Research and Library Services

Background Briefing SNP Proposal for Scottish Local Income Tax

-

As part of their agenda to create “a wealthier and fairer Scotland 1 ”, the Scottish National Party (SNP) has set out proposals for replacing council tax (and council tax benefit) with a local income tax;

-

The idea behind this is to introduce a regime which is based intrinsically on ability to pay.

-

The local income tax (LIT) would apply at the starting, basic and higher rates, to all taxable income except savings income, and would be capped at 3%;

-

The SNP would continue to levy a property tax on second and empty homes.

-

They are also proposing a ‘freeze’ on council tax rates in the short term, to avoid interim increases.

Financial Implications:

- Council tax in Scotland is forecasted to raise £2,131 million in 2006-07, of which around £45 million comes from second and/or empty homes. Council tax benefit is forecasted to cost £381 million;

- The Institute of Fiscal Studies (IFS) has estimated that, if the LIT were in place in 2006-07 and was set at its maximum level by all local authorities, it would raise around £1,250 million 2;

- The reform would therefore constitute (at best) a £450 million tax cut and leave a corresponding revenue shortfall 3;

- The SNP argue that this £450 million reduction in local authority spending could be absorbed with no loss of quality in public services, if councils make efficiency savings of 1½% p.a. for 3 years. However, precedent suggests this could be difficult, particularly since this would be in addition to any efficiency savings already implied for the UK 4.

Net Income Implications:

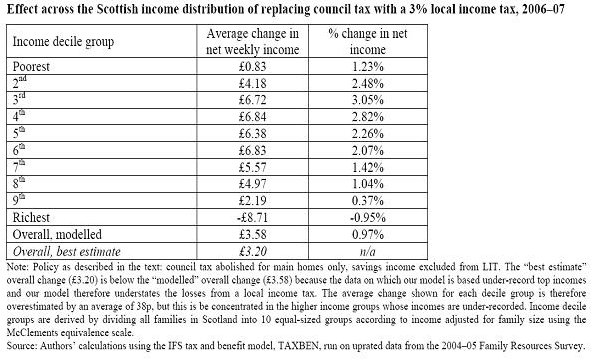

The table below quantifies the estimated average effects upon net income, by income decile group (individuals are categorised into ten groups on the basis of income levels – 1 is the Poorest, 10 is the Richest).

Source: Institute for Fiscal Studies, March 2007

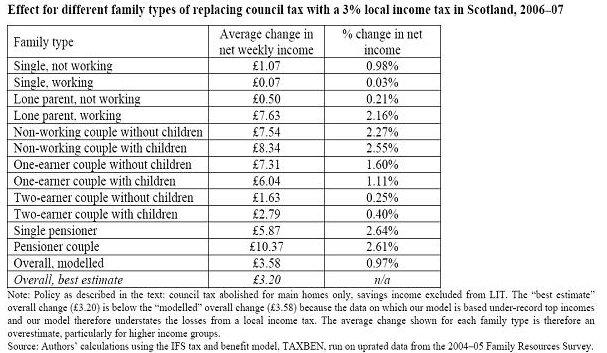

- One of the potential shortcomings of a local income tax is that families (with multiple-earners) could be comparatively worse off. The next table quantifies net income effects, by ‘family type’:

Source: Institute for Fiscal Studies, March 2007

Some Criticisms of Proposed LIT

-

The exclusion of savings income

The proposed LIT has been criticised on the basis that savings income is excluded, and the implications of this for “fairness”. For example, a wealthy, retired investor who earns dividend income would not be required to contribute under this system. However, savings income is excluded due to the enormous administrative costs which would be associated with charging investment income 5.

-

Would reduce the importance of local government

It is argued that local authorities’ reduced ability to raise revenue would constitute a significant reduction in the importance of local government within Scotland. Levels of local spending would be almost entirely determined by the level of grant received from the Scottish Executive, since local authorities would lose the ability to increase local taxes to fund expenditure. There are concerns that this could result in the accountability and efficiency of local government being undermined 6.

-

Burden on Employers

The proposed LIT could represent a considerable additional administrative burden on local employers.

-

Effect on families

As mentioned above, it is argued that families consisting of multiple incomes would be comparatively worse-off under a LIT.

-

High Earners may leave Scotland

It is argued that the introduction of a LIT would result in the economy suffering the flight of high earners. High earners are typically highly mobile; they often have more control over their terms and locations of work. They are also adept at arranging their tax affairs to maximum advantage.

-

Large companies may relocate

Large UK companies with a presence on both sides of the border may recruit senior staff to offices outside Scotland if this tax is imposed. This argument implies that the tax could damage the economy doubly – by driving wealth creators away and diverting business to other parts of the UK.

-

Implications for Housing Market

The current system of council tax provides some incentive to live in relatively smaller (low-value) properties. This alleviates some degree of pressure on the local housing market. This effect would be removed by the proposed LIT 7.