 00.01 AM on Thursday 10 December 2009

This document is available in a range of alternative formats.

For more information please contact the

Northern Ireland Assembly, Printed Paper Office,

Parliament Buildings, Stormont, Belfast, BT4 3XX

Tel: 028 9052 1078

Membership and Powers

The Public Accounts Committee is a Standing Committee established in accordance with Standing Orders under Section 60(3) of the Northern Ireland Act 1998. It is the statutory function of the Public Accounts Committee to consider the accounts and reports of the Comptroller and Auditor General laid before the Assembly.

The Public Accounts Committee is appointed under Assembly Standing Order No. 56 of the Standing Orders for the Northern Ireland Assembly. It has the power to send for persons, papers and records and to report from time to time. Neither the Chairperson nor Deputy Chairperson of the Committee shall be a member of the same political party as the Minister of Finance and Personnel or of any junior minister appointed to the Department of Finance and Personnel.

The Committee has 11 members including a Chairperson and Deputy Chairperson and a quorum of 5.

The membership of the Committee since 9 May 2007 has been as follows:

Mr Paul Maskey*** (Chairperson) Mr Roy Beggs (Deputy Chairperson)

| Mr Patsy McGlone ** &****** | Ms Dawn Purvis |

| Mr Jonathan Craig | Mr David Hilditch ******* |

| Mr John Dallat | Mr Jim Shannon ***** |

| Mr Trevor Lunn | |

| Rt Hon Jeffrey Donaldson MP MLA ******** |

* Mr Mickey Brady replaced Mr Willie Clarke on 1 October 2007

* Mr Ian McCrea replaced Mr Mickey Brady on 21 January 2008

* Mr Jim Wells replaced Mr Ian McCrea on 26 May 2008

** Mr Thomas Burns replaced Mr Patsy McGlone on 4 March 2008

*** Mr Paul Maskey replaced Mr John O’Dowd on 20 May 2008

**** Mr George Robinson replaced Mr Simon Hamilton on 15 September 2008

***** Mr Jim Shannon replaced Mr David Hilditch on 15 September 2008

****** Mr Patsy McGlone replaced Mr Thomas Burns on 29 June 2009

******* Mr David Hilditch replaced Mr George Robinson on 18 September 2009

******** Rt Hon Jeffrey Donaldson MP replaced Mr Jim Wells on 18 September 2009

Table of Contents

List of abbreviations used in the Report

Report

Executive Summary

Summary of Recommendations

Introduction

The Value for Money of the Necarne Lease

The Disposal of Sport Horse Assets

The Handling of a Freedom of Information Request

Appendix 1:

Minutes of Proceedings

Appendix 2:

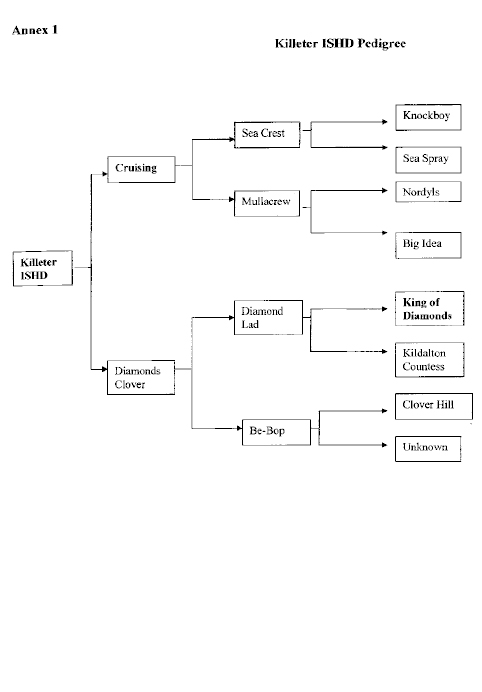

Minutes of Evidence

Appendix 3:

Correspondence

Appendix 4:

List of Witnesses

List of Abbreviations used in the Report

DARD Department of Agriculture and Rural Development

C&AG Comptroller and Auditor General

CAFRE College of Agriculture, Food and Rural Enterprise

FDC Fermanagh District Council

Sport Horse Irish Sport Horse Genetic Testing Unit Ltd

The Centre The Equine Reproductive Technology Centre

Executive Summary

Introduction

1. Irish Sport Horse Genetic Testing Unit Ltd (Sport Horse) was set up in 1996 to establish a commercially run elite horse-breeding project. The company received over £3.3 million in EU funding from the Department of Agriculture and Rural Development (DARD). Following DARD’s decision in April 2001 not to provide further funding to the project, Sport Horse was wound down in July of that year. Remaining assets were transferred to the Enniskillen campus of the Department’s College of Agriculture, Food and Rural Enterprise (CAFRE). These assets included an Equine Reproductive Technology Centre; 95 horses; and a stock of frozen equine semen.

2. The Committee has held two previous hearings on Sport Horse. The first, in January 2001, focused on serious conflicts of interest and weaknesses in project selection, financial management and accountability. The second hearing, in September 2001, raised concerns about the value for money of the 230-acre Ulster Lakeland Equestrian Centre at Necarne, near Irvinestown, held by DARD since 1998 on a 25-year lease from Fermanagh District Council; and the basis of a “gentlemen’s agreement" surrounding the sale of eight horses to the Irish Army.

3. Due to the suspension of the Assembly in October 2001, the Committee did not produce a report on its second hearing. However, in the wake of the C&AG’s 2008 report, which followed up a number of unresolved concerns from the second evidence session and reviewed the Department’s handling of the winding-up of Sport Horse, the Committee has taken the opportunity to finalise its work on this long-running case. While it is unusual for one project to be the subject of three evidence sessions, this reflects the Committee’s concerns about how a number of the issues had been dealt with, following the earlier sessions.

Overall Conclusions

4. The Committee recognises that the Sport Horse project presented a number of challenges by virtue of its innovative nature. However, it was not a particularly large project, nor was its administration inherently complex. It is disappointing to find, therefore, that a relatively small and short-lived project was so poorly handled, in so many respects. Moreover, most of the shortcomings were in areas where there were already well-established procedures for dealing with the types of issues that arose, but these appear to have been largely ignored.

5. While many of the failings in the project originated within Sport Horse itself, a large measure of responsibility must rest with the Department. As the provider of substantial public funds to the project, the Department was responsible for overseeing its operation. Unfortunately, in several key respects, the Department failed to ensure that the risks were properly managed. In addition, the Department’s own handling of some issues, particularly surrounding the Necarne Lease, give the Committee cause for concern.

6. The Committee acknowledges that the project did deliver a number of benefits to the equine industry and to the local economy of the Irvinestown area. However, these benefits were generally of short duration and fell far short of what had been envisaged when the project was launched. In the final analysis, therefore, the Committee must conclude that the Sport Horse project represented poor value for taxpayers’ money. There are a number of important lessons which the Department must take on board in its future handling of this type of development project. In that regard, the Committee welcomes the Accounting Officer’s assurances that similar projects would now be handled very differently by the Department.

Summary of Recommendations

Recommendation 1

1. The Committee recommends that the Department reviews its appraisal procedures to ensure that, when considering whether a leasehold arrangement would represent good value for money, it carries out a rigorous assessment of future needs and assesses the full cost involved, including both capital costs and operating expenses (see paragraph 10).

Recommendation 2

2. The Committee recommends that the Department ensures, in future, that any lease for land or property into which it enters includes arrangements for early termination and for some form of recompense with regard to any betterment which it has funded. The Committee further recommends that payments connected to such leases are made on a staged basis and that, if payments have to be made in advance, the period covered by each tranche should not normally exceed 12 months (paragraph 12).

Recommendation 3

3. The Committee is concerned that the failure to obtain planning permission and building control approval created unnecessary risks for personal safety and the safeguarding of publicly funded property. The Committee recommends that, where planning permission and building control approval is required for any project funded by the Department, this should be a condition of the Letter of Offer. Documentary evidence that these controls have been agreed with the relevant authority should be required before any funding is paid. (paragraph 18).

Recommendation 4

4. The Committee recommends that the Department reviews its procedures for the sale of publicly funded assets to ensure that both the current and future value of those assets are maximised for the benefit of the taxpayers (paragraph 23).

Recommendation 5

5. The Committee recommends that the Department reviews its procedures on the handling of Freedom of Information requests to ensure that its responses meet the spirit of the Nolan principles on openness. The Committee further recommends that details of the Sport Horse Freedom of Information case, together with the Committee’s views, are brought to the attention of all departmental staff involved in the Freedom of Information process (paragraph 28).

Introduction

1. The Public Accounts Committee met on 8 October 2009 to consider the Comptroller and Auditor General’s report on ‘Irish Sport Horse Genetic Testing Unit Ltd: Transfer and Disposal of Assets’ (NIA 10/08-09). The witnesses were:

- Dr Malcolm McKibbin, Accounting Officer, Department of Agriculture and Rural Development (DARD);

- Mr Roy McClenaghan, Deputy Secretary for Service Delivery, DARD;

- Mr John Fay, Director of the College of Agriculture, Food and Rural Enterprise (CAFRE);

- Mr Kieran Donnelly, Comptroller and Auditor General; and

- Ms Fiona Hamill, Deputy Treasury Officer of Accounts.

2. Irish Sport Horse Genetic Testing Unit Ltd (Sport Horse) was set up in 1996 to establish a commercially run elite horse-breeding project. The company received over £3.3 million in EU funding from DARD. Following DARD’s decision in April 2001 not to provide further funding for the project, Sport Horse was wound down in July of that year. Remaining assets were transferred to the Enniskillen campus of the Department’s College of Agriculture, Food and Rural Enterprise (CAFRE). These assets included an Equine Reproductive Technology Centre; 95 horses; and a stock of frozen equine semen.

3. The Committee has held two previous hearings on Sport Horse. The first, in January 2001, focused on serious conflicts of interest and weaknesses in project selection, financial management and accountability. The second hearing, in September 2001, raised concerns about the value for money of the 230-acre Ulster Lakeland Equestrian Centre at Necarne, near Irvinestown, held by DARD since 1998 on a 25-year lease from Fermanagh District Council; and the basis of a “gentlemen’s agreement" surrounding the sale of eight horses to the Irish Army. Due to the suspension of the Assembly in October 2001, the Committee did not produce a second report.

4. In taking evidence, the Committee focused on three key areas. These were:

- the value for money of the Necarne Lease

- the disposal of Sport Horse assets

- the handling of a Freedom of Information request.

The Value for Money of the Necarne Lease

5. The Ulster Lakeland Equestrian Centre at Necarne was developed by Fermanagh District Council (FDC) at a cost of some £4.5 million and opened in 1994. Sport Horse was based at Necarne from 1996. The Department also used Necarne to run part of its equine education provision. In May 1998, amid concerns that FDC intended to sell Necarne, DARD entered into a 25-year lease for the 230 acre site, for a lump-sum premium of £500,000. The lease requires the Department to facilitate major equestrian events at Necarne and to maintain and repair the site. In the six years to March 2007, the Department’s operating costs were some £200,000 per year. Projected operating costs to the end of the lease, in 2023, are a further £3 million.

6. In June 2006, a departmental review found that, because CAFRE’s equine provision was being delivered at two sites (the Enniskillen campus and Necarne), it was costing more than necessary. It recommended that all equine provision be located at Enniskillen. This was accepted by the Department in July 2006, subject to a full economic appraisal. The appraisal, completed in 2008, supported a move from Necarne. It concluded that the removal of equine provision to Enniskillen would involve capital costs of £750,000 to £900,000, but produce net savings of some £167,000 a year.

The Necarne Lease has not proved a “good deal" for DARD

7. In the September 2001 evidence session, the Department told the Committee that, prior to it taking on the Necarne lease, it had been paying FDC some £75,000 a year for students to use the facility. On this basis, it considered that securing a 25-year lease on Necarne for a total payment of £500,000 was “a good deal". In the most recent hearing, the Department added that the decision to lease the Necarne site in 1998 was linked to the expansion of equine education provision in Northern Ireland. It said that, at that time, FDC had been incurring losses in running the Necarne estate that it could not sustain. Had Necarne not been secured through the lease arrangement, thereby preventing its sale by FDC, the Department could not have continued its HND equine course or introduced a degree-level course. It also pointed out that Necarne became surplus to requirements because of a dramatic fall in agricultural course enrolments at Enniskillen campus, rather than a drop in demand for equine courses. It was the resultant freeing-up of capacity at Enniskillen that led to a reassessment of the need for Necarne.

8. The Committee notes from the C&AG’s report, however, that the fall in agricultural enrolments at Enniskillen began in 1998, the same year in which the Department acquired the Necarne lease. And although the Department said that the decrease in applications for agricultural courses at Enniskillen could not have been foreseen, it seems surprising that the Department was so poorly sighted as regards the demand for its courses. If, indeed, the demand for courses was as unpredictable as the Department suggests, this calls into question its judgement in taking on a 25-year lease for Necarne.

9. In the Committee’s opinion, the evidence strongly suggests that the decision to acquire the Necarne lease was poorly thought out. While the Department considered that the lease was a good deal, it does not appear to have taken into account the £200,000 annual operating costs, over and above the cost of the lease itself, in arriving at this conclusion.

Recommendation 1

10. The Committee recommends that the Department reviews its appraisal procedures to ensure that, when considering whether a leasehold arrangement would represent good value for money, it carries out a rigorous assessment of future needs and assesses the full cost involved, including both capital costs and operating expenses.

The terms of the Lease have severely disadvantaged DARD

11. The Committee was concerned to learn of fundamental flaws in the terms of the lease. First, the lease does not include a clause for early termination. Given the position in which the Department now finds itself, this seems particularly remiss of the Department and its legal advisers. Second, the lease does not provide for recompense (or any other form of financial allowance), to cover the cost of capital development works carried out at Necarne by Sport Horse and the Department, since 1998. This included the erection of three buildings, now valued at some £410,000, together with other capital upgrades costing around £250,000. All of this will transfer to FDC when the lease ends. The Committee is also disturbed to learn that the full cost of the lease (£500,000) had been paid by the Department in advance, to FDC. This was not only questionable in terms of appropriateness, but leaves the Department with little or no leverage in any future negotiations with FDC on early termination of the lease.

Recommendation 2

12. The Committee recommends that the Department ensures, in future, that any lease for land or property into which it enters includes arrangements for early termination and for some form of recompense with regard to any betterment which it has funded. The Committee further recommends that payments connected to such leases are made on a staged basis and that, if payments have to be made in advance, the period covered by each tranche should not normally exceed 12 months.

Necarne remains a drain on resources, and its future has yet to be resolved

13. Following the evidence session, the Department said that it had obtained the Minister’s approval to disengage from Necarne, subject to the necessary capital resources being available and the decision being aligned with the Department’s educational policy. The Department anticipates that, subject to agreement with FDC, it would surrender the leasehold in around March 2012. It will not be able to recover the unexpired portion of the lease (which in 2012 will amount to £220,000) and will have to ensure that the estate is transferred in an “appropriate condition".

14. The Committee finds the slow progress with which this matter has been pursued by the Department to be unacceptable. It is now more than three years since the departmental review highlighted that its equine provision was costing substantially more than necessary. Yet this situation appears set to pertain for, at least, a further three years, with public funds continuing to be wasted. This is most unsatisfactory. In these circumstances, the Committee requires the Department to bring this issue to a satisfactory conclusion with the minimum of delay.

The Disposal of Sport Horse Assets

The Equine Reproductive Technology Centre

15. The Equine Reproductive Technology Centre (the Centre) was constructed in 2000 at a cost of £160,000, but was never fully completed - it still requires fitting-out and painting. DARD attempted to lease the Centre in 2003, but found that it had been built without planning permission on registered historic parkland and without building control certification. Moreover, it had been constructed to agricultural, not commercial, standards. The Department obtained retrospective planning permission in May 2004 and a building control certificate in March 2005. However, leasing could not progress because additional capital investment is required to meet new environmental legislation and disability requirements.

16. The failure to obtain planning and building control approvals, and construction of the Centre to agricultural standard only, were serious breakdowns in control. While the Committee notes the Department’s comments that it had relied on the services of a senior building control officer from Fermanagh District Council to manage and supervise the construction work, the fact remains that the Department was still responsible for ensuring that its funding was being properly applied. Unfortunately, it failed to do so.

17. It is very disappointing that no benefit whatsoever has accrued from the provision of the Centre, since its construction in 2000. Scarce resources have, in effect, been wasted and an opportunity to help the Northern Ireland equine industry has been missed. In the Committee’s view, the Department must accept a large measure of the blame for this.

Recommendation 3

18. The Committee is concerned that the failure to obtain planning permission and building control approval created unnecessary risks for personal safety and the safeguarding of publicly funded property. The Committee recommends that, where planning permission and building control approval is required for any project funded by the Department, this should be a condition of the Letter of Offer. Documentary evidence that these controls have been agreed with the relevant authority should be required before any funding is paid.

The sale of eight horses to the Irish Army

19. In 2001, the Committee expressed concerns that the Irish Army Equitation School had “cherry-picked" eight of Sport Horse’s best animals for £15,000, prior to the company’s winding-up. The sale included a “gentlemen’s agreement" (rather than a formal contract) that the Irish Army would return the animals to Sport Horse for breeding, once they had retired from competition. However, only three of the eight were returned, all in 2004. Three others had died and the two remaining horses were retained by the Irish Army for breeding, following their retirement from competition. At the evidence session, the Department said that one of the two retained horses had since been euthanised.

20. The Accounting Officer told the Committee that the retention of the one remaining animal, named ‘Killeter’, was in line with the “gentlemen’s agreement", which he said stated that “when the horses’ competitive careers are complete, the Irish Army Equitation School will retain the mares for breeding". The Committee notes, however, that this is at odds both with the C&AG’s agreed report and the Department’s evidence to the Committee in 2001, each of which noted that the terms of the agreement were that the horses would be returned to Sport Horse for breeding, after retirement from competition.

21. Irrespective of which understanding is correct, the outcome is most unsatisfactory. Either the so-called gentlemen’s agreement has been breached, or the Irish Army has been allowed to retain the best horses for breeding (returning only poorer performing animals). The result, however, is the same - the interests of the Northern Ireland taxpayers who funded the project will not be recognised in the sale of any progeny of Killeter. The Committee recognises that breeding sport horses is high risk, with no certainty that an animal with a good show jumping record will produce a horse of great value. The point, however, is that Killeter was bred from very high quality bloodlines and so its progeny could turn out to be extremely valuable. This should have been recognised in the arrangements for the sale of the eight horses to the Irish Army.

22. The Department said that it cannot press for any compensation from the Irish Army, as no contract existed with Sport Horse. The Committee notes that, despite the failure of the Sport Horse Board to observe proper contract procedures in the sale of the eight horses, and the lack of value for money obtained from the sale, no action was taken against the directors of the company. This is very disappointing.

Recommendation 4

23. The Committee recommends that the Department reviews its procedures for the sale of publicly funded assets to ensure that both the current and future value of those assets are maximised for the benefit of the taxpayers.

The Handling of a

Freedom of Information Request

24. The Sport Horse assets transferred to the Department in 2001 included “straws" of frozen horse semen stored in liquid nitrogen tanks. Although the total purchase cost of the semen stocks (to Sport Horse), had been some £45,000, the value on transfer to DARD was “nil". The Department said this was because of uncertainties that had developed over the authenticity, quality and health status of the semen stock. In April 2006, staff discovered that there was no liquid nitrogen in one of the tanks and that the semen it contained was dead. An internal investigation by Enniskillen campus concluded that the loss of semen was due to “poor communications" – there had been no formal written procedures for the regular checking of liquid nitrogen in the tanks. The investigation also judged that there had been no negligence by any member of staff; instead, management accepted collective responsibility for the loss.

25. In November 2006, DARD received a Freedom of Information request from a journalist regarding the loss of semen stock. The information sought included:

- what stock of Sport Horse equine semen was currently held by the College and its value

- whether an internal enquiry had taken place into the loss of semen, the value of the loss and the reason

- whether anyone was held responsible for the loss, following the internal enquiry.

Parts of the Department’s response were inaccurate

26. In the Committee’s opinion, parts of the Department’s response were inaccurate.

On the value of the lost semen stock

(i) The Department’s response stated that the semen transferred from Sport Horse had “nil" value because its authenticity, viability and health status could not be verified. However, the Committee notes that the Audit Office found health certification, for a large proportion of the purchased semen, on Sport Horse files held by DARD;

(ii) The Department’s response also stated that the semen had been retained for educational purposes only, explaining that, under the ‘Horserace Betting Levy Board Code of Practice’, the semen transferred from Sport Horse could not be used on College or any other horses (because of the uncertainties about its health status). However, the Audit Office found that, in 2002, some of the semen had been used to inseminate three of the College’s mares, in order that the Department could “maximise the value of assets and avoid wasting the 2002 breeding season". Indeed, two of the three mares and their foals were subsequently sold. At the evidence session, the Department told the Committee that this action was entirely appropriate because the three mares were inseminated as part of an educational programme, they were the property of the Department and no third parties were involved. In the Committee’s view, however, the Department’s desire to maximise the value of its assets through the sale of the foals belies its contention that there was simply an educational purpose to its actions. Moreover, if the Department believed that the health status and authenticity of the semen could not be verified, the semen should never have been used, nor should the resulting progeny have been sold to third parties.

On how the loss occurred

(iii) The Department’s response to the information request stated that an internal review into the destruction of semen could not identify how the loss had occurred. This was clearly incorrect – the review had found that the loss was due to poor communications within the College;

On who was responsible for the loss

(iv) The Department responded that “no one individual member of staff could be held responsible for the loss". Given, however, that its internal investigation had found that management was collectively responsible, this response has the appearance of a rather disingenuous attempt to avoid any affirmation of responsibility.

27. In the Committee’s view, Freedom of Information responses ought to meet the spirit of the Nolan standards on ‘openness’, whereby “Holders of public office should be as open as possible about all the decisions and actions that they take. They should give reasons for their decisions and restrict information only when the wider public interest clearly demands". The Committee’s conclusion in this case is that the Department’s response fell short of the standard required.

Recommendation 5

28. The Committee recommends that the Department reviews its procedures on the handling of Freedom of Information requests to ensure that its responses meet the spirit of the Nolan principles on openness. The Committee further recommends that details of the Sport Horse Freedom of Information case, together with the Committee’s views, are brought to the attention of all departmental staff involved in the Freedom of Information process.

Appendix 1

Minutes of Proceedings of the Committee Relating to the Report

Minutes of Proceedings of the Committee Relating to the Report

Thursday, 1 October 2009

Room 144, Parliament Buildings

Present: Mr Roy Beggs (Deputy Chairperson) Mr John Dallat Rt Hon Jeffrey Donaldson MP MLA Mr David Hilditch Mr Trevor Lunn Mr Patsy McGlone Mr Mitchel McLaughlin Mr Jim Shannon

In Attendance: Ms Aoibhinn Treanor (Assembly Clerk) Mr Phil Pateman (Assistant Assembly Clerk) Miss Danielle Best (Clerical Supervisor) Mr Darren Weir (Clerical Officer)

Apologies: Mr Paul Maskey (Chairperson) Ms Dawn Purvis Mr Jonathan Craig

The meeting opened at 2.03 pm in public session.

5. Briefing on NIAO report ‘Irish Sport Horse Genetic Testing Unit Ltd: Transfer and Disposal of Assets’.

Mr Kieran Donnelly, C&AG, Mr Robert Hutcheson, Director; Jacqueline O’Brien, Audit Manager; and Mr Joe Campbell, Audit Manager; briefed the Committee on the report.

The witnesses answered a number of questions put by members.

[EXTRACT]

Thursday, 8 October 2009

The Senate Chamber, Parliament Buildings

Present: Mr Paul Maskey (Chairperson) Mr Roy Beggs (Deputy Chairperson) Mr Jonathan Craig Mr John Dallat Rt Hon Jeffrey Donaldson MP MLA Mr Trevor Lunn Mr Patsy McGlone Mr Mitchel McLaughlin Ms Dawn Purvis Mr Jim Shannon

In Attendance: Ms Aoibhinn Treanor (Assembly Clerk) Mr Phil Pateman (Assistant Assembly Clerk) Miss Danielle Best (Clerical Supervisor) Mr Darren Weir (Clerical Officer)

Apologies: Mr David Hilditch

The meeting opened at 2.01 pm in public session.

4. Evidence on NIAO report ‘Irish Sport Horse Genetic Testing Ltd: Transfer and Disposal of Assets’.

The Committee took oral evidence on the above report from:

Dr Malcolm McKibbin, Accounting Officer, Department of Agriculture and Rural Development; and supporting officials Mr Roy Clenaghan and Mr John Fay.

The witnesses answered a number of questions put by the Committee.

Members requested that the witnesses should provide additional information to the Clerk on some issues raised as a result of the evidence session.

[EXTRACT]

Thursday, 15 October 2009 Room 144, Parliament Buildings

Present: Mr Paul Maskey (Chairperson) Mr Roy Beggs (Deputy Chairperson) Mr John Dallat Rt Hon Jeffrey Donaldson MP MLA Mr David Hilditch Mr Trevor Lunn Mr Patsy McGlone Mr Mitchel McLaughlin Mr Jim Shannon

In Attendance: Ms Aoibhinn Treanor (Assembly Clerk) Mr Phil Pateman (Assistant Assembly Clerk) Miss Danielle Best (Clerical Supervisor) Mr Darren Weir (Clerical Officer)

Apologies: Mr Jonathan Craig Ms Dawn Purvis

The meeting opened at 2.03 pm in public session.

6. Issues Paper on evidence session on NIAO report ‘Irish Sport Horse Genetic Testing Unit Ltd: Transfer and Disposal of Assets’.

Members considered an issues paper on this evidence session.

[EXTRACT]

Thursday, 19 November 2009 Room 144, Parliament Buildings

Present: Mr Paul Maskey (Chairperson) Mr Roy Beggs (Deputy Chairperson) Mr Jonathan Craig Mr John Dallat Rt Hon Jeffrey Donaldson MP MLA Mr David Hilditch Mr Trevor Lunn Mr Patsy McGlone Mr Mitchel McLaughlin Ms Dawn Purvis Mr Jim Shannon

In Attendance: Ms Aoibhinn Treanor (Assembly Clerk) Mr Phil Pateman (Assistant Assembly Clerk) Miss Danielle Best (Clerical Supervisor) Mr Darren Weir (Clerical Officer)

Apologies: None

The meeting opened at 2:02 pm in public session.

7. Consideration of the Draft Committee Report on ‘Irish Sport Horse Genetic Testing Ltd: Transfer and Disposal of Assets’.

Paragraphs 1 – 7 read and agreed.

Paragraph 8 read, amended and agreed.

Paragraphs 9 – 17 read and agreed.

Paragraph 18 read, amended and agreed.

4:20 pm Mr Hilditch left the meeting

4:20 pm Mr Donaldson entered the meeting

4:24 pm Mr Beggs entered the meeting

4:29 pm Mr Hilditch entered the meeting

Paragraphs 19 – 25 read and agreed.

Paragraph 26 read, amended and agreed.

Paragraphs 27 – 28 read and agreed.

Consideration of the Executive Summary

Paragraphs 1 – 6 read and agreed.

Agreed: Members ordered the report to be printed.

Agreed: Members agreed that the report would be embargoed until 00.01 am on Thursday,

10 December 2009.

Agreed: Members agreed to launch the report with a press release to be agreed at a later meeting.

[EXTRACT]

Appendix 2

Minutes of Evidence

8 October 2009

Members present for all or part of the proceedings: Mr Paul Maskey (Chairperson) Mr Roy Beggs (Deputy Chairperson) Mr Jonathan Craig Mr John Dallat Mr Jeffrey Donaldson Ms Dawn Purvis Mr Jim Shannon

Witnesses:

Mr John Fay Mr Roy McClenaghan Dr Malcolm McKibbin |

Department of Agriculture and Rural Development |

Also in Attendance:

Mr Kieran Donnelly |

Comptroller and Auditor General |

|

Ms Fiona Hamill |

Deputy Treasury Officer of Accounts |

1. The Chairperson (Mr P Maskey): We will now hear evidence on the 2008 Audit Office report ‘Irish Sport Horse Genetic Testing Unit Ltd: Transfer and Disposal of Assets’.

2. We are joined by Dr Malcolm McKibbin. You are very welcome, Dr McKibbin. I see that you are in a bit of pain today, so hopefully the evidence session will not last too long. However, Committee members have some questions for you, on which we will need detail. I will hand over to Dr McKibbin to introduce his team.

3. Dr Malcolm McKibbin (Department of Agriculture and Rural Development): With me is Roy McClenaghan, who is the deputy secretary in the Department’s service delivery group, and John Fay, director of the College of Agriculture, Food and Rural Enterprise (CAFRE). We thank the Committee for the opportunity to give evidence to it.

4. The Committee will be aware that this is quite an unusual session, as it is the third time that the Department of Agriculture and Rural Development (DARD) has given evidence to this Committee on this very challenging, innovative, high-risk and, ultimately, problematic project. The Sport Horse company was established in 1996, and it went into liquidation in 2001. The Committee will be aware from evidence given in Committee previously, the last time as far back as September 2001, and in subsequent correspondence, that problems were identified and acknowledged as having existed at the time.

5. I was encouraged to learn, after discussions with the new Comptroller and Auditor General — I formally congratulate Mr Donnelly on his appointment — that we would be focusing today primarily on the content of the 2008 report. For that I am grateful, because we should be trying to deal with the few outstanding issues, in order to move forward and improve future control.

6. From my perspective, Chairperson, thank you very much for making arrangements to make it slightly easier for me to get in and out of the Building. I appreciate the sympathy and understanding, which, I trust, will continue for the next hour, or for however long we are here.

7. The Chairperson: We are sometimes caring. I appreciate your saying that this is the third time that DARD has appeared before the Committee on the same subject. That is unfortunate, because if some issues had been addressed, you would not be in front of us today. You and some of your departmental colleagues need to ask yourselves why you are here for a third time.

8. Paragraph 2.11 of the Audit Office report, ‘Irish Sport Horse Genetic testing Unit Ltd: Transfer and Disposal of Assets’, which was published in September 2008, says that the Department told the then Comptroller and Auditor General that work was well advanced on the economic appraisal, which was considering the Department’s options for equine education. Has that appraisal been completed, and if so, what were the results?

9. Dr McKibbin: The appraisal was completed in mid-2008 in DARD. It went through our economic and policy branch, which approved it in autumn 2008, and the Department of Finance and Personnel (DFP) approved it in March 2009. The report concluded that it would be best if DARD removed itself from the Necarne estate and relocated its equestrian education services to the Enniskillen campus. Capital costs of between £750,000 and £900,000 would be associated with that move. The move would produce net resource savings of around £167,000 per annum.

10. The Department has obviously had to liaise with Fermanagh District Council, and any such move would depend on an agreement with the council. The state of play is that the Department’s top management group has considered the issue in the light of the economic appraisal, and it will shortly make a recommendation to our Minister. Should that answer be in the affirmative, we would, in conjunction with Fermanagh District Council, surrender the leasehold, probably in March 2012. We would have to pass the estate across in its existing state, with DARD responsible for maintaining the assets that are there up to that date. At that stage, we would also be removing horses to the value of probably £60,000.

11. Again, if the answer to move were yes, we would also give the council permission to market the Necarne estate. Those would be the general conditions attached to a move. A condition report would also have to be undertaken in order to ensure than any asset that we transferred to the council was in the appropriate condition. I stress, however, that any decision is subject to our Minister’s approval, and it will depend on the necessary capital resources being available and on any policy decision’s being coincidental to or aligned with our education policy.

12. The Chairperson: Is there a timescale for that recommendation going to the Minister?

13. Dr McKibbin: Within a matter of weeks — it may well go this month.

14. The Chairperson: If there is a specific timescale, the Committee may, as on the previous occasion, ask for more information and the outcome of the recommendation before we complete our report. Will the Department provide the Committee with that information in writing?

15. Dr McKibbin: Absolutely. That is not a problem.

16. The Chairperson: OK. Paragraph 2.4 states that the Department is paying more than £200,000 every year for the Necarne site, and you have given us some details about that. Do you think that the Necarne site represents value for money for the taxpayer?

17. Dr McKibbin: We should ask ourselves why we took out the lease in the first place, but I do not know whether you want to venture into that territory now. We are spending £200,000 a year at present. If we relocate to the Enniskillen campus, the economic appraisal indicates that we will save £166,700 a year, which would reduce the costs that the Department incurs.

18. The Chairperson: Without going into great detail, I take it that £200,000 a year was not and is not value for taxpayers’ money?

19. Dr McKibbin: We have to go back to when the decision was made. In 1995, we began to offer an HND course for the equine industry in conjunction with Fermanagh District Council. We wanted to introduce a degree course, but we could not do that without the ability to use the Necarne site. The council had spent £4·5 million on a top-class equestrian facility at Necarne. Pages 5 and 24 of the Northern Ireland Audit Office (NIAO) report give an impression of the quality of the estate.

20. We did not have any budgetary provision to locate in a different facility. Press reports, and internal correspondence that I read, made it clear that Fermanagh District Council was incurring losses that it could not sustain. If we were to continue our education provision, we were going to have to invest in Necarne. The then Valuation and Lands Agency (VLA) concluded that the 25-year lease, at a cost of £500,000, represented reasonable value for money. When the decision was made, it was thought to have been a reasonable one. Indeed, in 2005, a review of the equine industry identified a need for more skilled and more qualified staff to meet the industry’s needs, and concluded that the number of students should be increased. In order to continue to provide an equine education service, we were going to have to invest somewhere. Around that time, the VLA concluded that the £500,000 lease over 25 years, with an annual nominal rent of £1, was reasonable value for money.

21. Mr Craig: I listened to that with some interest. You told us about the reasoning behind your entering into a 25-year lease of the equestrian centre, but you made a strange statement when you said that you thought that £500,000 a year represented value for money. Perhaps you can outline why you think that that was value for money and why you think that the Department did not get it wrong when it entered into a 25-year lease.

22. Dr McKibbin: What I said was that the Valuation and Lands Agency concluded that it was value for money. It was the expert in determining what should be an appropriate rent, not me. We believed that it was a good deal because there was a commitment to continue with equine education. If we had not invested in Necarne and had entered into the lease agreement, we would not have been able to continue with the HND course, nor would we have been able to commence the degree course. For the past four years, on average, 130 students a year have been involved in equine education. There is quite a demand; it is a significant industry in its own right. We believed that, in order to continue to provide equine education services, it was an appropriate lease to enter into.

23. Mr Craig: Did the Department not have any concerns that it may have been signing a lease that was too long?

24. Dr McKibbin: The question over the future of Necarne did not arise because of the difficulties in providing equine services. It arose because of the significant and dramatic decrease in the number of agricultural students applying to the college. In 2004-05, fewer than 10 students applied for the course on agricultural studies at Enniskillen, and, therefore, no agricultural course was run. That freed up additional capacity, which allowed the need for Necarne to be reassessed. If your question is whether such a decrease in applications by agricultural students was foreseen, the answer is no.

25. It has been acknowledged at previous Public Accounts Committee (PAC) meetings and in correspondence that a clause should have been written into the agreement to allow for better conditions should a change in circumstances require an early termination of the contract. Undoubtedly, there was an oversight by DARD and the Departmental Solicitor’s Office (DSO), as was acknowledged at each of the previous PAC meetings and in subsequent correspondence. I agree that it was a flaw not to have such a provision in the contract.

26. Mr Craig: Two obvious questions arise from that. You openly admitted that a clause should have been included in the contract, and, to me, that would have been common sense, but that is in short supply everywhere. Is it now the Department’s policy that, when entering into any such negotiations in future, a get-out clause will be included in the lease? I am also slightly puzzled that the entire lease of £500,000 was paid up front? Should that payment not have been made in stages?

27. Dr McKibbin: In answer to your first question, clauses to deal with early termination of a contract and to address what would happen over time with capital investment into land, for instance, will be included in future.

28. I cannot answer your question on why it was agreed to pay £500,000 up front and a nominal £1 yearly rent. That was the result of the negotiations at the time between DARD and Fermanagh District Council. The lease was signed in 1998, and I do not have the answer to your question, nor do I believe that I would easily be able to get it.

29. Mr Craig: It occurred to me that the chief executive of Fermanagh District Council deserved a huge bonus for what happened, because, frankly, he wiped your eye.

30. Another glaringly obvious question arises: why was a clause not built into the lease whereby, ultimately, there would be some clawback of any investment that you made in the site? As it stands, and as is outlined in paragraph 2.2 of the report, it seems that the Department will not be able to claim back any money for the new sheds that you erected, which were valued at more than £400,000, or for other upgrades to the value of £250,000?

31. Dr McKibbin: Irish Sport Horse Developments (ISHD) erected the sheds, not the Department.

32. I return to your point about the Department’s getting its eye wiped, as you so eloquently put it. From the information that was available at the time, the VLA considered the deal to be reasonable. At that stage, no one predicted the huge downturn in the number of agricultural students applying to campuses throughout Northern Ireland.

33. Hindsight is wonderful, but we should look back at decisions that were made in 1998 and assess the information that people had at their fingertips when they made those decisions. I accept the criticism: there should have been, as you pointed out, Mr Craig, a clause in the contract to deal with capital investment over that period and, indeed, to deal with early termination.

34. Mr Craig: You mentioned, rightly, that some buildings were not erected by the Department. Given that the Department was involved in the process, how closely did it keep an eye on events at the centre? Paragraphs 3.5 to 3.8 explain that much of the construction was on registered parkland and that the Department had to apply for retrospective planning permission because it did not bother to apply in the first place. The less that is said about that, the better. It is unbelievable that that happened on land that was leased to the Department.

35. Dr McKibbin: When ISHD was constructing the centre, it utilised the services of the senior building control officer on Fermanagh District Council to manage and supervise the project. At the time, the Department assumed that that individual’s involvement in the project would provide sufficient assurance of compliance with planning permission and building control. As it transpired, that was a false assumption, and we had to rectify the situation subsequently.

36. Mr Craig: That brings me back to the statement that I made earlier about the council.

37. Anyway, I have no further questions.

38. Mr Shannon: It is nice to see you again, particularly Roy, whom I have not seen for a long time. I hope that we are not too hard on you. A rumour is going around that we will take your stick away, Malcolm, if you do not answer the questions correctly. You need to be dead careful. [Laughter.]

39. I want to discuss paragraph 3.11. “Gentlemen’s agreement" is a loose term at the best of times. The Public Accounts Committee is concerned that the Irish Army had cherry-picked eight of Sport Horse’s best horses. The nature of the term “cherry-picked" means that they took the best horses. The Irish Army did that shortly before Sport Horse was wound up. However, the Committee is concerned that, contrary to the gentleman’s agreement, not all the horses were later returned to the Department, as had been agreed. The appendices to the report show that very clearly. The Irish Army retained the two most successful horses in competition for breeding. Did that not breach the gentlemen’s agreement? Moreover, why did you allow that to happen? Ultimately, we, as a Committee and as elected representatives, have a responsibility to the taxpayer and to our constituents. Did they lose out as a result?

40. Dr McKibbin: Those are fair questions. As an accounting officer, I would have wanted and expected a formal contract between ISHD and the Irish Army. That point has been acknowledged during previous PAC evidence sessions and in correspondence. I fully accept that public bodies should not do business on the basis of gentleman’s agreements. Having said that, it would be helpful to highlight a couple of points.

41. Since the start of the project in 1996, Irish Sport Horse tried to evolve a collaborative arrangement with the Irish Army equitation school. It has an international reputation as Ireland’s premier showjumping organisation. However, DARD did not permit the subsequent sale of the eight horses on the basis of a gentleman’s agreement. The company had the right to dispose of the assets, excluding tangible fixed assets, at its own discretion and in the normal course of trading under the memorandum and articles of understanding that it had. Indeed, DARD did not know how the valuation of the eight horses was reached. The Irish Sport Horse development board and the Irish Army arrived at the valuation between them.

42. Moreover, throughout the process, ISHD maintained that it had a firm understanding with the Irish Army that the animals would be returned once the Irish Army equitation school no longer required them. You point out correctly that there was no formally signed contract; however, a draft contract and a letter from ISHD support that belief. Discussions with and letters from the commanding officer of the Irish Army did not dispute ISHD’s view and indicated the Irish Army’s willingness to work with ISHD or its successor organisation.

43. A letter written by the Irish Department of Defence to the Department of Agriculture and Rural Development on 4 April 2003 stated:

“the School remains willing to co-operate with any official disciplined breeding programme in Northern Ireland, overseen by the Northern Ireland Authorities, and dedicated to the production of quality sport horses for the benefit of all Irish breeders. Such co-operation could include return of mares for breeding once their competitive careers are finished, irrespective of what stage that might be".

44. In other words, in some cases the mares might be quite young, if, for example, they were injured. The Department of Defence went on to offer additional services, such as semen from Irish Army stallions, as well as advice. That is what the letter said on the agreement.

45. The Committee asks whether the Irish Army equitation school lived up to that gentleman’s agreement. Of the eight horses originally sold to it for £15,000, three were returned. Two were sold by DARD for £6,770, and a further animal, valued at £2,000, was retained. At the time when the Northern Ireland Audit Office report before us was published, three of the remaining horses had died: two as a result of injuries in competition and one from colic. That left two out of the original eight, and at the time of the report, both were involved in competition. Since then, one of those horses has had to be euthanised, so one remains.

46. Therefore, as Mr Shannon said earlier, the Irish Army still has one horse. However, that is in line with the gentleman’s agreement of 2000, which stated:

“When their competitive career is complete, the Army Equitation School will retain the mares for breeding. However, should the Army Equitation School not wish to retain all the mares they will be returned to ISHD or Enniskillen College of Agriculture for breeding purposes subject to the agreement of both parties."

47. At our previous appearance before the PAC, Mr McClenaghan explained the very high attrition rate and the great risk involved in dealing with these animals.

48. What else did the Irish Army do? More than the eight animals mentioned were involved — it also donated four further horses to DARD. Two of those were sold for a total of £3,500 and the two others retain a value of £4,500. That means that we have sold, returned or received donated horses from the Irish Army for over £10,000, and we own others valued at over £6,500. That makes a total of £16,700, which is more than the £15,000 that the Irish Army paid us or ISHD originally. In addition, the Irish Army has also transferred two young horses produced under the donor mares scheme, offered semen from Irish Army stallions, and provided advice and support to breeders in Northern Ireland who ask for it.

49. Although I absolutely agree that there should have been a formalised agreement, I cannot look at the agreement and say that DARD or ISHD was short-changed. They got the services outlined in the gentleman’s agreement and more.

50. Mr Shannon: Appendix 7, on page 44 of the report, lists the horses and their status at 2008. Look at the two horses that the Irish Army retained for breeding. I am not an expert on horses, but I have many friends who are. They have fed information on this matter through to me.

51. Are you aware of the background of the horse Killeter? I believe that the correct terminology in the horsey world is “bloodline". Diamonds Clover was the dam for Killeter. Are you aware of that?

52. Dr McKibbin: You are right to pick that horse out, because it is the only one that the Irish Army retains. I am not an expert in horses, nor did I hurt my back falling off one. Horses that enter competitions are graded from A to E. I think that Killeter reached the top of grade C, and that would have allowed it to compete nationally. Killeter, therefore, was the best performing of the horses that went to the Irish Army.

53. However, I do not have any information on the breeding lines.

54. Mr Shannon: This line of questioning is important. I am not saying that Dr McKibbin is trying to avoid answering; however, if he checks, he will find that the dam, Diamonds Clover, is from the same bloodline as King of Diamonds and Clover Hill. If that fact is confirmed, the value of Killeter far outweighs the £10,000 that came from the Irish Army. Are you aware of the status of Killeter’s sire, Cruising?

55. Dr McKibbin: No, I do not have bloodline details with me.

56. Mr Shannon: I make the point because Cruising made the Irish Olympic team. Consequently, every horse to come from Killeter will be top of the tree in the horsey world, so it must be looked on as being much better and more valuable, and the Irish Army has retained it for breeding purposes in order to further that bloodline. Did we, therefore, get value for money for the people whom we represent? I do not believe that we did, because Killeter’s bloodline clearly indicates that its progeny should be highly valuable.

57. Dr McKibbin: Cruising was also Clogher’s sire, and it was returned to the Department and sold for just over £5,000. We have talked about the high risk that is associated with sports horses, and we have seen that at least four of the eight horses have since died. It is a high-risk business, and there is no certainty that a good showjumping lineage will produce a horse of great value.

58. Mr Shannon: Everyone in the horsey world will tell you that they are working towards getting that one great horse. Indeed, today, a very good friend of mine is at the Horse of the Year Show and, if his horse does well, he will probably retire from the butchery business. That is how it works.

59. Nonetheless, when Diamonds Clover is put with Cruising to produce Killeter, you have something special that is above everything else on the list in appendix 7. I shall not labour the point, but does the Department have any arrangements in place to obtain a share of the value of any progeny that come from the two horse retained by the Irish Army according to appendix 7? Am I right to believe that Killeter is now the only horse that is retained by the Irish Army?

60. Dr McKibbin: I shall ask John Fay to answer your questions about the horses, because he knows a great deal more about the animals than I do.

61. Mr John Fay (Department of Agriculture and Rural Development): It is notoriously difficult to breed a very good horse, even given a good dam line and a good sire line. For anatomical reasons, a horse may turn out to be neither a good showjumper nor a good racehorse. That is a characteristic of both the thoroughbred and non-thoroughbred sides of equine breeding. People have endeavoured to change that, and the initial purpose of the project was to bring together the good sire and dam lines using the best reproductive technology that was available at the time. Those technologies included artificial insemination and embryo transfer —where embryos from, for example, a combination of Cruising and a high genetic-merit mare were taken and disseminated throughout the equine industry.

62. However, as Dr McKibbin said, very few of those horses, particularly in the showjumping world, make it to the top. Very few horses make the grade from the thousands of horses that are bred; therefore, it really is a chance meeting if a dam and a sire do so successfully. However, I acknowledge what Mr Shannon said about the need to breed good dam and sire lines.

63. Mr Shannon: It is not really a chance meeting, because those horses are produced artificially. Man puts them together. The chances are different, the probabilities outweigh the possibilities, and I do not believe that the project provided good value for money.

64. Did the Department press for compensation, or was it not able to do so because the information was unavailable? Chairman, can the Committee pursue the matter further at this stage?

65. Dr McKibbin: As I said, the Department does not have a contract: no contract was drawn up between ISHD and the Irish Army. There was an unwritten agreement, and, as yet, the Department does not know whether Killeter will be returned. Currently, it is being used for breeding in the South, and, to repeat what I said, the highest level that it reached was the top of group C from a banding of A to E.

66. Mr Shannon: Yes, but it was the best horse that was produced, and that is the point that I am trying to make. The value of Killeter is much greater than any of the other seven horses.

67. Paragraph 3.21 of the report deals with the Department’s response to a freedom of information (FOI) request. We are all aware that, when a question is asked or information sought under the Freedom of Information Act 2000, all the information must be made available. However, I was disturbed by the fact that paragraph 3.21 — the Department’s FOI response — records the fact that the Department carried out an internal review but could not establish how the loss of semen occurred, yet paragraph 3.15 of the report states:

“the semen was lost as a result of poor communications."

68. How could the Department not explain how that semen was lost yet later decide that it was as a result of “poor communications"? The Department should have disclosed all the information under FOI rather than try to hide it.

69. Dr McKibbin: The FOI request that was put to the Department asked it to detail whether anyone had been found to be responsible, and the answer given was that no one was held responsible.

70. The Department believes that the response that it gave provided the information that was requested of it, and that it has satisfied its obligations under the Freedom of Information Act. Indeed, on receipt of the NIAO comments, the Department asked a senior departmental officer, who was specifically trained in FOI, to review that matter, and he also concurred that the Department had complied with the provisions of the Act.

71. Furthermore, the journalist who requested the FOI release did not ask for a formal review of the information that was released, and he was able to use the information that he received from the Department to produce his newspaper article. If he had been dissatisfied with that information, he could have complained to the Information Commissioner under section 50 of the Act, rather than whistle-blow to the NIAO.

72. Moreover, although the NIAO has suggested that the response was incomplete, because other information that was available to the Department that was not released would have been relevant or helpful, that goes beyond the adequacy issue associated with FOI requests. Indeed, it moves into the more complex area of how helpful someone should be in responding to an FOI request.

73. We frequently face difficult dilemmas. I do not want my staff going into the business of second-guessing a correspondent’s motives or acquirements by providing information that they thought that the correspondent may have wanted but did not request. The information request was from a professional journalist who, I imagine, had experience in submitting FOI requests and knew that if he was dissatisfied, there was an appeal mechanism for him to go through. However, I believe that our reply satisfied the specific terms of the question.

74. We do find the situation difficult at times, Mr Shannon. When someone asks a question, and other pieces of information are available, do we or do we not supply that information? We tend to try to give a direct answer to the question that was asked and deal with supplementaries as they come to us.

75. Mr Shannon: The freedom of information request in paragraph 3.21 states:

“the semen cannot be used on College or any other horses."

In its freedom of information response, the Department said that the semen had been retained by the college for educational purposes only. However, in 2002, it was used to impregnate three mares at the college. Did the Department’s response misrepresent that position?

76. Mr Fay: No, I do not believe that our response misrepresented the position. In 2002, the College of Agriculture, Food and Rural Enterprise used the semen to inseminate three mares as part of an educational programme. At that stage, the mares were the Department’s property. There were no third parties involved. I believe that it was entirely appropriate to use the semen from ISHD on those mares as part and parcel of an educational programme.

77. When the Horserace Betting Levy Board code of practice was published in 2006, we realised that there were increased biosecurity risks with that semen, and we have not used any of it in any college horses since then. It has never been used outside of that, and it certainly has no commercial value. That is why, when it was initially transferred to the Department, it was not allowed to be used on a recommendation from the liquidator.

78. Mr Shannon: Your freedom of information response at paragraph 3.21 states:

“Under the Horserace Betting Levy Board [HBLB] Code of Practice, the semen cannot be used on College or any other horses."

Does that not mean that, by using it on three college mares in 2002, that code of practice was contravened? You said that it was used for educational purposes, but did that contravene the code of practice?

79. Mr Fay: Yes, but that code of practice was only published in 2006. It did not exist in 2002 when the mares were inseminated. Those guidelines were not available to us at that time.

80. Mr Dallat: Initially the project did a great deal for Irvinestown. I remember being there: it attracted the good and the great, including members of the Royal Family, and Secretaries of State strutting around. If the project had been done properly, it might have been a real investment in Irvinestown. At the end of day, do you agree that the people who were responsible for this and who have never been unmasked did the people of Irvinestown a terrible disservice and hurt the whole concept of rural development? Has the Department addressed that situation?

81. Dr McKibbin: One must consider what the project achieved against what its original objectives were. The original objectives were set out in the economic appraisal of 1996, and the company was formed in 1997. Undoubtedly in that economic appraisal, some of the assumptions on the cost of the processes were wrong and the ultimate demand for services was overestimated. The PAC concluded at a previous evidence session that ISHD had met its objectives only partially, but it contributed towards the peace and reconciliation fund.

82. Mr Dallat: Surely the first thing that anybody who is designing an arena for horses should find out what is the international size for such an arena. The arena in Necarne was three metres short of that. Do you agree that that was one of the reasons that it could not meet its objectives? Despite three inquiries, we never got to the bottom of who did that awful disservice to the people of Irvinestown and practically ruined the whole concept of rural development at a time when the area was coming out of 30 years of conflict and desperately in need of economic regeneration, and when rural development was essential. We get caught up in discussing the horses, their names, and all that stuff. However, the people who really suffered, the businesspeople of Irvinestown in particular, have never had answers. The people involved just walked away.

83. Dr McKibbin: The first thing to appreciate is that the arena that you are referring to was not built as part of this project. I am fully aware of the issues around the arena, but it was not built as part of the project that I am here to give evidence on today.

84. On the question of the project’s key outputs, it is a mistake to imply that the project did not deliver anything.

85. Mr Dallat: Of course.

86. Dr McKibbin: The project quite clearly did not achieve all its objectives, but it did produce around 150 superior foals that were born and went into the industry. There was a breeders’ association forum with around 50 members that helped to reduce the fragmentation of the industry. There were 70 local people trained to a much higher level of expertise than ever before; two veterinarians were qualified to a much higher level of expertise in embryo transfer techniques; and 150 individuals availed themselves of the equine technology centre facilities. There was a substantial contribution to the educational programme at Enniskillen College of Agriculture. All the activities were cross-border-based and the project employed seven people locally and, through contracts with contract rearers, put a significant amount of money into the local economy. Although the project did not achieve all the objectives that it should have achieved, those outputs were of benefit not only to the people of Irvinestown but to the industry and to that area of Fermanagh.

87. Mr Dallat: My case could not be made better. If the project had been properly planned and designed, had met the international standards and had had any degree of supervision, it is possible that Irvinestown might have a state-of-the-art equestrian centre today. Do you agree that your Department played a dreadful role in the demise of the whole project?

88. Mr McClenaghan: With respect, the indoor arena of a smaller size to which you are referring was built by Fermanagh District Council, which received up to £4·5 million for the project. DARD was not involved in that.

89. Mr Dallat: Who was co-ordinating the whole project?

90. Mr McClenaghan: DARD was not co-ordinating that bit.

91. Mr Dallat: That is like talking about a leisure centre with no swimming pool. I am sorry, but I feel sore about this.

92. Dr McKibbin: Mr Dallat is clearly concerned. What we are trying to say is that DARD, for which Mr McClenaghan was working at the time, was not involved in the project that delivered the indoor arena that is causing Mr Dallat such concern.

93. The Chairperson: I think that — [Inaudible.]

94. Mr Dallat: Totally.

95. Mr Beggs: Can you clarify the nature of the gentleman’s agreement with the Irish Army? Was it said that the horses would be returned if they were not used for breeding by the Irish Army?

96. Dr McKibbin: Yes; after the horses had finished competing, and if they were not being used for breeding, it was expected that they would be returned.

97. Mr Beggs: Essentially, the agreement was that the Irish Army could keep and breed the successful horses and the centre would take back the unsuccessful ones and pay for their long-term retirement, perhaps, in grazing costs. It strikes me as being a lose-lose agreement — the centre lost the good horses and the bad ones came back to it.

98. Dr McKibbin: First, the horses that came back to us were either sold or used for educational purposes. As I said, DARD got £6,770 for the first two that were returned to us and then sold, and a further £3,500 for two others that were sold. There was clearly a benefit to DARD from that. The only horse that the Irish Army retains is the one that Mr Shannon has referred to already.

99. Mr Beggs: The Irish Army holds the only one that has any significant value.

100. Mr Shannon: That is the point that I am making.

101. Mr Beggs: Another point is worth pursuing. If a local community group received assets from Peace II funding and then had to wind up, there are procedures in place that dictate how it would have to properly dispose of those assets, which would be of much smaller value than the very expensive horses about which we are talking. Have you assessed whether proper procedures were followed by the directors of the ISHD when it disposed of those assets? If they were not, have any of the then directors been held liable for the disposal of public assets?

102. Dr McKibbin: In April 2001, when the decision was made to no longer fund ISHD, its board decided to adopt the recommended route of going into voluntary liquidation, which would involve a managed disengagement. PricewaterhouseCoopers helped us with that process and stated that, on the subject of value for money, a managed disengagement, and a retention and subsequent disposal of strategic assets would alleviate concerns over value for money in respect of European and national funds. The process also ensures that out-turns can be safeguarded and, subject to consultation with the industry, that the Department is able to exercise its duty of care.

103. The assessment of assets and liabilities indicated that the assets marginally exceeded the liabilities. After the assets were transferred across, the Department stated that it had to make sure that those assets were disposed of in such a way that taxpayers’ interests were protected and the benefits of the project were not lost. There were two groups of assets of value and one that was not of value, which I have no doubt we will come back to later. There were 95 horses, 61 of which were either offered to contract breeders or sold, after independent valuation, on the market. Of the remaining 34, DARD retained five. The remainder were either offered to contract breeders or were sold at market value. The disposal of the horses was dealt with in the best interests of the taxpayer and so that those who wished to stay involved in the project had the opportunity to do so.

104. The second issue was around the centre itself. The preferred option that arose out of the disposal of assets plan was a leasing of the centre. For a variety of reasons, which, no doubt, will be highlighted, the centre was never leased. The third asset, which was valued at £0, was the semen. PricewaterhouseCoopers made an assessment of the plan to dispose of the assets and concluded that it was the best option for value for money. It also came to the conclusion that the plan complied with the obligations that DARD had given to the Public Accounts Committee in previous evidence sessions and correspondence.

105. The disposal issue was also approved by the Department of Finance and Personnel, which, although not having to do so, gave the opinion that the managed disengagement and the disposal of assets was best value for money. A great deal of effort was put into trying to get that part of the process right, if that assuages some of the Committee’s concerns.

106. Mr Beggs: I understand that effort was put in, but the public purse pays the lease agreement and the maintenance costs of the building. The limited funds in the Northern Ireland block grant continue to pay for those assets. It was not a break-even situation, because we still had to pay money from Executive funds to maintain those buildings.

107. Has the Department examined whether the disposal of those assets, which were publicly owned property in Northern Ireland, was properly dealt with? The most valuable horses were cherry-picked by the Irish Army, which was given permission to breed whichever horses it chose. Those very expensive assets and the future breeding prospects of successful horses were passed on to the Irish Army.

108. Has the Department assessed whether the directors of Sport Horse carried out their duty as members of a public body to represent the public’s interest? Did they carry out the disposal appropriately, and if not, has the Department pursued them for failure to carry out their duties as directors, bearing in mind that one of those directors was, I understand, in the Irish Army?

109. Dr McKibbin: That is correct. One of them was in the Irish Army, yes. There are two issues: first, after 3 July 2001, all assets were transferred to the Department. We believe that every effort was made or is being made to dispose of those assets in a manner that will secure value for money to the taxpayer. Secondly, at previous meetings and in correspondence, the Public Accounts Committee acknowledged that there were flaws in the way in which those assets were disposed of or purchased by the board of Sport Horse before 3 July 2001.

110. As I said earlier, the board had the authority under the memorandum and articles of understanding to dispose of assets. We would have wished to have seen a contractual written agreement with the Irish Army, but that did not exist.

111. Mr Beggs: My very first point was that a small community group cannot dispose of its laptop computer in anyway that it chooses; rather, it must follow appropriate procedures. My very specific question was: did the then directors of Sport Horse dispose of those assets in an appropriate manner, and if not, has the Department considered pursuing them?

112. Dr McKibbin: The conclusion of the Committee and the Department was that the assets were not disposed of by following the best procurement or disposal practices. Has any of the directors been pursued for culpability or liability? The answer is no. At the end of the last PAC session on the issue in September 2001, the issue of whether there was any suspicion of any of the directors having carried out fraud was raised. The Committee and the Department concluded that there was not.

113. Mr Beggs: Yet public assets have been lost. No doubt those directors have some sort of public liability insurance that should have been tapped into.

114. Dr McKibbin: Without going back over the history, at that time that the board made the point — indeed, the point was made at some of the evidence sessions — that, although best practice procurement and disposal procedures were not always followed, it did not always mean that value for money was not obtained. I am just saying that that is a —

115. Mr Beggs: Do you think that value for money was obtained when there was cherry-picking of the horses by the Irish Army?

116. Dr McKibbin: First, I have never used the word “cherry-picking". I am not aware of how particular animals were selected exactly, so I cannot answer that question honestly.

117. Mr Beggs: I will rest on that point.

118. The Chairperson: I suppose that much of the confusion came down to the gentleman’s agreement. It is hard to believe, in this day and age, that something like that even exists.

119. Dr McKibbin: I do not think that that will happen again.

120. The Chairperson: I will take that as an assurance. Have gentleman’s agreements been used by anyone else in DARD? You said that that should not happen again, and I agree.

121. Dr McKibbin: I am certainly not aware of it. The procedures are quite clear: if we arrange to dispose of or purchase assets, proper contract documentation or formal agreements should be put in place.

122. The Chairperson: It is astonishing that that happened.

123. The Committee may put some more questions to you in writing; however, you will be glad to hear that those are all questions that we have for you today. You mentioned that you might not be able to find the information relating to the payment in advance for the lease that Mr Craig asked for. If you find that information, please send it to the Committee, as it will be useful. On behalf of the Committee, I thank John, Roy and Malcolm for attending today’s session.

124. Mr Shannon: Before you go, will you confirm the situation with the dam and sire for Killeter? That will clearly illustrate our point that the Irish Army held on to the horse that was worth the most money. It kept the one horse that had the ability to donate semen to create progeny worth around £500,000.

125. The Chairperson: The Committee will ask for that information in writing. Once again, thanks for coming today.

Appendix 3

Correspondence

Chairperson’s Letter of 12 October 2009 to Dr Malcolm McKibbin

![]()

Public Accounts Committee

Dr Malcolm McKibbin Accounting Officer Department of Agriculture and Rural Development Dundonald House Upper Newtownards Road Belfast BT4 3SB |

Room 371 Parliament Buildings Belfast BT4 3XX Tel: (028) 9052 1208 Fax: (028) 9052 0366 E: pac.committee@niassembly.gov.uk 12 October 2009 |

Dear Malcolm,

Evidence Session on Irish Sport Horse Genetic Testing Ltd: Transfer and Disposal of Assets

Thank you for attending the evidence session on Irish Sport Horse Genetic Testing Ltd.

As agreed the Committee would be grateful if you could provide the following information:

1. An indication of when the recommendation proposed by the Department to the Minister of Agriculture and Rural Development concerning the surrender of the leasehold of the Necarne Estate to Fermanagh District Council will be considered by the Minister.

2. The outcome of the Minister’s decision on this recommendation once it has been considered.

3. An explanation from the Department detailing why, upon negotiating the lease on the Necarne Estate it was agreed to pay the total cost of £500,000 in one lump sum as opposed to integrated amounts being paid throughout the life of the lease.

4. Confirmation of the pedigree/blood line of Killeter and a valuation of the horse based upon its parentage.

I should appreciate your response by 5 November 2009.

I am also copying this letter to David Thomson, Treasury Officer of Accounts, for his information.

Yours sincerely,

![]() Paul Maskey

Paul Maskey

Chairperson Public Accounts Committee

Correspondence of 28 October 2009 from Dr Malcolm McKibbin

Appendix 4

List of Witnesses Who Gave Oral Evidence to the Committee

List of Witnesses Who Gave Oral Evidence to the Committee