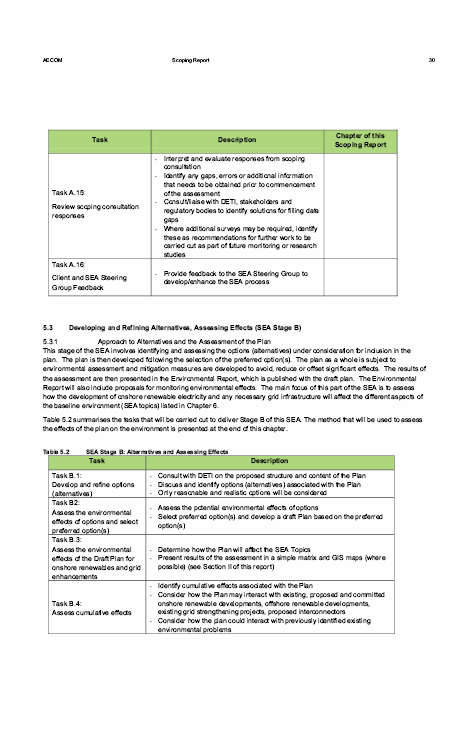

| Homepage > The Work of the Assembly > Committees > Statutory > Enterprise, Trade and Investment > Reports | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Committee for Enterprise, Trade and InvestmentReport on the Committee's Inquiry into Barriers to the Development of Renewable Energy Production and its Associated Contribution to the Northern Ireland Economy - Volume 2Together with the Minutes of Proceedings of the Committee Ordered by The Enterprise, Trade and Investment Committee to be printed 27 January 2011 Written Submissions

Session 2010/2011Third ReportTable of ContentsVolume 23. Written Submissions to the Committee Written SubmissionsAppendix 3 – Written Submissions1. Action Renewables 2. Armagh City and District Council 3. B9 Energy 4. Belfast City Council 5. Biomass Energy NI 6. Carbon Trust NI 7. Committee for Regional Development 8. Department of Agriculture and Rural Development 9. Department for Employment and Learning 10. Department of Enterprise, Trade and Investment 11. Department for the Environment 12. Department for Regional Development 13. ESB Wind Development UK Ltd. 14. ESBI Ocean Energy, ESB International 15. Farm Woodlands Ltd. 16. Fasttrack to IT 17. Fermanagh District Council 18. Glen Dimplex 19. Green Energy 4 U 20. Green Party 21. GT Energy 22. IBEC-CBI Joint Business Council 23. Invest Northern Ireland 24. John Simpson 25. Lisburn City Council 26. Michael Coyle 27. Northern Ireland Authority for Utility Regulation 28. Northern Ireland Energy Agency 29. Northern Ireland Environment Link 30. Northern Ireland Renewables Industry Group 31. Northern Ireland Electricity (NIE) Energy Supply 32. Northern Ireland Electricity (NIE) 33. Northern Ireland Manufacturing 34. NPP MicrE and NPP Smallest Projects 35. Office of First Minister deputy First Minister 36. Omagh District Council 37. Phoenix 38. Renewable Energy Systems Ltd 39. RSPB Northern Ireland 40. Rural Generation Ltd 41. SmartGridIreland 42. Ulster Farmers Union 43. University of Ulster 44. WWF Northern Ireland Response from Action Renewables

Please provide some background information on the companyAction Renewables is the leading organisation in Northern Ireland in the promotion and development of renewable energy. Action Renewables delivers a large portfolio of programmes including: general awareness raising; seminars; performance monitoring of technologies; research and evaluation and policy development. Action Renewables was set up in 2003, as a partnership between Department of Enterprise and Investment (DETI) and Viridian Group. Our objectives are to significantly raise awareness of the impending threat from climate change, understanding of the issues associated with conventional energy use and to help facilitate the development and use of low carbon energy across Northern Ireland. Section 2 Government Strategy for Renewable Energy2.1 Please provide information on your level of awareness of current Government Strategy for Renewable Energy and how that strategy assists the renewable energy sectorAction Renewables is the leading organisation in Northern Ireland in the promotion and development of renewable energy. Action Renewables delivers a large portfolio of programmes including: general awareness raising; seminars; performance monitoring of technologies; research and evaluation and policy development. Our principal aim is to promote Northern Ireland Government policy in respect of renewable energy. This includes raising awareness about climate change and its impact on Northern Ireland and how sustainable energy can provide solutions. To meet the set targets and assist the sector, the strategy needs to ensure that:

2.2 Please provide information on any Government support that your company has received in the past that is specifically related to renewable energyAction Renewables was set up in 2003, as a partnership between Department of Enterprise and Investment (DETI) and Viridian Group. For the first four years of our existence we were fully funded by DETI, whereas for the last three years our funding has been gradually reduced, and from the 1st April 2011 we will no longer receive any funding from DETI. 2.3 Please provide information on any Government support that your company has applied for or is planning to apply for in the future that is specifically related to renewable energyN/A 2.4 Please provide information on the barriers within Government to developing the renewable energy sector in Northern IrelandNorthern Ireland is a small economic unit, with a population of approximately 1.7 Million. Perhaps a better approach for renewable energy technologies to grow and develop, in what is still an emerging market, is to have an overall strategic policy that is applied in a UK wide context, with local administrations applying a 'local context' implementation plan. Thus we would have an overall policy with local factors taken into consideration. In addition, SME's could base business cases on long term strategies, but still be able to lobby for local conditions to be taken into consideration. 2.5 Please provide suggestions on how Government can better support the renewable energy sector in the future in order to grow and develop the sector (suggestions should be specific to the renewable energy sector)

Section 3 Government Strategy for Economic Development and its Application to the Renewable Energy Sector3.1 Please provide information on your level of awareness of current Government Strategy for Economic Development and how that strategy assists businessesA number of Government bodies and agencies contribute to a strategy for economic development, many of which have produced reports and policy on economic development:

SME's and Businesses will generally welcome the reports and policies but will usually argue that it can be difficult to access the correct information, speak to the appropriate person or just find it complicated to be signposted in the right direction. Therefore the strategy that assists best is one of 'joined up government'. 3.2 Please provide details of any Government support for economic development (at any level) that your company has had in the pastSee answer to 2.2 above. 3.3 Please provide information on any Government support for economic development that your company has applied for or is planning to apply for in the futureN/A 3.4 Please provide information on the barriers within Government to developing the indigenous businesses in Northern IrelandRecent Government announcements have strongly indicated the dissolution of the Carbon Trust (along with other similar Government funded organizations like the Energy Saving Trust, Technology Strategy Board and Sustainable Development Commission). The aim is that the monies saved would be put into a 'Green Investment Bank' in order to provide finance for sustainable projects. If however the bank is based in GB, without a Northern Ireland branch, it is likely that this arrangement will mitigate against Northern Ireland Projects, which tend to be smaller. Similarly, Venture capital companies tend to finance larger projects for an overall better return, once again NI is not likely to benefit. Government action should ensure this does not become a barrier to further development for NI companies. 3.5 Please provide suggestions on how Government can better support indigenous SME businesses in the future in order to assist them to grow and developmentInvest Northern Ireland (INI), has a three stranded approach to growing the economy, namely 1 - Exports, 2 - Inward investment and 3 - Support for commercialisation of R&D. However there is little or no support available to local SME's which service the Northern Ireland renewable energy market. Specifically, there would appear to be a lack of a specialised technical resource, within INI, to assist SME's to grow and develop their renewable energy technologies. This needs to be addressed. Further we would envisaged a coordination role for INI in the proposed 'Centre of Excellence' (see 2.5) Section 4 Communication, Sharing Information, Raising Awareness4.1 How well do you think Government departments communicate and share information with each other in relation to renewable energy and how can this be improved?It appears that Government departments find it difficult to successfully ensure that other departments are aware of the renewable energy research and projects they undertake. The cross–departmental working group set up to discuss renewable energy should ensure that at meetings, each department is represented and clearly highlights current or upcoming legislation and projects they are involved in relating to renewable energy. The group should then be asked to ascertain ways to support such projects across departments and/or develop projects which follow-on from those delivered by another department. 4.2 How well do you think the Government departments and local Government communicate and share information with each other in relation to renewable energy and how can this be improved?It would perhaps be beneficial to set up an additional renewable energy working group which contains a number of representatives from the cross-departmental working group as well as representatives from local Government. The cross-departmental representatives could relay information arising at departmental level to those at local level so that they are aware of current and upcoming legislation, research and projects and vice versa. Such a working group would serve to improve communication, information sharing and perhaps even allow for projects to be jointly developed between Government departments and local Government. 4.3 How well do you think the Government departments and the EU communicate and share information with each other in relation to renewable energy and how can this be improved?The EU focuses heavily upon the promotion of renewable energy and it would be therefore beneficial to establish good working relationships at this level. Representatives from the cross-departmental renewable energy working group should be appointed to monitor relevant information coming from the EU and pass this on to other members of the group. If feasible, a member of the working group should be appointed as the official liaison person for Northern Ireland Government departments and travel to Brussels to meet with and establish contacts in the EU. This relationship could allow Government departments to gain inspiration and ideas from Europe and give the EU the opportunity to learn more about how renewable energy is being developed in Northern Ireland. 4.4 How well do you think the Government departments and businesses communicate and share information with each other in relation to renewable energy and how can this be improved?Businesses can often find it difficult to liaise with Government departments and it can be hard for them to access the relevant people they need to talk to. Working closely with businesses to share information will help Government develop a strong renewable energy industry in Northern Ireland. This will not only ensure long term sustainable energy security but also help develop new economic opportunities in this sector. It could perhaps be beneficial for Government departments to offer appointment based surgeries whereby they set time aside once a fortnight to meet with businesses to discuss renewable energy issues, thus improving communication relations. Businesses could call or email to arrange an appointment, outline what they wished to discuss and it would then be arranged for them to meet with the appropriate person they need to speak to. 4.5 How well do you think the Government departments and other regions and EU Member States communicate and share information with each other in relation to renewable energy and how can this be improved?A vast level of information regarding renewable energy is shared by EU members, normally via EU projects, it is important that Government departments in Northern Ireland participate in this knowledge sharing in order to facilitate the successful development of renewable energy in Northern Ireland. Many countries in Europe have well established renewable energy industries and Government departments in Northern Ireland could learn a lot from these regions. The cross-departmental working group should appoint a number of representatives to liaise with other regions and EU members and feed this information back to the group, giving updates on legislation and ideas developed at regional and European level. 4.6 How well do you think businesses in the renewable energy sector communicate and share information with each other in relation to renewable energy and how can this be improved?The development of the renewable energy sector has slowed as a result of the financial crisis (and subsequent slow down of the construction industry). Businesses in the renewable energy sector now face even more direct competition from each other to secure work and for this reason, they tend to be less willing to communicate and share information with each other unless it is of mutual benefit. It is unlikely that this situation could be improved in the short term unless financial benefits were perceived to be gained from the interaction. 4.7 How well do you think Government departments communicate and share information with the public in relation to renewable energy and how can this be improved?Government departments appear to find it difficult to communicate directly with the public and interaction tends to be largely limited to press releases and consultations. Government have in the past used Third Party Organisations (TPO's) as intermediaries. Action Renewables was the main organisation in Northern Ireland to provide free, independent advice and information on renewable energy to the general public. Cuts in Government spending have resulted in funding being withdrawn and this information service is no longer available. It's important that Government understand that as renewable energy is still a relatively new industry, promoting education and understanding amongst the public remains paramount to its success and development. A number of advisory agencies in Northern Ireland do still remain although they do not provide advice specifically on renewable energy. The Energy Saving Trust specialises in energy efficiency information, while the carbon trust focus their information and advice service on businesses. An apparent gap therefore currently exists in relation to government departments communicating and sharing information on renewable energy with the public. To fill this gap Government should try to either develop their relationship with the general public or continue to fund an established TPO with renewable energy expertise to act as a liaison. 4.8 How well do you think renewable energy businesses communicate and share information with the public in relation to renewable energy and how can this be improved?Renewable energy businesses are keen to communicate and share information with the public however as they are trying to sell goods and services, the information they provide tends to favour the products they wish to sell. This means that this information can often be of limited value as it is neither independent nor impartial. As renewable energy businesses will always be primarily focused upon promoting their products, securing a sale and making a profit, it is difficult to ascertain how this situation could be improved upon. 4.9 What other support organisations are you aware of that exist to support the renewable energy sector?A number of advisory agencies in Northern Ireland indirectly support the renewable energy sector. The Energy Saving Trust for example specialises in providing energy efficiency information (improving the energy efficiency of a building is an important precursor to any renewable energy installation) while the carbon trust focus their information and advice service on businesses and carbon reduction. The Northern Ireland Energy Agency was administering the Low Carbon Buildings Programme Householder Grant but this UK-wide scheme closed in May 2010. A number of other organisations such as Northern Ireland Environment Link, Bio Energy Northern Ireland (BENI), the Sustainable Energy Association and the Wood Fuel Quality Assurance Scheme are not-for profit organisations which have been established to support the renewable energy sector in Northern Ireland. Through carrying out research, writing reports and lobbying Government they try to promote the successful development of the industry. 4.10 How well do you think Government departments and renewable energy support organisations communicate and share information with each other in relation to renewable energy and how can this be improved?When Action Renewables, as a support organisation, was fully funded by DETI an 'Implementation Plan' was agreed between the parties which would detail the work programme to be carried out in any particular year. The implementation plan would reflect bodies of work considered important by DETI e.g. awareness raising, research and reports and incorporate ideas from Action Renewables including monitoring and training for installers. Communication and sharing of information was achieved by regular update meetings between the parties. However, in the current situation where the funding levels are decreasing, communication between the parties is limited to bodies of work directly funded by the department. Therefore it is suggested that any Communications Initiative (see answer in 2.5) should not be limited to the 'wider community' but continue in a meaningful way between support organisations and government, so that engagement continues on issues surrounding the level of awareness and understanding of the wider issues surrounding the main drivers for renewable energy. 4.11 How well do you think renewable energy businesses and support organisations communicate and share information with each other in relation to renewable energy and how can this be improved?Action Renewables as a support organisation, has both formal and informal links with renewable energy businesses. Formal links include:

Other links would include accessing the AR website, informal meetings and telephone calls requesting information on a wide range of renewable energy policy. The situation could be improved and enhanced by an industry led 'forum' or 'body' which would have regular update meetings with support organisations and other interested parties. 4.12 How well do you think renewable energy support organisations communicate and share information with the public in relation to renewable energy and how can this be improved?When Action Renewables, as a support organisation, was fully funded by DETI, a significant part of the agreed 'Implementation Plan' was initiatives to raise awareness educate and inform the public in relation to renewable energy. However the Energy Saving Trust report, referred to in 2.5, also highlighted the following: While those who were aware of some renewable energy technologies, 49% of approx 500 people, only 6% were aware of either Biomass Boilers or Air Source Heat Pumps. This data illustrates that previous awareness raising plans were not as effective as envisaged or were discontinued too early. Action Renewables was an important information source for the public, however our current status of attracting other sources of funding, as public funding is reduced, means we are no longer in a position to maintain this vital function. Unless the public are able to make an informed decision regarding choices on renewable energy requirements it is difficult to be optimistic regarding how awareness can be improved. Section 5 Additional Information5.1 Please provide any additional information which you believe will be of assistance to the Committee during the course of the Inquiry

Section 6 Contact DetailsAll written responses should be sent to: Jim McManus Tel: 028 9052 1574 · Fax. 028 9052 1355 · Email: committee.eti@niassembly.gov.uk Response from Armagh District Council  Response from B9 Energy   Response from Belfast City CouncilDevelopment Department Your reference: Jim McManus, Committee Clerk Dear Mr McManus, Re. Barriers to Renewable Energy Production – NI Assembly Task Force ConsultationPlease find below our comments in response to your invitation to discuss barriers to renewable energy production. Most of the information in this response has come from our North Foreshore Project Manager (who is responsible for the Council's existing renewable electricity facilities) and our Planning team. Reference has also been made to an early consultation response to the Department of Environment Consultation on Permitted Development Rights, which included a section on Microgeneration (e.g. wind turbines, solar panels). That response was informed by our Environmental Services Department and was approved by the Council's Town Planning Committee on 3rd December 2009. It is available online if required. Please also note that the views expressed in this response are pending ratification by the Development Committee on the 11th August 2010. Unfortunately, the timescales and the timing of this consultation have made it impossible to submit a ratified response. Provisional ResponseBelfast City Council is making a significant contribution to non-wind renewable energy production. The Council developed the Landfill Gas Electricity Power Plant to utilise the methane gas at the North Foreshore Giant's Park, the former Dargan Road Waste Landfill site. Our landfill gas powered generating facility produces 5 megawatts of green electricity per hour sufficient to power 6,000 homes. However landfill gas is not sustainable, as the methane gas supply will progressively decline over a 15 – 20 year period. Alternative sources of renewable energy must be found. Anaerobic digestion (AD) is the solution but this is new to NI and as yet there are no commercial facilities in operation. The AD process produces methane gas which can be used for the production of renewable energy and heat. Questor and others have carried out extensive research into A.D. technology and this is an opportune time to develop AD facilities in NI. A major difficulty for potential operators is the identification of suitable sites and obtaining satisfactory planning consent for AD and other forms of renewable energy production, such as Energy from Waste. As shown at the end of this paper, the Council's own planning unit and committee have concerns about the potential noise, vibration and visual impact of renewable technologies when they are sited near domestic areas. The B9 a private sector company has spent 2/3 years in the planning process to secure planning consent for a proposed AD facility in Dungannon. If the Assembly Committee is to encourage renewable energy generation, planning consent must be made easier to obtain and the planning process speeded up. Delays of 2/3 years are not acceptable or economically attractive to commercial operators or their funders. Therefore there is a need to change the perception of renewable energy production facilities and educate those involved in the decision making and development process, not least the Planning Service and NIEA. Also there is a need to educate the public about modern renewable energy facilities, and the importance of guaranteeing energy security for NI. We encourage visitors to our North Foreshore facilities to help this education process. The North Foreshore Giant's Park site is unique as the only site in Draft Belfast Metropolitan Area Plan with a statutory waste management zoning. This should help to make it easier to secure planning consent for AD and EfW Facilities. Currently we are investigating the potential of promoting a site for a commercially operated AD facility at the North Foreshore Giant's Park. The project would have synergies for the Council's Landfill Gas Electricity Generation Power Plant as we have the generation capacity and the electrical infrastructure to export renewable energy from the site. It is suggested that future statutory local area development plans should designate suitable sites for renewable energy generation. This would help to speed up the development of renewable energy facilities in NI, assisting commercial decision making and investment. ROCs and LECs are available for AD biogas powered electricity generation and are currently at 2 ROCs per MWhr of electricity generated. The Committee will need to determine if this level of support is sufficient to encourage biogas production for electricity generation. Connection to the local electricity grid is another major barrier due to the significant set up costs involved. Electrical infrastructure to export the renewable energy at the North Foreshore Giant's Park cost the Council circa £2.5 million. Are there ways in which this could be reduced e.g. capping the NIE connection fee? It is suggested that clustering renewable energy facilities would maximise the use and efficiency of electrical infrastructure. In particular the new non wind renewable energy facilities such as AD and EfW are clean processes that could be located within settlement areas on brownfield industrial sites. Electricity generation facilities also usually produce large quantities of heat, which can be captured and used in production processes or for a district heating facility. The Committee should consider the introduction of Renewable Heat Incentives to NI to encourage operators to install heat exchangers and pipe network to make productive use of the waste heat. Again consideration needs to be given to clustering businesses / houses close to renewable energy facilities to minimise the cost of the pipe network. Summary of our previous Comments regarding planning permissionIn terms of planning permission for non-domestic microgeneration facilities they need to be considered in terms of the impacts they may have on adjacent properties, particularly residential properties. The Council views issues around noise, vibration and visual impacts as key considerations. The Council is concerned that the risk of adverse impacts from renewable energy technologies such as wind turbines is too great, in some instances, to allow for no consideration in the form of a planning application. The Council would encourage increased usage of such technology but a full assessment of impacts is necessary. The baseline taken is that non-domestic microgeneration PD will be at least on a par with the provisions for dwelling houses. The proposed changes will bring Northern Ireland permitted development rights closer in line with those in other UK jurisdictions. Yours sincerely David Dr David PurchasePolicy & Business Development Tel: 02890 320202 ext 3792 Response from Biomass Energy NI

Response from Biomass Energy Northern Ireland to the request for submission of evidence to the Northern Ireland Assembly Committee for Enterprise, Trade and Investment to inform it's enquiry into "renewable energy and the barriers to its development and contribution to the Northern Ireland economy". 1. Introduction to Biomass Energy – Northern Ireland1.1 Biomass Energy – Northern Ireland (BENI) was established in 2008 as a co-ordinating body for biomass producers and processors. Its aim is to facilitate the establishment of a sustainable supply chain from producer to end user. In doing so it aims to establish benchmarks and quality standards in the production and utilisation of energy from biomass crops. 1.2. Membership is open to anyone who supports our aims and objectives. Members have a large reservoir of knowledge and practical experience in the production and processing of biomass fuel. The membership currently includes a large proportion of the farmers who produce the approximately 1000 hectares of Short Rotation Coppice Willow which is grown and used in Northern Ireland for energy production; as well as suppliers of boilers and other equipment required to service this sector. 2. Biomass as a renewable energy source.2.1. BIOMASS –definition within the EU Renewables Directive: 'the biodegradable fraction of products, waste and residues from agriculture (including vegetable and animal substances) forestry and related industries, as well as the biodegradable fraction of industrial and food waste' A more practical definition has been provided by the Alternative Energy Association (AEA) and is used by DETI:

2.2. At present BENI's activities are focussed primarily on heat energy and developing a market for woodchip mainly derived from SRC willow. This is currently the most readily available and easily grown source of biomass in Northern Ireland, but it is certainly not the only one. Other sources of biomass comprise forestry and its wastes, sawmill residues and clean waste wood. In the future it may include miscanthus (elephant grass) and fast-growing hardwoods. BENI supports research into all forms of biomass which may be grown in Northern Ireland. The Agri Foodand Biosciences Institute (AFBI) has been a world leader in willow biomass for many years, and provides invaluable research support to the sector. We have very real concerns that the suggested closure of the AFBI Loughgall research facility will seriously disadvantage the renewable energy sector as long term trials cannot simply be moved to another AFBI site. This is the very time when the research is needed to help Northern Ireland achieve government targets for renewable heat. 2.3. There are many advantages to the use of biomass as a source of renewable energy in NI, including –

2.4. The Report of the Agricultural Stakeholder Forum on Renewable Energy "Renewable Energy in the Land Based Sector – A Way Forward 2009" identified a heat energy requirement in Northern Ireland of some 25,000 GWh/year, which represents some 52% of the total energy demand. Even though other studies suggest this is an overestimate, the figure is of this order. Through effective incentives applied to the renewable electricity sector ( Renewable Obligation Certificates ) DETI is on target to achieve the target of 12% on Northern Ireland's electricity to be supplied from indigenous renewable sources by 2012. On the other hand renewable heat is still very low at only 0.6 % of the UK heat demand –(DETI Consultation on the Bioenergy Action Plan for NI 2009 – 2014). This same document suggests the potential available to NI is up to 6.4% of heat demand. The potential for increased use of renewable heat energy is therefore considerable, while the technology is by and large simple, and requiring minimal development. What is required is the sustained political commitment and commercial incentive to make it happen. 3. Developing a Biomass Energy industry in Northern Ireland.3.1. "It's a chicken and egg problem"- Biomass production is a fledgling industry in Northern Ireland. Members of BENI have visited and studied developed biomass markets, principally in Sweden and Austria, and believe strongly that, if we can make the same thing happen here, there will be immense benefit to individual businesses in the supply chain and the whole NI economy, as well as economic benefits to individual consumers. 3.2. The problem in a nutshell is that farmers are unwilling to plant biomass crops unless they can be sure of having a long term market at a price which makes the enterprise viable, whilst heat users are reluctant to convert to biomass-fuelled systems unless they can be confident of reliable long term supply at attractive prices, 3.3. Overcoming the barriers to the development of a sustainable biomass energy sector in NI depends on successfully bridging that gap between producers and consumers. BENI is working with other organisations to achieve this, but lessons from elsewhere in Europe indicate that Government has a critical role to play in stimulating private sector involvement; supporting innovation; generating the confidence required to encourage the long term investment necessary and showing strong and committed leadership to the concept, through sustained action over a long timescale . Energy Service Companies3.4. BENI believes that the best long-term solution to supply management will be the creation of Energy Service Companies (ESCOs). ESCO's finance, design, build/install, operate and maintain agreed energy services equipment and undertake energy efficiency measures and savings under long term contractual arrangements. Usually an ESCO contracts to supply heat rather than fuel. Thus the ESCO takes responsibility for installing, running and maintaining the heating equipment. The customer pays for the provision of heat and does not have to manage the system and its fuel supply. The willow grower could sell his crop to the ESCO, which takes responsibility for supplying their boilers, while some growers may also be investors and partners in their ESCO. 4. Current Support Available in Northern Ireland.4.1. DARD has been proactive in developing support mechanisms and funding which falls within its terms of reference, including --

4.2. There is also excellent advice and documentation available through the Carbon Trust – e.g. "Biomass Heating – a practical guide for potential users"; as well as helpful zero interest loans. 4.3. Currently the support available in Northern Ireland to SRC willow producers and users is –

5. Barriers to the development of renewable energy production and its associated contribution to the NI economy.5.1. This is the fundamental question which this important inquiry has defined as its overall objective and one which we would like to address before commenting from our perspective on some of the specific issues raised by the Committee. The NI business owner – and that includes farmers – has a track record of rapid adoption of new technology where this has clear commercial advantages which compensates for the risk involved. We must therefore ask ourselves why any action needs to be taken by Government to stimulate the adoption of biomass energy – or in economic terms why there is a need to take action to overcome "market failure". 5.2. To take SRC willow in particular, the vast majority of the 1000 ha now producing energy crops was planted when the rate of grant was approximately double the £1000 hectare available today. In other words the risk of producing this "new" crop was much lower than it is today, when the new area planted each year is minimal. DARD in its Renewable Energy Action Plan 2010 has committed to continue this planting grant until 2013 but has stated that, despite an increase to 75% being recommended by the report on "Renewable Energy in the Land Based Sector – 2009" produced by the Agriculture Stakeholder Forum on Renewable Energy, it would not be appropriate to increase it. In DARD's view the current rate is the maximum allowed by regulation. The difficulty potential growers face is a high, up-front planting cost in excess of £2,000 / hectare, and a delay of 3 -4 years before the first harvest, and any return on their investment of land and capital. 5.3. However the planting grant is only one way of "funding" the risk – the other is to provide confidence that a high enough income can be sustained to balance the risk taken in planting the crop – which it must be remembered does not generate income for 3 years after planting and produces for at least 20 years thereafter. 5.4. The current difficulty is that for the business / public authority investing in the biomass boiler to justify the higher capital investment required (for both the boiler, storage and fuel delivery systems) and to achieve an acceptable return on its investment, the payment made for the biomass fuel is at a rate which makes production of very limited profitability at present fossil fuel prices. This is producing a situation whereby demand is starting to outstrip supply and this will worsen unless action is taken to increase income to producers. The alternative is to import biofuels, thereby losing the potential benefits to the local economy and adding to the use of fossil fuels in transporting the material. 5.5. This problem is by no means unique to Northern Ireland and the lessons from elsewhere in Europe are equally applicable here. The key messages are –

5.6. The omission of Northern Ireland from the Energy Act 2008 deprives us from the legislative basis for any Renewable Heat Incentive Scheme. This places Northern Ireland at a very significant disadvantage and puts the development of the renewable heat sector in serious danger of decline before it can even get off the ground. It is imperative that the Northern Ireland Executive in general and DETI in particular takes urgent action to rectify this situation. The sector requires confident and committed leadership to maximize opportunities which exist. BENI recognises that DETI has identified the need to provide a co-ordinated approach to this issue and has established a Bioenergy Interdepartmental Group with this objective. There does not however seem to be a single "renewable energy champion" to both lead and be accountable for the development of the sector. 5.7. We are aware that a study has been commissioned to consider what needs to be done to stimulate renewable heat in Northern Ireland but are becoming increasingly concerned at the plethora of studies, strategies and action plans being produced by Government. All of these seem to recommend further work and are being seen by some as a means of postponing difficult decisions and financial commitment. They contrast markedly with the limited financial support for those trying to make it happen and sustain their businesses in the real world. 5.8. There seems to be an unrealistic quest in policy makers to achieve certainty where certainty cannot be found. Predicting the future is a risky business. Real progress will require leadership and judgement based on the best information available rather than continuing analysis and research in search of the optimum no-risk solution. One thing is clear – without long term heat incentives in the immediate future renewable heat in Northern Ireland will stagnate and cease to grow to achieve its potential. To avoid situations in which you might make mistakes may be the biggest mistake of all. - Peter McWilliams 5.9. The level of support required does not require huge research – the figures are already available from both research papers and commercial growers. BENI would be very willing to assist in this analysis if necessary. By way of example one member and local grower provided the following figures for SRC willow production in 2009.

Assuming an ex-farm sale price of £80 per tonne leaves a margin of £30 per tonne to cover land, planting costs, drying store investment ( at least £1850 per hectare )and the farmers managerial input. Typically 10 – 12 tonne chip is sold per hectare per year which leaves a gross margin of £300 to £360 per hectare per year. Some figures from the 2010 DARD Farm Business Data report provide interesting comparisons –

5.10. At the other end of the supply chain if we allow for transport cost the wood chip can be supplied to the user at around £100 per tonne. This contains in the region of 3,500 kWh of energy per tone, so if compared to heating oil, its heat content is worth about £120 per tonne ( assuming 40 p per litre). 5.11. In short, current returns are insufficient to stimulate large numbers of farmers to change from traditional enterprises, with which they are familiar and have the required skill sets, to invest in biomass energy production. At the same time the cost savings compared to oil are probably marginal in justifying large scale investment, unless the material can be sourced at prices which do not provide adequate return to local farmers. The commercial pressure driving the change to renewable energy is therefore minimal. It is very apparent to us that, in addition to the excellent research, advice and education services provided, if society wishes to stimulate the use of renewable heat with the resulting benefits to the local economy and the world climate, some form of additional financial incentive is essential. The fact that Great Britain is moving towards that goal through a Renewable Heat Incentive, while Northern Ireland does not even have the legislative cover, let alone the methodology to do so, is a matter of grave concern. 6. Best Practice Elsewhere.When looking for best practice and learning from the experience of other countries we would suggest that the Committee review the successful actions taken in Austria, and Sweden. 6.1. In Sweden some 18,000 ha of willow is grown by around 1250 farmers. All this material, is burnt as harvested, without any artificial drying. A high proportion of the salix (willow) crop in Sweden is treated with sewage sludge from local authority treatment works – this provides significant savings over conventional waste water treatment, and additional income to the farmer through payment of a gate fee. The resulting product (wood chip) is then sold back to the municipality for use in district heating systems. These District Heating Systems provide over 50% of all heat use in Sweden and 23% of all Sweden's heat requirements come for bioenergy sources, including sawdust, bark, forest thinning / waste and willow chip. This development was driven by a Government vision supported by strategies including sustained financial incentives. 6.2. In the case of Austria, almost half (47%) of which is covered in trees, so this central European nation has capitalised on these forest resources, to build a sizeable industry in micro scale biomass heating. The Austrian Government has a target of 25% of its primary energy supplies from renewables by 2010 and 45% by 2020. Some regions, such as Upper Austria, are aiming to generate all electricity and heat from renewables by 2030. The International Energy Agency (IEA) attributed the success of biomass in the country to a number of factors, including stable financial incentives, a wide portfolio of proven technologies and a long tradition of using biomass. Research and development in energy technology has a long and strong tradition in Austria, and has been successful in creating world class industries, e.g. for small-scale biomass boilers. Within Austria, the Government has supported biomass systems through subsidies – homeowners can get €800 from the national Government if they opt for biomass heating, or up to €4,500, or 30% of system cost, in some federal states. There are also subsidies for replacing old oil-fired systems with biomass, and large incentives for commercial installations. Pellet systems are rapidly replacing conventional oil heating systems. Pellet systems jumped from 32% of the new installations in 1999 to 76% in 2007.This is partly due to the price of fuel. In September 2008, pellets cost around 3.5 cents/kWh, compared to 6.3 cents for gas and 9.1 cents for heating oil. 7. Conclusion.We hope this information will be helpful to the Committee in considering this important topic. BENI is committed to furthering the development of Biomass Energy in Northern Ireland and sees renewable heat as the simplest and most realistic method of delivering this renewable energy in practice. There is also much focus on extending the gas distribution network within Northern Ireland as a means of developing low carbon heating systems. We would refer to the recently published "Into the West" report from the Energy Saving Trust. The broad conclusions show that there would be significant investment of public funds required with very limited benefit, giving poor value for money. If a fraction of this money was instead used to encourage adoption of renewable heat technologies as well as microgeneration, there would be significant progress towards meeting Northern Ireland's 2020 renewable heat target, as well as helping to address fuel poverty. We will be pleased to provide further assistance if the Committee feels this would be helpful. This includes the opportunity to visit SRC willow crops and processing facilities, as well as renewable heating systems already in operation using locally grown woodchip fuel. John C MartinChairman Tel: 07808 060037 Biomass Energy Northern Ireland Limited Response from Carbon Trust NI No.1

27 September 2010 Dear Jim, Committee for Enterprise, Trade and Investment renewable energy inquiryThank you for the opportunity to comment on the above mentioned inquiry and to contribute to the debate on NI's renewable energy policy. Our submission reflects the experience gained by Carbon Trust working in NI since 2002 and I hope the Committee finds it helpful. The Carbon TrustThe Carbon Trust is a not-for-profit company with the mission to accelerate the move to a low carbon economy. We provide specialist support to help business and the public sector cut carbon emissions, save energy and commercialise low carbon technologies. By stimulating low carbon action we contribute to key UK and NI goals of lower carbon emissions, the development of low carbon businesses, increased energy security and associated jobs. Our vision is the creation of a new, vibrant, low carbon economy – with jobs, wealth and competitive advantage for those that take the lead. The Carbon Trust receives funding from Government including the Department of Energy and Climate Change, the Department of Transport, the Scottish Government, the Welsh Assembly Government and Invest Northern Ireland. In Northern Ireland Carbon Trust activities are part financed by the European Regional Development Fund under the European Sustainable Competitiveness Programme for Northern Ireland. The funding we receive from Invest NI has enabled us to make substantial progress in improving the energy and carbon performance of local businesses as well as catalysing markets for low carbon technologies, products and services. Our key achievements in NI include:

The need for a low carbon transition plan for NI Northern Ireland is heavily dependent on imported fossil fuels for the vast majority of its energy requirements. This dependency poses a number of significant challenges vis-à-vis:

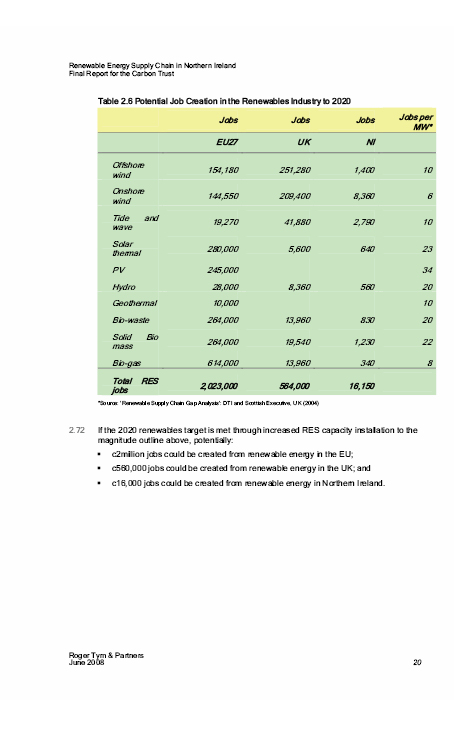

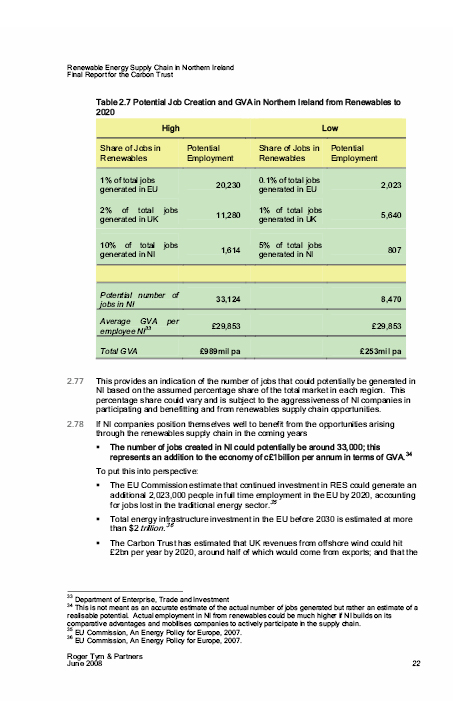

We believe that a rapid move to a low carbon economy must be a strategic imperative for the NI Executive. There are huge incentives for modern economies to decarbonise. For example, wealth generation from the development and supply of low carbon products, goods and services and attracting foreign direct investment into a low carbon region that can offer secure, affordable, indigenous energy supplies. Accordingly, we would encourage the creation of a 'low carbon transition-plan' for NI that addresses all aspects of the move to a low carbon economy, including those relating to the production of renewable energy. Such an approach should facilitate the delivery of efficient and effective policies that currently cut across or impinge on multiple NI Departments. It is likely that the outworking of a 'low carbon transition-plan' will have a very significant impact on many aspects of the NI economy and society. It should therefore be led and promoted by the NI Executive, to ensure that such a plan sought and received the endorsement of key stakeholders, business and citizens. National and international energy and climate change policies will likely result in higher energy and carbon prices in the years ahead and as a region so dependent on imported high-carbon energy supplies, it is imperative that NI quickly develops and implements a plan to mitigate these risks. We believe that such an approach is necessary to ensure that NI's move to a low carbon economy is achieved in the most rapid and cost-advantageous manner possible and in such a way as to maximise the wealth creation opportunities for NI plc through the creation, development and commercial exploitation of low carbon intellectual property and technologies. Targets and objectives set in various Government documents including, the NI Executive's Programme for Government, DETI's Strategic Energy Framework and the Sustainable Development Strategy provide the basis for an encouraging start to putting NI on the path to a low carbon economy. Contribution of renewable energy to the NI economyWe are pleased that the Committee intends to look at the contribution that renewable energy technologies could make to the NI economy. The renewable energy sector - and the low carbon sector more broadly - has been identified as an important growth area by a number of UK and global regional development agencies and one which we believe offers a solid foundation for a forward looking, wealth creating, economic strategy for a region like NI. Northern Ireland already has considerable capability and capacity in a number of key industry sectors which, if strategically managed, could transfer to the low carbon sector. Our natural resources (wind, land, marine) and strategically important infrastructure (e.g. deep-port and cranage facilities), aligned with the internationally recognised talent in low carbon research that resides in both our local Universities, provides the building blocks to enable Northern Ireland to become a significant player in the fast growing clean energy sector - both as a creator of products and services and as an exploiter of the available technologies. However, further work is required to fully understand what NI's distinctive, natural advantage in the low carbon space is and to develop business plans for commercialisation and exploitation. The multi-billion pound investment outlined or implied in the Strategic Energy Framework, in order to meet the 2020 targets and objectives set within it, should be managed strategically to provide a platform for the development of the clean energy sector in NI. This scale of investment is unprecedented and represents a generational opportunity to create jobs and wealth in the clean/sustainable energy space. Accordingly, we believe a 'Legacy Action Plan' should accompany the Strategic Energy Framework detailing the long term imprint the multi-billion investment will leave in terms of wealth, job creation and societal impacts. Renewable energy policy developmentAcknowledging that energy generation from renewable technologies is generally more expensive than from fossil fuels, the Government has introduced a number of policy instruments to effectively incentivise and subsidise the deployment of renewables. In NI, the main mechanism is the NI Renewable Obligation (NIRO) which imposes a target on electricity suppliers to source from renewable generators. We understand that the NIRO has been designed and the profile set with the cost to the NI consumer as a key consideration. This is clearly important in order to protect business and citizens from even higher electricity prices; however it does limit the effectiveness of the NIRO in encouraging an indigenous renewable energy industry. The absence of renewable energy feed-in-tariffs (FITs) and a Renewable Heat Incentive (RHI) in NI (compared to GB and elsewhere) could disadvantage some businesses that wish to deploy renewable energy technologies, however the overall cost of such schemes and their impact on energy costs to consumers must be taken into consideration. We believe that DETI's on-going efforts to ensure that NI consumers benefit from evidenced based policy that efficiently addresses market failures, is a prudent approach. We would further encourage the NI Executive to give consideration to the development of innovative policies that reward companies that deploy renewable energy technologies through, for example, a 'green business rates' mechanism. The planning process is a key aspect to renewable energy development and can add substantial costs and time delays to technically viable projects. Designating geographic areas as 'pre-approved' renewable energy 'zones' could facilitate more rapid and cost effective deployment. Ultimately, the development of renewable energy policy in NI comes down to 'political' will. If the NI Executive were to make the move to a low carbon economy a key strategic and economic priority – and we would encourage them to do so - then smart support measures can be developed that incentivise and reward innovation in this sector. However, low carbon technology development is a 'race' and other countries are working hard across all aspects of renewable energy technologies and some have indigenous markets of scale that allow alignment of policy and technology development. The NI (and indeed, the RoI) energy market is relatively small and efforts should be focussed on those technologies that allow wealth creation through export of skills, intellectual property and renewable technologies. Northern Ireland has some significant skills in off-shore wind, wave and tidal energy, the built environment and is also well placed to grow and exploit biomass energy. We would strongly encourage that the development of renewable energy policies takes place within a wider context of moving NI to a low carbon economy. A sequential approach to decarbonising NI's energy supplies would ensure that cost effective energy reduction measures are implemented through improved energy management, conservation and efficiency thereby delivering savings that could help ease the burden of higher costs resulting from renewables. Making sense of renewable energy technologies: Opportunities for businesses in NIDuring 2008, in order to help local businesses better understand the opportunities provided by renewable energy technologies, we produced a comprehensive guide that explains the key technologies that are available and provides guidance on assessing the suitability of each technology for a particular site. Incorporating local case studies for businesses and organisations that have already chosen to install these technologies, the guide provides numerous real-life examples to help companies appreciate the economics of investing in renewable energy systems. The guide also summarised the key carbon reduction and renewable energy targets that applied at the time of publication (some of which have been upgraded) and concluded that achievement of these targets in NI will be challenging and will require intelligent and effective policy making and regulation to create the right conditions for the significant investment in carbon abatement technologies required. It also reinforces a point made earlier that incorporating renewable energy targets into wider, more holistic carbon reduction efforts will help ensure that they are achieved in the most cost advantageous manner. We attached a copy of the guide for your reference. Renewable energy supply chain opportunities in NIAlso in 2008, we commissioned a piece of work to investigate the commercial opportunities for Northern Ireland businesses to supply a range of goods and services into the renewable energy supply-chain. Key findings from this study included:

However, the study makes clear that there is no guarantee that jobs resulting from the deployment of renewable energy technologies in any given geography will be created in that geography. Many will be created and sustained during the development phase of the technology and will therefore largely be located in the country/region development. We attached a copy of the study report for your reference. We hope you find this short submission helpful and we would of course be happy to elaborate on any of the points raised in our response. Yours sincerely

Carbon TrustGeoff Smyth Response from Carbon Trust NI No.2                                         Response from Carbon Trust NI No.3

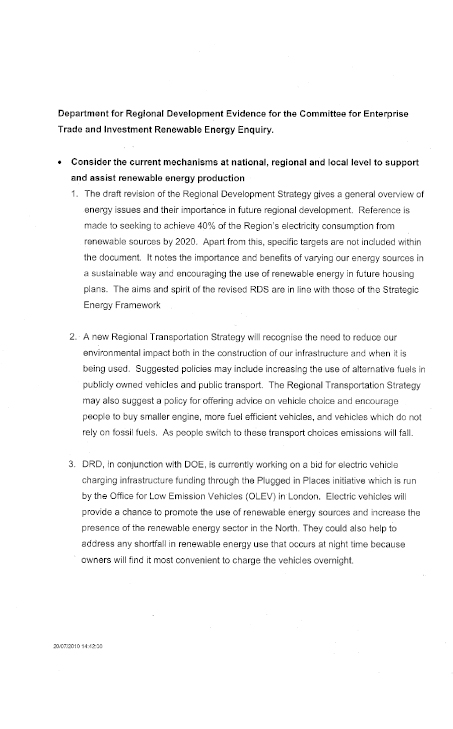

Response from Committee for Regional Development   DRD Response re Inquiry Follow up Questions    Response from Department of Agriculture and Rural DevelopmentPeter Scott Department of Agriculture And Rural Development 17 Dec 2010 Dear Sohui ETI Committee - Renewable Energy InquiryI refer to your correspondence of 6th Dec 2010 requesting additional information in respect of the recent ETI Committee Inquiry. Thank you for this opportunity to provide additional information to support of our evidence. Please find our response attached. Yours sincerely,

Peter Scott DARD Response to ETI Committee Request for Additional InformationAn indicative list of those farms/forestry enterprises meeting their own energy needs.An assessment of interest questionnaire in renewable energy production and usage was commissioned by DARD in August 2008 in conjunction with UFU to ascertain the level of interest in renewable energy within the agricultural sector. Three hundred members of the UFU were surveyed, it must be noted they were not totally representative of the total agricultural sector in NI. There were 85 returns to the survey, all agricultural sectors responded although the main participants in the survey were from the Beef and dairy sectors. The survey revealed 56% of participants indicated a high level of interest in renewable energy production and usage; a further 41% had some interest in the sector. Participants were mainly interested in wind generation at 43% followed by the processing of livestock waste/organic material at 28%. 21% were interested in willow/wood. Subsequently as part of the Renewable Energy Event held at Greenmount in November 2010 of the 700 visitors surveyed to indicate adoption of renewable energy technologies on farm, 50 responded and results are tabulated below

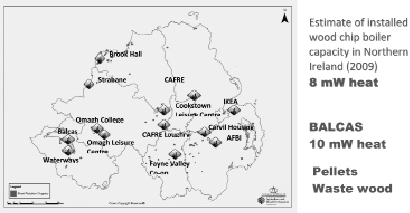

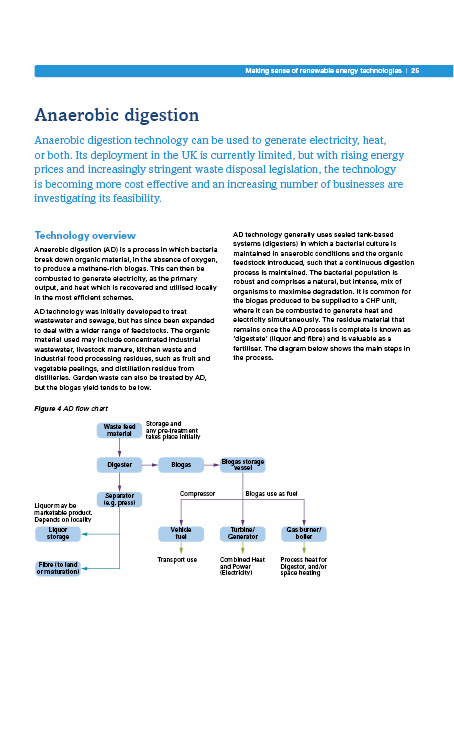

Work will commence in the near future to obtain a wider knowledge of the level of uptake of renewable energy technologies within the land based sector. DARD wish to progress this work during the early part of 2011. A list of any biomass schemes that are currently operational in Northern Ireland.The Biomass Schemes that are operational in NI are mainly for heat purposes and are indicated in the diagram below. The Anaerobic Digester installed at AFBI Hillsborough produces heat and electricity for the Hillsborough site. DARD are not aware of any other Anaerobic digesters currently operational in NI Northern Ireland – Biomass for heat1000 hectares of SRC willows (red dots), 10 ha miscanthus 400 hectares of forest harvested annually 55,000 t of wood pellets manufactured annually

Thanks due to Rural Generation Ltd, Green Energy Ltd and others who supplied information on biomass installations in Northern Ireland A list of those individuals/organisations that have received grants to develop an anaerobic digestion installation.The Anaerobic Digester commissioned at Agri- Food Biosciences Institute, Hillsborough in 2008 received a grant from the Hain Fund 2006. The total amount of funding received by AFBI amounted to £4.2m, which covered the purchase and installation of an Anaerobic Digester and the building and establishment of the Renewable Energy Centre of Excellence at AFBI Hillsborough. DARD have not provided funding for any Anaerobic Digesters to date, however out of 11 Letters of Offer made under the DARD Biomass Processing Challenge Fund, 4 were in respect of Anaerobic Digestion Projects. We have had one declaration of acceptance and are currently awaiting responses from the remaining 3 AD projects. Response from Agriculture and Rural Development No.2Jim McManus 6 January 2011 Dear Jim I refer to you letter of 16 December 2010, seeking DARD's views on a number of queries from the Committee for Enterprise, Trade and Investment in relation to their Inquiry into Barriers to the Development of Renewable Energy Production and its associated contribution to the Northern Ireland economy. Our response is attached at Annex 1. Please contact me should you have any further queries. Yours sincerely,

Liam McKibben cc. Sohui Yim Annex 1Queries arising from DARD oral evidence to the Committee for Enterprise, Trade and Investment's inquiry into barriers to the development of renewable energy production and its associated contribution to the Northern Ireland economy.Q1 Do officials see a role for DARD in supporting the development of a commercial market?A1 DARD's policy is to assist the land based sector to maximise the benefits that exploiting the utilisation and production of renewable energy can offer. Key actions within the Department's 2010 renewable Energy Action Plan aim to encourage the land based sector to become active in commercial markets. As such therefore we see the DARD role as not being to directly support the development of a commercial market but rather to assist the land based sector to participate in that market. Q2 Officials informed the Committee that incentives are provided to grow energy crops, particularly in relation to short-rotation coppice. The Committee would be grateful for full details of all incentives provided by DARD in relation to renewable energy.A2 The following table details current and recent renewable energy incentives provided by the Department.

DARD sponsor a programme of Renewable Energy Research which has been established at the Environmental Renewable Energy Centre at the Agri Food Bioscience Institute's (AFBI) Hillsborough site. The Department's College of Agriculture and Rural Enterprise deliver a programme of training and Knowledge Exchange on Renewable Energy in the land based sector. Q3 Officials informed the Committee that DARD has strengthened its links with the NNFCC. The Committee would like to receive more details of this.A3 As part of the ongoing implementation of the 2010 Renewable Energy Action Plan, DARD have forged links with the National Non Food Crops Centre (NNFCC). This includes working with the NNFCC to provide information specific to Northern Ireland agriculture on the Official Anaerobic Digestion Portal. The website acts as a gateway to a wide range of publically available information on anaerobic digestion from a wide range of sources. The portal can be viewed at www.biogas-info.co.uk . Q4 The Committee would like to receive details of who will sit on the External Stakeholder Group to provide advice to the Department.A4 Membership of the External Stakeholder Group has yet to be finalised. However, Ministerial approval has been agreed to approach 3 people with backgrounds in the land based sector, the renewable energy sector and from the business community from a selected list of knowledgeable and representative individual An informal approach will be made by officials, to confirm availability and willingness to participate. Once the individuals have confirmed agreement to participate we will provide further details to the Committee. Q5 What level of anaerobic digestion will be required to enable Northern Ireland to fully meet its obligations under the Nitrates Directive in the long term?A5 The total quantity of nitrogen that is in the input feedstock to an anaerobic digester is still in the output digestate. Therefore, the AD process has little direct impact on the 170kg total organic N/ha limit imposed by the Nitrates Directive. However, to ensure sustainability, AD must include management of the plant nutrients in digestate. This will involve ensuring that there are sufficient spread lands available for nutrient utilisation from digestate. Please note that there are many positive advantages of AD that are not associated with the Nitrates Directive. Response from Department for Employment and Learning No.1 Response from DELAppendix 1Enterprise, Trade and Investment Committee Inquiry into Renewable EnergyEvidence from the Department for Employment and Learning (DEL)Contents1. Summary of the Department's vision and values and key areas of activity 2. The context of the Department's work 3. The relevance of DEL work by business area to the development of renewable energy production and associated contribution to the Northern Ireland economy Department for Employment and Learning (DEL)1 Vision and Values DEL's vision is: A dynamic, innovative and sustainable economy where everyone achieves their full potential. DEL's aim is: To promote learning and skills, prepare people for work and to support the economy. DEL's purpose is: To unlock the talent inherent in the people in our community and enable them to make the most of their potential. By helping people to find work, upskilling the workforce, supporting employment rights, innovation and creativity and making education and training accessible, DEL can create the dynamic and innovative economy that lies at the heart of the aims of the Programme for Government. The Department bases its work on a number of key values, which underpin the delivery of its commitments. The Department will seek to provide a professional and responsive service to its customers in an equitable way. It will strive to be innovative and dynamic and to improve continually as an organisation whilst motivating, developing and valuing its staff. Underpinning the work of the Department is its commitment to develop and manage a framework of employment rights, remedies and responsibilities to ensure that those in work are adequately protected. Context The Department's key areas of activity include:

These areas of activity are relevant to the renewable energy sector as described below 3. DEL and Renewable Energy activity 3.1 Support for Skills Development in the Renewable Energy SectorSkills are an essential element in the combination of actions required to improve productivity and enhance our economy. Renewable energy is increasingly considered to be an area which could contribute to economic growth. It is therefore important that the right skills are developed to support this growth. 3.2 Funding of Sector Skills Council (SSC) projects.It is the role of SSCs to work with employers to identify current and future skills needs, and to develop training solutions to meet those needs. A number of SSCs (including Energy & Utility Skills, Summit Skills, Construction Skills working with Action Renewables) involved in renewable energy activities have already grouped together in a Cross Sector Renewables Group to identify the training needs that will help companies accelerate their growth in this emerging industry. Funding has been provided for a range of projects including: developing labour market intelligence in respect of wind energy; review of existing training material being used to deliver installer training for solar, wind, biomass and heat pumps; and the development of a qualification for architects, designers and specifiers of renewable energy technologies. As a result of the work of the group, both plumbing and electrical apprenticeship frameworks in Northern Ireland now incorporate renewable technologies. 3.3 Further EducationThe Department does not provide direct or specific assistance to businesses in relation to renewable energy but Further Education (FE) Colleges offer a range of provision and support that may assist businesses in this area: Further Education CoursesFurther Education (FE) Colleges provide a range of courses in support of the green economy, and which may assist SMEs in developing renewable energy production/technologies, equipping them with the skills required. Courses cover topics such as solar energy, sustainable business practices, responsible sourcing of materials, biomass heating systems, and wind turbine specification and installation. Carbon Zero NIThe Department has provided time -limited funding for the development of an FE Sector-wide approach to sustainability, led by South West College. The Carbon Zero NI project aims to:

InnoTech CentreSouth West College's InnoTech Centre, is a business and mentoring support hub providing a range of services in sustainability, design, electronics and software. The overall aims of the InnoTech project are to:

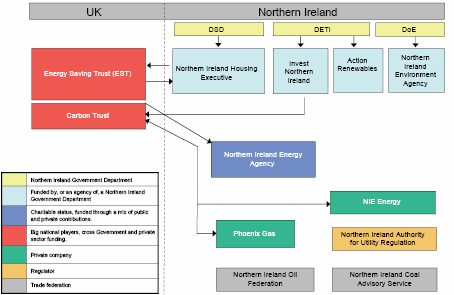

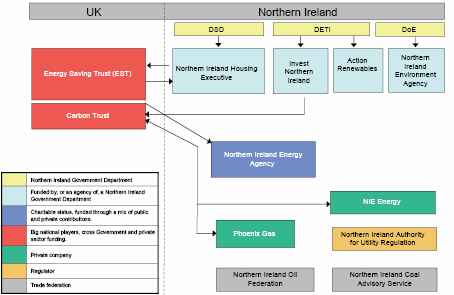

In years 1 and 2 of the project (2008-2010), the InnoTech Centre provided support for a wide range of businesses involved in renewable energy, with a focus on providing bespoke support, including: advice on wind turbine systems; anaerobic digestion and heat exchanger design; and the development of a bioethanol fuel project. Guidance to Colleges from the DepartmentThe Department issued guidance to the FE Sector on promoting Sustainable Development in January 2009. This guidance encouraged FE Colleges to develop curricula that enabled students to develop the skills and knowledge which would contribute to sustainable development. Colleges were required to put in place Sustainable Development Action Plans/Strategies in order to assess their current sustainable development status and establish ways to further improve performance in this area. 3.4 Higher EducationFunding to support renewable energy research projects in Northern Ireland universities fall within 4 broader funding streams: Quality-related Research FundingAt the request of the Minister, the Department has directed some £2m (5%) of Quality-related Research (QR) funding to the local universities, in both the 2009/10 and 2010/11 academic years, to focus on new projects which encompass the theme of sustainability and align towards research which relates to alternative/renewable energy sources or green technology. QR funding, which is paid by way of block grant, is used to support the research infrastructure necessary for the Northern Ireland universities to conduct research. Queen's University Belfast (QUB) has allocated the sum of £1.27m from this funding towards a project entitled "Clean Energies" where the research focuses on improving energy efficiency, the development of new, renewable, energy sources and integrating them within a more flexible and efficient power distribution system. Strengthening the all-Island Research Base initiativeAs part of its "Strengthening the all-Island Research Base" initiative, a programme aimed at developing and/or strengthening links with research groups in the Republic of Ireland through collaborative research which is socially and economically relevant to Northern Ireland and to the island as a whole, the Department is providing grant of £1.54m to the University of Ulster (UU), between 2008 and 2011, to support an "Energy Storage" project being undertaken in collaboration with University College Dublin, the National University of Ireland (Maynooth) and Dublin Institute of Technology. The project is concerned with demonstrating how energy storage can be incorporated within the built environment to reduce the use of fossil fuels. ConnectedThe Department is also supporting the development of a number of strategically important "sector specific" projects from its "Connected" programme, an initiative which enables the HE and FE sectors to identify and meet, in a coordinated and holistic fashion, the knowledge transfer needs of businesses, in particular, and the wider community. Two of these projects relate to the green economy arena: the Renewable Energies Foundation Degree programme at Belfast Metropolitan College (BMC) and UU, which aims to provide knowledge transfer and support to staff from BMC in the area of renewable energies; and the "Hydrogen Economy" programme, involving collaboration between UU and three regional colleges (South West, South Eastern and North West) in order to provide the latter with an opportunity to gain an insight into emerging technologies within the renewable energy sector. Science Research Investment FundIn addition, the Department has previously supported "green economy" research through its Science Research Investment Fund (SRIF) initiative, a funding stream set up to address a historic backlog of upgrading and updating of the physical university research infrastructure across the UK and to assist the Northern Ireland universities to operate on a sustainable basis. As part of the funding available through Round 2 (2004-06) of this initiative, some £798k was allocated to QUB for the development of a Coastal Science & Engineering Centre to engage in research on wave energy and coastal engineering. Current PositionThe Department has recently decided to appoint a lead official to co-ordinate sustainable energy skills support activities, working with external bodies and key stakeholders. The first step in this process will be to commission a focused skills study on sustainable energy, assessing current provision, identifying gaps in provision and highlighting best practice in other regions / countries. 3.5. DEL's CommitmentThe Committee will wish to be aware that the Department for Employment and Learning is fully committed, within the context of its core business, to support renewable energy through our support for skills development, education and research.  Response from Department of Employment and Learning No.2 Letter from Minister re Sustainable Energy Communication in NI           Annex ADiagram mapping some of the key stakeholders involved in communication in NI |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

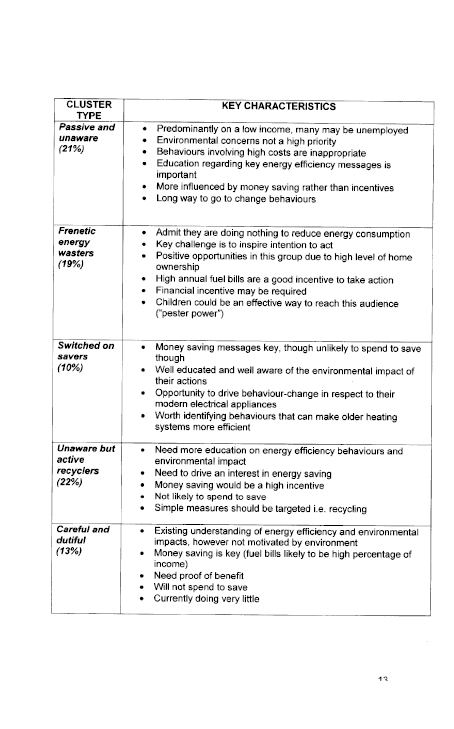

| Cluster | Target Behaviour | Direction for key message | Tools to use (existing and new) | targeted messages |

Likely lead Department |

| City Greens (15% of population) |

Spreading the word about taking positive action | Help your friends and family to take control of their energy usage | Internet site | "Smart energy use saves the environment and saves you, your friends and your family money." | DSD and DETI |

| Passive and unaware (21%) |

Learning to use what they have better rather than "switching off and freezing" | Smart energy use can save you money | Home visits, call centres, drop in centres | "Take control of your boiler. Turn it down not off. That's saving you money and being energy smart." "Take control of your heating. If you're out, turn if off. That's saving you money and being energy smart." | NI Housing Executive |

| Frenetic energy wasters (19%) |

Getting children to help engage parents in energy saving activities/ engaging the family unit in undertaking energy saving activities together. | Encouraging families to engage in energy saving behaviours together | Schools programmes, internet site | "Energy smart families take control together. The less energy you use the more money you save." | DSD and DETI |

| Switched on savers (10%) |

Action to reduce energy wastage from modern appliances | New technology can be a wasteful as traditional appliances | Internet site | "Take control of the hidden costs of new technology. If the red light is on – it's costing you money." | DSD and DETI |

| Unaware but active recyclers (22%) |

Learning how to maximise usage of central and local heating solutions | Need to create a mental link between saving money and energy use in order to drive behaviour change | Call centres and drop in centres | "Taking control of all the energy you use in your home can save you money. That's being energy smart." | DSD |

| Careful and dutiful (13%) |

Learning to use what they have better rather than "switching off and freezing" | Informing this cluster that there are choices beyond on and off; smart choices | Call centres and drop in centres | "Take control. Find the best heating solutions for your budget and your health. Be energy smart." | DSD |

COI research was gathered from the following sources:

Other sources were reviewed but information was not extracted for analysis at this stage due to lack of relevance to the research objectives.

Department of Enterprise, Trade and Investment

Statutory Consultation on a Bioenergy Action Plan for Northern Ireland 2009-2014

Renewable Energy Inquiry

Stimulating

Innovation

Enterprise and

Competitiveness

| Section | Title | Page number |

| A. | Government Strategy for Renewable Energy | |

| 1. | Strategic Context | |

| 2. | Energy supply in Northern Ireland

|

|

| 3. | Renewable energy

|

|

| 4. | Renewable electricity

|

|

| 5. | Heat/renewable heat

|

|

| 6. | Heat and electricity

|

|

| 7. | Renewable electricity incentivisation

|

|

| B. | Economic Development Opportunities from Renewable Energy | |

| 8. | Economic development opportunities from renewable energy

|

|

| C. | Communications | |

Communications

|

||

| Annex A | Relevant PFA/PSA targets and corporate plan targets | |

| Annex B | Executive Summary of work to establish renewable electricity targets | |

| Annex C | Executive Summary of work on heat and renewable heat | |

| Annex D | Summary of energy responsibilities of other departments | |

| Annex E | Onshore SEA scoping report | |

| Annex F | Draft Offshore Renewable Energy Strategic Action Plan | |

| Annex G | Draft Bioenergy Action Plan | |

| Annex H | Geothermal: summary of barriers | |

| Annex I | Current banding levels under the NIRO | |

| Annex J | Communications summary paper |

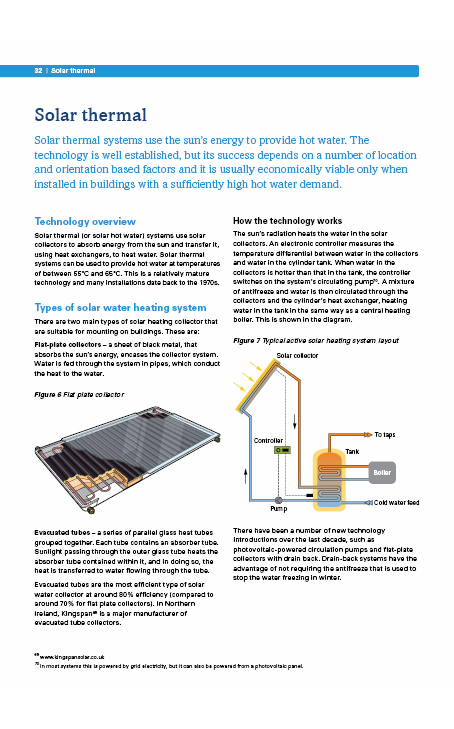

1.1 The Department of Enterprise, Trade and Investment (DETI) is responsible for over-arching energy policy in Northern Ireland[1]. This overarching energy policy was first determined through the Strategic Energy Framework of 2004. In the light of the changing world focus on tackling climate change, as well as the need to address concerns around security of energy supply and wider economic development, DETI has been developing a new energy framework for Northern Ireland in collaboration with internal and external stakeholders, and after full consultation.