Research and Library Services

Northern Ireland Assembly

Research Paper |

September 2007 |

Inquiry into Credit Union Regulation, Services, Funding and Recommendations

Aidan Stennett

This briefing paper outlines aspects of the regulation and functioning of Credit Unions in the UK and Ireland. It focuses on a comparison of regulation, services to members and funding availability between GB, Northern Ireland and the Republic of Ireland

Library Research Papers are compiled for the benefit of Members of the Assembly and their personal staff. Authors are available to discuss the contents of these papers with Members and their staff and can be contacted through 9052 1227 but cannot advise members of the public.

September 2007

Summary of Key Points

- Credit Unions have a long and successful history in Northern Ireland. The first credit union in the UK was founded by John Hume in Londonderry in 1960. There are approximately 170 credit unions in Northern Ireland with membership levels equivalent to more than one quarter of the population

- The success of credit unions in Northern Ireland has been attributed to their promotion by established community groups and religious organisations and their 'by the community for all the community’ ethos.

- Credit unions in Northern Ireland are governed by one primary piece and four subordinate pieces of legislation. They are regulated by the Registry of Companies, Credit Unions and Industrial and Provident Societies.

- In the rest of the UK credit unions are governed by three pieces of legislation and regulated by the Financial Services Agency.

- In the Republic of Ireland credit unions are governed by a single piece of legislation and regulated by the Financial Regulator.

- Article 24 of the Credit Unions ( Northern Ireland) Order 1985 expressly forbids credit unions in Northern Ireland from participating in the ‘business of banking’.

- In the rest of the UK and the Republic Ireland, recent changes to the governing legislation have removed this limitation.

- Northern Ireland ’s legislative anomalies have left credit unions with an operational disadvantage, in the following areas:

- The provision of services;

- Investment into the local community;

- The provision of Child Trust Fund Schemes;

- Promoting Financial Inclusion.

- Both the Irish League of Credit Unions and the Ulster Federation of Credit Unions have recommended the removal of Article 24.

- A comparison of the services offered by credit unions in the three areas examined, demonstrates the limitations placed upon Northern Ireland’s credit unions. In Northern Ireland, credit unions offer basic financial services, namely Share Accounts, loans and Life Assurance. In Great Britain and the Republic of Ireland the range of services offered by credit unions is wider (please refer to the table on page for details).

- Northern Ireland ’s credit unions receive no governmental funding. Credit unions in the rest of the UK have access to a £36 million growth fund for third sector lenders. This fund was bolstered by a further £6 million in 2007-08.

- In its recent paper on Financial Inclusion the HM Treasury Select Committee recognised the important role played by third sector lenders in promoting financial inclusion and made recommendations designed to increase the coverage and capacity of third sector lenders.

- None of these recommendations apply to credit unions in Northern Ireland.

- Both the Irish League of Credit Unions and the Ulster Federation of Credit Unions have criticised the HM Treasury Select Committee Document.

- The main issues facing Northern Ireland’s credit unions, in light of the above, can be summarised as follows:

- Access to services due to differential legislative constraints;

- The provision of Child Trust Fund Scheme;

- The capacity to invest in their local communities;

- Access to funding to help promote social inclusion through an expansion of the coverage and capacity of credit unions;

- The promotion of social inclusion in the current legislative climate.

A table summarising the operational differences between credit unions in Great Britain, Northern Ireland and the Republic of Ireland can be found in Annex 3.

Introduction

Following a request from the Committee on Enterprise, Trade and Investment this paper addresses the following points:

- The regulatory framework governing credit unions in Great Britain, Northern Ireland and the Republic of Ireland;

- The variation of services available to credit union members in Great Britain, Northern Ireland and the Republic of Ireland;

- The funding available to credit unions in Great Britain, Northern Ireland and the Republic of Ireland;

- The Treasury Select Committeerecommendations on credit unions and a discussion of the Government’s Financial Inclusion Strategy for 2008-2011.

1 Background:

There are currently 549 credit unions in England, Scotland and Wales i. Across the UK less than 1% of the population are members of a credit union. However, the situation in Northern Ireland is different, with over 26% of the population being members ii. There are approximately 170 credit unions in Northern Ireland iii.

Modelled on similar organisations in the US the first credit union in Northern Ireland, and the first in the UK, was co-founded by John Hume in Londonderry in 1960 iv. The first credit union in the Republic of Ireland was established in 1958 by Nora Herilhy in Dublin. Currently there are over 500 credit unions in the Republic of Ireland v.

The success of Northern Ireland’s credit unions has been attributed to their promotion by established community groups and religious organisations, particularly the Catholic Church and, more recently, the Orange Order vi. The perception that credit unions are financial institutions run 'by the community for all the community' is also thought to have inspired their popularity within Northern Ireland vii.

Research undertaken by the Joseph Rowntree Foundation found that the strength of the movement in NI stemmed in part from the fact that, from “the outset, […] their long term viability requires that they attract a cross section of people from local communities, and not just those who are socially or financially excluded.” viii

This paper will now address the following points in turn; the regulatory framework governing credit union activity in Northern Ireland, the Republic of Ireland and Great Britain (section 2); the services offered by credit unions in each of the three areas (section 3); the funding available to credit unions (section4); and the HM treasury Select Committee’s recommendations concerning credit unions contained within the Financial Inclusion Strategy for 2008-2011 (section 5). The paper will conclude with a short discussion of the issues arising from each of these sections (section 6).

2 Regulatory Framework

The following section examines the legislation governing credit unions in Northern Ireland, Great Britain and the Republic of Ireland and contains an overview of each area’s regulatory authority. The section concludes with a discussion of the differences between each area’s regulatory framework and highlights some of the problems arising from these differences.

2.1 Northern Ireland

What follows is a brief outline of the legislation governing credit unions in Northern Ireland. It begins with an overview of the Credit Unions (Northern Ireland) Order 1985 and includes details of significant amendments to that order. Also included is a summary of Northern Ireland’s credit union regulatory authority. A more detailed outline of the regulations governing credit unions in Northern Ireland is contained in Annex 1.

2.1a Credit Unions (Northern Ireland) Order 1985

The Credit Unions (Northern Ireland) Order 1985 requires credit unions to register under the Industrial and Provident Societies Act (Northern Ireland) 1969, and places a duty on DETI’s Registrar of Companies, Credit Unions and Industrial and Provident Societies to make a report on proceedings under the legislation in respect of each year ix. The Order outlines the objects, conditions and rules a credit union must fulfil to allow for registration.

Significantly, Article 24 of The Credit Unions (Northern Ireland) Order 1985 (as amended) prohibits Northern Ireland’s credit unions from involvement in the “business of banking”, which limits the range of services they can offer to members x.

The Deregulation (Northern Ireland) Order 1997

The Deregulation (Northern Ireland) Order 1997 includes provisions designed to make the growth of credit unions easier, whilst continuing to ensure the safety of their members’ funds.

Article 3 of the Order amends the Credit Unions ( Northern Ireland) Order 1985 removing some of the burdens to credit union growth whilst retaining the protection they afford members xi.

Specifically, the Order increased the limit placed upon members’ shareholdings to £10,000 or 1.5% of the total shareholding of a credit union and limited loans to (a) the greater of £10,000 and 1.5% of total shareholding or (b) 20% of the credit union's general reserve, whichever is the lesser amount.

The Credit Unions (Limit on Shares) Order (Northern Ireland) 2006

Further alterations to the limit on shares were introduced by the Credit Unions (Limit on Shares) Order (Northern Ireland) 2006. The Order increased the limit on shares to £15,000 or 1.5% of the total shareholding of a credit union, which ever is the greater xii.

The Credit Unions (Deposits and Loans) Order (Northern Ireland) 2006

The Credit Unions (Deposits and Loans) Order (Northern Ireland 2006, amended Article 26(1) of the 1985 Order increasing the maximum deposit of a person too young to be a member from £1,000 to £10,000. The Order also increased the maximum loan amount available to members to £15,000 xiii.

The Credit Unions (Limit on Membership) Order (Northern Ireland) 2006

The Credit Unions (Limit on Membership) Order ( Northern Ireland) 2006 amended the 1985 order, increasing the maximum membership of credit unions from 5,000 to 10,000 xiv.

2.1b Regulatory Authority

Credit unions in Northern Ireland are regulated by the Registry of Companies, Credit Unions and Industrial and Provident Societies, part of DETI. The regulatory powers of the Registry were established by the Industrial and Provident Societies Act (Northern Ireland) 1969. The main priorities of the Registry are:

- The effective prudential supervision of credit unions;

- The efficient administration and, where appropriate, enforcement of society law and codes;

- The provision of an effective public search facility xv.

2.2 Great Britain

The following section outlines the legislation governing credit unions in England, Scotland and Wales, beginning with the Credit Unions Act 1979. An overview of amendments to this act and significant subordinate legislation is also included. The section concludes by examining Great Britain’s regulatory authority, highlighting some of the changes made by this authority. A more detailed outline of the regulations governing credit unions in Northern Ireland is contained in Annex 2.

2.2a Credit Unions Act 1979

In Great Britain the Credit Unions Act 1979 requires that credit unions in England, Scotland and Wales be registered under the Industrial and Provident Societies Act 1965. The 1979 Act also lays down the objects, conditions and rules a credit union must fulfil to allow for registration. These three sections are replicated in the Credit Union Order (Northern Ireland) 1985, which is outlined above.

The 1979 Act defines “common ground”, which exists as a prerequisite to credit union membership.

The Deregulation (Credit Unions) Order 1996

The Deregulation (Credit Unions) Order 1996 amends the terms of the Credit Unions Act 1979. The changes brought in by the Order served to extend the notion of common ground, increase share holding limits, introduce secured loans, raise the borrowing limit for non-qualifying members to the same level that applies to other members, and relax the limit on a member's borrowings.

2.2b Regulatory Authority

Financial Services and Markets Act 2000

The Financial Services and Markets Act 2000 (FSMA) established a system of financial regulation within which all regulation is carried out by a single body – the Financial Services Agency (FSA). The FSA regulates banks, building societies, credit unions, friendly societies, stockbrokers, derivatives dealers, fund managers, financial advisors, insurance companies and insurance intermediaries xvi.

The FSA regulation of Credit Unions applies to England, Scotland and Wales only xvii. This system of financial regulation enables credit unions in these areas to offer members a greater range of services than previously.

The FSMA grants the FSA the authority to alter the regulations governing third sector lenders, provided it “… publish a draft of the proposed rules in the way appearing to it to be best calculated to bring them to the attention of the public” xviii.

Under this proviso the FSA introduced the following changes, in January 2006, to the Credit Union Act 1979 (as amended):

- Increased the limit on loans from £10,000 to £15,000 xix;

- Increased the limit on members’ deposits from £5,000 to £10,000 xx;

- Increased the limit on deposits from persons too young to be members from £5,000 to £10,000, unless the deposits are held in a Child Trust Fund, in which case the credit union may accept a larger deposit xxi.

2.3 Republic of Ireland

The following section applies the same structure found in the above two sections to the Republic of Ireland. It concludes by outlining the most recent amendments made to the primary legislation.

2.3a Legislation

Until 1997 credit unions in the Republic of Ireland were governed by the Credit Union Act 1966. This Act was replaced by the Credit Union Act 1997. The 1997 Act defines the notion of common ground and sets out the rules and regulations governing credit union operation. Article 17, section 5 of the Act grants full membership rights, excluding voting, to under 16s. The Act also contains a provision which enables credit unions to “provide, as principal or agent, additional services of a description that appears to the Registrar to be of mutual benefit to its members” xxii.

2.3b Regulatory Authority

Since the 1 st April 2003 credit unions have been regulated by the Registrar of Credit Unions, under the Central Bank and Irish Financial Services Regulatory Authority (now The Financial Regulator) xxiii.

The Registrar took over the work previously carried out by the Registry of Friendly Societies up until 2003 and oversees the registration, regulation and supervision of Credit Unions, along with the maintenance of a Public Record file on each Credit Union. Under the Credit Union Act, 1997 (as amended), the Registrar has the authority to inspect any Credit Union xxiv.

2.3c Amendments

Based upon the above provision, which allows credit unions to “provide, as principal or agent, additional services of a description that appears to the Registrar to be of mutual benefit to its members” xxv amendments to the 1997 Act, in both 2004 and 2007, have significantly extended the remit of services available to credit union members. The 2004 amendment introduced services such as telephone and internet banking, electronic transfers of monies into credit union accounts, ATMs, Insurance services, discount services, bill payment services, bureau de change, money advice and budgeting services, money transfers, direct debits, standing orders, financial counselling, will making, gift cheques, electricity budget meter cards and Savings Stamps xxvi. The 2007 amendment further extended the range of services credit unions can offer to members, enabling them to provide pensions to their membership xxvii.

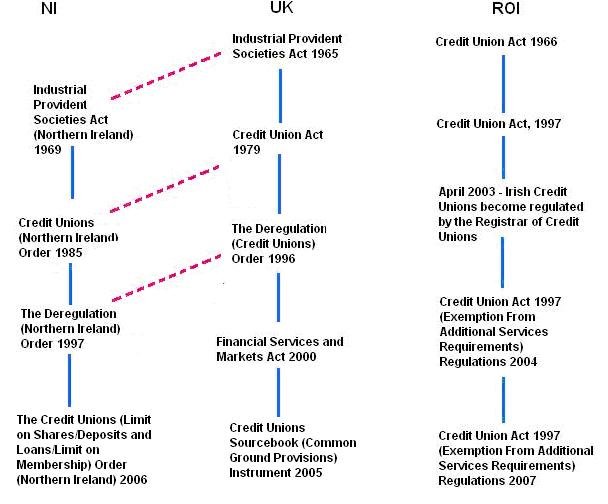

2.4

![]() = Amendments to primary legislation.

= Amendments to primary legislation.

![]() = Demonstrates the updating of one region’s regulations

= Demonstrates the updating of one region’s regulations

2.5 Legislative/Regulatory Impasse:

What follows is a brief overview of the legislative anomalies that affect Northern Ireland’s credit unions. The section is divided into four areas; the Business of Banking; Investment; Child trust Fund Schemes; and Financial Inclusion. The section also makes use of commentary from both the Irish League of Credit Unions and The Ulster Federation of Credit Unions.

The Business of Banking

A comparison of the regulations governing credit unions in the three geographical areas outlined above highlights the operational disadvantage facing Northern Ireland’s credit unions, particularly when it comes to the provision of banking services. The reason for this regulatory imbalance can be summarised in the following terms.

Paragraph 23 of Schedule 3 to the Northern Ireland Act, 1998, reserves the following to Westminster:

“…financial services, including investment, business, banking and deposit taking, collective investments and insurances; financial markets, including listing and public offers of securities and investments, transfer schemes and insider dealing” xxviii.

Furthermore, the Schedule continues “this does not include the subject matter of the Credit Unions (Northern Ireland) Order, 1985” xxix.

According to the Irish League of Credit Unions (ILCU) “… this means that credit unions in Northern Ireland cannot seek to expand into the reserved areas such as deposit taking, insurance and mortgage activity of any kind without concurrently seeking to be regulated by the Financial Services Agency” xxx.

This, coupled with Article 24 of the Credit Unions (Northern Ireland) Order, 1985, has had the effect that Northern Ireland has not benefited from the relaxation of regulations which has enabled their counterparts in England, Scotland and Wales to offer members a wider variety of services and to avail of funding.

The Ulster Federation of Credit Unions (UFCU) has called for the deletion of Article 24 as they believe this would allow credit unions to effectively meet the challenges set out in the Government’s Financial Inclusion Document (see below). On the ‘business of banking’ the Federation has said:

“The Federation believes that to become more effective it should be allowed to act as a bank and to take deposits, offer mortgages, and insurance products to its members. In this way the ‘third sector’ in Northern Ireland can become more effective and reach many more disadvantaged members of Northern Ireland’s society.” xxxi

Investment

Limiting credit unions in Northern Ireland to basic banking has also had the effect of preventing them from investing in their local communities. Both the ILCU and the UFCU have highlighted the need for change in this area.

The UFCU has stated that the “… primary legislation should be amended to allow … credit unions to invest in community development and community enterprise development initiatives. xxxii ”

The ILCU has also pointed out that in the “… Republic of Ireland, credit unions with excess liquidity may invest in community development and/or community enterprise projects”. They conclude that a similar provision in Northern Ireland would be of great benefit to disadvantaged communities but would require a change in legislation xxxiii.

Child Trust Fund Schemes

In addition to the above, Northern Ireland’s exclusion from the UK Government’s Child Trust Fund Scheme, on the grounds that the ILCU and UFCU do not offer the same level of protection as the Financial Services Compensation Scheme (FSCS), when the said scheme is not available to Northern Ireland’s credit unions, promotes an unfair balance of services between Credit Unions here and those in Great Britain xxxiv.

Financial Inclusion

Credit unions play a crucial role in promoting financial inclusion xxxv. However, the legislative anomalies that currently exist are deemed to prevent credit unions from maximising their capacity to carry out this function. On this subject the ILCU has stated:

“While the products and services available to credit union members in Northern Ireland constitute basic banking… it is clear that in order to enable equitable access to other basic financial services to middle and lower income groups, further legislative changes are required.” xxxvi

The UFCU has stated that a timely review of the current legislation is “… particularly appropriate as the Federation attempts to extend its coverage of disadvantaged Protestant areas of Northern Ireland and seeks to expand the services in makes available to its members. xxxvii”

3 Services Offered by Credit Unions

The following section provides a short comparison of the services offered by credit unions in Northern Ireland, Great Britain, and the Republic of Ireland.

Credit unions in Northern Ireland have a remit to offer a range of basic financial services, namely Share Accounts, loans and Life Assurance xxxviii. However, the legislative limitations placed upon Northern Ireland’s credit unions, particularly Article 24 of The Credit Unions (Northern Ireland) Order 1985 (as amended), which expressly prohibits credit unions in Northern Ireland from carrying out the business of banking, prevents them from offering a range of services equivalent to those offered by their counterparts in Great Britain and the Republic of Ireland xxxix.

Credit unions in Great Britain and the Republic of Ireland, without such limitations can offer members a wider range of services. Listed below is a breakdown of services offered in Northern Ireland compared to the additional services offered in the other two regions

| NI | ROI |

GB |

| Share Accounts | Internet/Telephone banking |

Current Accounts |

| Loans | Electronic Transfers of wages etc into accounts |

Internet/Telephone banking |

| Life Assurance | ATMs |

Electronic Transfers of wages etc into accounts |

Home, travel, car and health insurance |

ATMs |

|

Discount services |

Home, travel, car and health insurance |

|

Micro-Finance Lending |

Discount services |

|

Money Advice and Budgeting Services |

Debit Cards |

|

Bill Payment |

Mortgage |

|

Direct Debit |

Bill Payment |

|

Standing Orders |

Direct Debit |

|

Financial Counselling |

Standing Orders |

|

Will Making |

Junior Savings Accounts |

|

Gift Cheques |

||

Electricity Budget Meter Cards |

||

Savings Stamps |

||

Pensions |

||

Junior Savings Accounts |

4 Access to Funding:

Having outlined regulatory framework associated with and services offered by credit unions in Northern Ireland, Great Britain and the Republic of Ireland the paper will now examine the funding available to credit unions in Northern Ireland.

In 2004 the UK Government set aside £36 million from the Financial Inclusion Fund to support a Department for Work and Pensions (DWP) growth fund for third sector lenders. The fund will be used “to make affordable loans more available through local third sector lenders such as Credit Unions and Community Development Finance Institutions xl.

The Government further boosted the capacity of third sector lenders in 2007-08 by announcing that an extra £6 million would be made available to them through the growth fund xli. This funding is available to credit unions in England, Scotland and Wales only.

The Ulster Federation of Credit Unions has asked that consideration “… be given to extending funding for credit unions in Northern Ireland to support the Government’s financial inclusion strategy”. xlii

The Irish League of Credit Unions has indicated that the failure to offer funding to Credit Unions in Northern Ireland hinders their effectiveness in the following areas:

Loan Guarantees: “If certain loans were Guaranteed, different lending criteria could be applied by the credit union no doubt leading to a different outcome. The potential long term benefit of such a scheme… is that the borrower may, in time, borrow in his/her own right on foot of their newly established saving/repayment history with the credit union.” xliii

Money Advice: “… any funding that could be made in this area… would no doubt operate to combat financial inclusion.” xliv

Capital Funding: “ … for participation in initiatives aimed at broadening the boundaries of financial inclusion…” xlv

Funding in the Republic of Ireland

Credit unions in the republic of Ireland can apply for loans from the Central Financial Service to pay for premises, equipment or for short-term liquidity purposes. In 2006, five credit unions applied for loans totaling €6.7m. The five loans were approved xlvi.

5 HM Treasury Select Committee Recommendations

This section contains an overview of the latest HM Treasury Select Committee recommendations concerning credit unions.

The HM Treasury Select Committee makes the following recommendations relating to credit unions in its recent paper on Financial Inclusion xlvii:

- The Government’s Affordable Credit Policy should focus on third sector lenders

- Much more support is needed if the third sector is to become a nationwide option;

- Increase the coverage and capacity of third level lenders;

- Set up a Financial Inclusion Taskforce to consider how this increase in coverage and capacity can be achieved;

- A further £6 million will be made available to credit unions and community development finance initiatives through the Department for Work and Pensions Growth fund. The new funding will be used to:

- To support new lending in parts of the country where supply of third sector affordable credit is insufficient

- To support the emergence of new banking providers, through financial support for credit unions investing in transactional banking capability

- To fund increased investment in the skills of third sector lenders’ staff and volunteers through a capacity-building programme.

- Carry out a Review of mutuals legislation with a view to increasing flexibility. The review will consider:

- Common Bond Restrictions;

- Corporate Deposits;

- Subsidiaries.

- Government recommendations do not include an extension of the Community Investment Tax Relief scheme to cover the personal lending activities of third sector lenders.

6 Discussion

What follows is a short discussion of the issues facing credit unions in Northern Ireland. The section makes use of commentary from both the Irish League of Credit Unions and the Ulster Federation of Credit Unions.

Commenting on the Governments “Financial Inclusion: the way forward” document, president of the Irish League of Credit Unions, Samuel Adair has said:

“It is nothing short of astounding that the Government’s document ‘Financial Inclusion: the way forward’ purports to set out the UK Government’s financial inclusion strategy for the 2008-2011 period without making reference to credit unions in Northern Ireland.” xlviii

The Ulster Federation of Credit Unions (UFCU) has also levelled criticism at the document, stating:

“The Ulster Federation of Credit Unions represents credit unions in many deprived protestant working class areas with little or no governmental support. The Federation feels that the Government’s Financial Inclusion Strategy should apply equally to Northern Ireland as to the rest of the UK and that government assistance for credit unions in the rest of the UK should be made available in Northern Ireland.” xlix

Fundamentally the recommendations do not seek to transverse the legislative gap between Northern Ireland and the rest of the UK. This legislative gap prevents the expansion of credit unions in Northern Ireland into additional regulated services and investment. To enable this expansion it would be necessary for credit unions here to be regulated by the FSA for all their activities and for the removal of Article 24 of the Credit Union Order (Northern Ireland) 1985.

The HM Treasury Select Committee’s recommendations do not attend to the differential access to Child Trust Fund Schemes, available to credit union members across the UK. Currently, credit unions in England, Scotland and Wales may accept deposits, in excess of £10,000, on behalf of non-members under 16 years-of-age, so long as these deposits are held in a Child Trust Fund l. Such a provision does not exist in the legislation that governs credit unions in Northern Ireland li. On the issue of Child Trust Funds the UFCU has asked that consideration be given to extending the scheme to Northern Ireland. The Federation believes that such a move would be particularly pertinent at this time as it is “… currently expanding its operation of children’s accounts for savings into local schools lii ”.

Furthermore, the funding imbalances, which exist between credit unions in Northern Ireland and the rest of the UK, are not addressed. At present, credit unions in England, Scotland and Wales have access to funding through the Department for Work and Pensions growth fund. The HM Treasury Select Committee has recognised the benefits of this funding liii; however, credit unions in Northern Ireland are currently unable to avail of it.

7 Conclusion

The main issues facing Northern Ireland’s credit unions can be summarised as follows:

- The limitations imposed by Article 24 of the Credit Unions (Northern Ireland) Order 1985;

- Access to services due to differential legislative constraints, particularly the services which fall under the ‘business of banking’ heading;

- The provision of Child Trust Fund Scheme and the availability of protection under the Financial Services Compensation Scheme;

- The capacity to invest in their local communities;

- Access to funding to help promote social inclusion through an expansion of the coverage and capacity of credit unions. Credit Unions in England, Scotland and Wales have access to growth fund provided by the DWP;

- Exclusion from the HM Treasury Select Committee’s “financial inclusion: the way forward” document and its aim to increase the coverage and capacity of third level lenders;

- The promotion of social inclusion in the current legislative climate.

Annex 1

Regulatory Framework Northern Ireland

Credit Unions (Northern Ireland) Order 1985

Superseding the Industrial and Provident Societies Act (Northern Ireland) 1969 Act the Order introduced the following changes:

- Credit unions may have a minimum of 21 and a maximum of 5,000 members;

- Members leaving the common bond may retain full borrowing powers for one year;

- Limited pre-membership deposits may be accepted from children under 16 years, to be held in trust until the child turns 16, and then either converted to shares or withdrawn by the depositors;

- The maximum dividend on shares was increased to 8%;

- Insurance against fraud and dishonesty must be maintained by all registered credit unions liv.

Under the terms of the Order credit unions should have the following objectives:

- The promotion of thrift among members by the accumulation of their savings;

- The creation of sources of credit for the benefit of members and a reasonable rate of interest;

- The control and use of members’ savings for their mutual benefit;

- The training and education of members in the wise use of money in their financial affairs.

The 1985 Order strictly regulates the operation of Credit unions by placing limits on the:

- Size of loans which a credit union may make to a member;

- The value of a member’s share holding in the credit union;

- The dividend payable on member’s shares

- The rate of interest on loans and investment lv.

The Deregulation (Northern Ireland) Order 1997

The order served to:

- Increase the limit placed upon members’ shareholding levels from £5,000 or 1.5% of the total shareholding of a credit union to £10,000 or 1.5% of the total shareholding of a credit union;

- Ensure that the total amount on loan to a member of a credit union shall not at any time exceed his total paid-up shareholding in the credit union by more than (a) the greater of £10,000 and 1.5% of total shareholding or (b) 20% of the credit union's general reserve, whichever is the lesser amount.

The Credit Unions (Limit on Shares) Order (Northern Ireland) 2006

Further alterations to the limit on shares were introduced by the Credit Unions (Limit on Shares) Order (Northern Ireland) 2006. The Order increased the limit on shares to £15,000 or 1.5% of the total shareholding of a credit union, which ever is the greater lvi.

The Credit Unions (Deposits and Loans) Order (Northern Ireland) 2006

The Credit Unions (Deposits and Loans) Order (Northern Ireland 2006, amends Article 26(1) of the 1985 Order increasing the maximum deposit of a person too young to be a member from £1,000 to £10,000. The Order also increased the maximum loan amount available to members to £15,000 lvii.

The Credit Unions (Limit on Membership) Order ( Northern Ireland) 2006

The Credit Unions (Limit on Membership) Order ( Northern Ireland) 2006 amended the 1985 order, increasing the maximum membership of credit unions from 5,000 to 10,000 lviii.

Annex 2

Regulatory Framework Great Britain

Credit Unions Act 1979

The objects of a credit union, as defined by the Credit Unions Act 1979, should be as follows:

- The promotion of thrift among members by the accumulation of their savings;

- The creation of sources of credit for the benefit of members and a reasonable rate of interest;

- The control and use of members’ savings for their mutual benefit;

- The training and education of members in the wise use of money in their financial affairs.

The 1979 Act defines “common ground”, which exists as a prerequisite to credit union membership. For registration as a credit union to take place an organisation’s membership must fulfil one or more of the following criteria:

- They are living and/or working in a particular geographical area;

- They are a member of, or have an association with, a particular organisation;

- They are working for a common employer;

- They are following a particular occupation lix.

The Credit Unions Act 1979 obliges that credit unions operate under the following rules and regulations:

- Each share in a credit union is fixed by statute at £1.00

- The maximum saving permitted is £5,000 or 1.5% of the total shareholding of a credit union, whichever is the greater

- A credit union may accept deposits only as subscription for its shares;

- It may pay a dividend on shares, not exceeding 8%, after all expenses and taxes have been accounted for;

- The normal range of dividend payments is between 3 and 5%;

- Loans may be made to members up to a maximum of £5,000 in excess of their share capital. So a member with the maximum of £5,000 shares may borrow up to £10,000 lx.

The Deregulation (Credit Unions) Order 1996

The Deregulation (Credit Unions) Order 1996 amends the terms of the Credit Unions Act 1979 as follows:

- Article 3 introduces a new membership qualification for credit unions: that of either living or working in a particular locality. It also allows the appropriate registrar to register a credit union on the basis of a statutory declaration by three members and the secretary that a common bond exists among the members;

- Article 4 allows a member to hold shares of up to 1.5% of a credit union's total shareholdings, if that produces a higher figure than the £5,000 already permitted;

- Article 5 ensures a loan, which is equal to or less than a member's shareholding, should be regarded as a secured loan (which can be repaid over a longer period than an unsecured one). It also amends section 7(5) of the Act to prevent a member from withdrawing the shares used to support such a loan;

- Article 6 amends sections 11(3) and 5(8) of the Act to raise the borrowing limit for non-qualifying members to the same level that applies to other members;

- Article 7 relaxes the limit on a member's borrowings for those credit unions which can demonstrate to the Registrar that they have satisfactory arrangements to deal with the increased risk. The maximum that may be lent by such an approved credit union, in excess of shareholding, becomes: (a) the greater of £10,000 and 1.5% of total shareholding or (b) 20% of the credit union's general reserve, whichever is the lesser amount lxi.

Financial Services and Markets Act 2000

The Financial Services and Markets Act 2000 (FSMA) established a system of financial regulation within which all regulation is carried out by a single body – the Financial Services Agency (FSA).

The key features of the FSA’s regulation of Credit Unions are:

- Credit unions have to meet a basic test of solvency. Additional capital requirements are set for larger credit unions, reflecting their potentially greater impact on consumers should they fail;

- Credit unions are required to maintain a minimum liquidity ratio;

- Key personnel running credit unions have to meet the standards set out in the FSA’s rules for Approved Persons;

- Senior management of a credit union must take reasonable care to plan, direct, manage and maintain systems and controls as are appropriate to the business of their credit union;

- Credit unions are required to comply with the FSA’s rules on Money Laundering;

- Credit unions are required to operate an effective complaints scheme with members having access to the new Financial Ombudsman Service if they are not satisfied with the way their complaint has been handled;

Credit unions have access to the Financial Services Compensation Scheme providing members with deposit protection for the first time lxii.

Annex 3

|

Northern Ireland |

Great Britain |

Republic of Ireland |

Legislation |

1 Primary piece and 4 Subordinate pieces of legislation - Article 24 of Credit Union ( Northern Ireland) Order prevents 'business of banking' Credit Union legislation in Northern Ireland mirrored the legislation in the UK up until the Financial Services and Markets Act 2000 |

3 pieces of primary legislation. Most recent legislation allows credit unions to engage in the business of banking |

1 Primary piece of legislation superseding previous legislation, which (as amended) allows credit unions to engage in the business of banking |

Regulatory Authority |

Registry of Companies, Credit Unions and Industrial and Provident Societies |

Financial Services Agency |

Financial Regulator |

Services |

Limited to basic banking: ● Share Accounts ● In Northern Ireland Credit Unions the limit placed upon member’s shares is to £15,000 or 1.5% of the total shareholding of a credit union, which ever is the greater. ● The maximum loan amount available to members to £15,000. |

Extended beyond basic banking to include: ● Current Accounts |

Extended beyond basic banking to include: ● Internet/Telephone banking |

|

Northern Ireland |

Great Britain |

Republic of Ireland |

Funding |

No funding available |

Funded by the Department of Work and Pensions growth fund |

Can apply to the Central Financial Service for loans. |

HM Treasury Select Committee Recommendations |

Do not apply to Northern Ireland |

Recognises the role of credit unions in promoting financial inclusion. Makes recommendations designed to promote the coverage and capacity of third sector lenders. |

N/A |

i House of Commons Treasury Twelfth Session Report from session 2005-2006, 7 November 2006 http://www.publications.parliament.uk/pa/cm/200505/cmselect/cmtreasy/848/84802.htm

ii Ibid

iii Consumer Line – Money Matters – Credit Unions http://www.consumerline.org/search/?cat=Money+Matters&item=Credit+Unions

iv WOCCU Honor for John Hume, Nobel Prize-Winner http://www.scottishcu.org/files/documents/WOCCU%20Honour%20for%20John%20Hume.pdf

v About the Credit Union in Ireland - http://www.creditunion.ie/publisher/index.jsp?re=0&pID=93&nID=594

vi Building Better Credit Unions http://www.jrf.org.uk/bookshop/eBooks/9781861348302.pdf p.9

vii Building better credit unions Findings 2006 http://www.jrf.org.uk/knowledge/findings/socialpolicy/0066.asp

viii House of Commons Treasury Twelfth Session Report from session 2005-2006, p.5

ix Department of Enterprise, Trade and Investment Registrar of Credit Unions Report 2006 p2

x Department for Work and Pensions quoted in House of Commons Treasury Twelfth Session Report, p.4 http://www.publications.parliament.uk/pa/cm200506/cmselect/cmtreasy/848/84802.htm

xi Ibid p.7

xii Credit Unions (Limit on Loans) Regulations (Northern Ireland) http://www.statutelaw.gov.uk/content.aspx?LegType=All+Legislation&title=Credit+Unions+(Limit+on+Shares)+Order+(Northern+Ireland)+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&sortAlpha=0&TYPE=QS&PageNumber=1&NavFrom=0&parentActiveTextDocId=2878663&ActiveTextDocId=2878671&filesize=2109

xiii The Credit Unions (Deposits and Loans) Order (Northern Ireland) 2006 http://www.statutelaw.gov.uk/legResults.aspx?LegType=All+Legislation&title=Credit+Unions+Northern+Ireland+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&TYPE=QS&NavFrom=0&activeTextDocId=2878675&PageNumber=1&SortAlpha=0

xiv The Credit Unions (Limit on Membership) Order (Northern Ireland) 2006 http://www.statutelaw.gov.uk/content.aspx?LegType=All+Legislation&title=Credit+Unions+Northern+Ireland+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&sortAlpha=0&TYPE=QS&PageNumber=1&NavFrom=0&parentActiveTextDocId=2878654&ActiveTextDocId=2878660&filesize=638

xv Registry of Credit Unions Annual Report 2006 http://www.detini.gov.uk/cgi-bin/downutildoc?id=1870 p1

xvi Butterworth’s Financial Regulations Service/Binder 1a – General Division A The Regulatory Structure/Chapter 1 The Financial Service and Markets Act 200/Part 1 The Regulatory Structure

xvii How we regulate Credit Unions http://www.fsa.gov.uk/Pages/Doing/small_firms/unions/how/index.shtml

xviii Financial Services and Markets Act 2000, Part X Rules and Guidance, Chapter I Rule-making Powers S138 http://www.opsi.gov.uk/Acts/acts2000/ukpga_20000008_en_12#pt10-ch1-pb4-l1g153

xix Credit Unions Sourcebook (Common Ground Provisions) Instrument 2005 http://fsahandbook.info/FSA/handbook/LI/2005/2005_67.pdf p.2

xx Ibid p. 6

xxi Ibid

xxii Credit Union Act 1997 Article 48, sec 1, p41 http://www.gov.ie/bills28/acts/1997/a1597.pdf

xxiii The Financial Regulator and Registrar of Credit Unions http://www.creditunion.ie/publisher/index.jsp?1nID=93&2nID=597&3nID=3047&4nID=3050&nID=3058

xxiv Ibid

xxv Credit Union Act 1997 Article 48, sec 1, p41 http://www.gov.ie/bills28/acts/1997/a1597.pdf

xxvi Credit Union Act 1997 (Exemption from Additional Services Requirements) Regulations 2004 - http://www.ifsra.ie/data/in_cru_files/S.I.%20No.%20223%20of%202004%20-%20Credit%20Union%20Act%201997%20(Exemption%20From%20Additional%20Services%20Requirements)%20Regulations%202004.pdf p. 1-6

xxvii Credit Union Act 1997 (Exemption from Additional Services Requirements) Regulations 2007 - http://www.ifsra.ie/data/in_cru_files/S.I.%20No.%20107%20of%202007%20–%20Credit%20Union%20Act%201997%20Exemption%20for%20Additional%20Services%20Requirements%20-%20Regulations%202007.pdf p. 2

xxviii Northern Ireland Act, 1998, Schedule 3, Paragraph 23

xxix Ibid

xxx Irish League of Credit Unions: Financial Inclusion Northern Ireland – Briefing Document for a Meeting with the Rt Hon John McFall (Chairman, Treasury Select Committee) on Wednesday, 06 September 2006 p 4

xxxi Financial Inclusion – The Ulster Federation of Credit Unions p 3

xxxii Ibid

xxxiii Irish League of Credit Unions: Financial Inclusion Northern Ireland – Briefing Document for a Meeting with the Rt Hon John McFall (Chairman, Treasury Select Committee) on Wednesday, 06 September 2006 p. 17

xxxiv Ibid p 15

xxxv About Credit Unions – Financial Exclusion http://www.abcul.org/page/about/financialexclusion.cfm

xxxvi Ibid p.17

xxxvii Financial Inclusion – The Ulster Federation of Credit Unions p 2 - 3

xxxviii Irish League of Credit Unions: Financial Inclusion Northern Ireland – Briefing Document for a Meeting with the Rt Hon John McFall (Chairman, Treasury Select Committee) on Wednesday, 06 September 2006 p17

xxxix Ibid p6

xl Department for Work and Pensions quoted in House of Commons Treasury Twelfth Session Report, p.4 http://www.publications.parliament.uk/pa/cm200506/cmselect/cmtreasy/848/84802.htm

xli HM Treasury – Financial Inclusion: the way forward, March 2007 http://www.hm-treasury.gov.uk/documents/financial_services/financial_inclusion/financial_inclusion_wayforward.cfm p.46

xlii Financial Inclusion – The Ulster Federation of Credit Unions p. 3

xliii Irish League of Credit Unions: Financial Inclusion Northern Ireland – Briefing Document for a Meeting with the Rt Hon John McFall (Chairman, Treasury Select Committee) on Wednesday, 06 September 2006 p. 14

xliv Ibid p. 15

xlv Ibid

xlvi http://www.creditunion.ie/files/20070316031137_4%20Operational1%20-%20FINAL%20PDF.pdf

xlvii HM Treasury – Financial Inclusion: the way forward, March 2007 http://www.hm-treasury.gov.uk/documents/financial_services/financial_inclusion/financial_inclusion_wayforward.cfm p. 45 - 6

xlviii Letter to Mark Durkin from Samuel Adair re: Northern Ireland Credit Unions – Legislation/Access to Funding, 30 May 2007

xlix Financial Inclusion – Ulster Federation p. 2 - 3

l Credit Unions Sourcebook (Common Ground Provisions) Instrument 2005 http://fsahandbook.info/FSA/handbook/LI/2005/2005_67.pdf p 6

li The Credit Unions (Limit on Membership) Order (Northern Ireland) 2006 http://www.statutelaw.gov.uk/content.aspx?LegType=All+Legislation&title=Credit+Unions+Northern+Ireland+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&sortAlpha=0&TYPE=QS&PageNumber=1&NavFrom=0&parentActiveTextDocId=2878654&ActiveTextDocId=2878660&filesize=638

lii Financial Inclusion – Ulster Federation p. 3

liii HM Treasury – Financial Inclusion: the way forward, March 2007 http://www.hm-treasury.gov.uk/documents/financial_services/financial_inclusion/financial_inclusion_wayforward.cfm p. 46

liv Department of Enterprise, Trade and Investment Registrar of Credit Unions Report 2006 p2

lv Ibid

lvi Credit Unions (Limit on Loans) Regulations (Northern Ireland) http://www.statutelaw.gov.uk/content.aspx?LegType=All+Legislation&title=Credit+Unions+(Limit+on+Shares)+Order+(Northern+Ireland)+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&sortAlpha=0&TYPE=QS&PageNumber=1&NavFrom=0&parentActiveTextDocId=2878663&ActiveTextDocId=2878671&filesize=2109

lvii The Credit Unions (Deposits and Loans) Order (Northern Ireland) 2006 http://www.statutelaw.gov.uk/legResults.aspx?LegType=All+Legislation&title=Credit+Unions+Northern+Ireland+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&TYPE=QS&NavFrom=0&activeTextDocId=2878675&PageNumber=1&SortAlpha=0

lviii The Credit Unions (Limit on Membership) Order (Northern Ireland) 2006 http://www.statutelaw.gov.uk/content.aspx?LegType=All+Legislation&title=Credit+Unions+Northern+Ireland+&searchEnacted=0&extentMatchOnly=0&confersPower=0&blanketAmendment=0&sortAlpha=0&TYPE=QS&PageNumber=1&NavFrom=0&parentActiveTextDocId=2878654&ActiveTextDocId=2878660&filesize=638

lix Particular bodies: credit unions: introduction – http//www.hmrc.gov.uk/manuals/ctmanual/ctm401.55.htm

lx Proposed amendments to the Credit Unions Act 1979 - http://www.hm-treasury.gov.uk/consultations_and_legislation/consult_credit/consult_credit_nov98.cfm

lxi www.opsi.gov.uk/SI/si1996/Uksi_19961189_en_1.htm - 23

lxii How we regulate Credit Unions http://www.fsa.gov.uk/Pages/Doing/small_firms/unions/how/index.shtml