Session 2008/2009

First Report

COMMITTEE FOR ENTERPRISE, TRADE AND INVESTMENT

Report on the Committee's

Inquiry into the Role and

Potential of Credit Unions in

Northern Ireland

TOGETHER WITH THE MINUTES OF PROCEEDINGS OF THE COMMITTEE

RELATING TO THE REPORT, WRITTEN SUBMISSIONS,

MEMORANDA AND THE MINUTES OF EVIDENCE

Ordered by The Committee for Enterprise, Trade and Investment to be printed 5 February 2008

Report: 05/08/09R (Committee for Enterprise, Trade and Investment)

This document is available in a range of alternative formats.

For more information please contact the

Northern Ireland Assembly, Printed Paper Office,

Parliament Buildings, Stormont, Belfast, BT4 3XX

Tel: 028 9052 1078

Membership and Powers

Powers

The Committee for Enterprise, Trade & Investment is a Statutory Committee established in accordance with paragraphs 8 and 9 of the Belfast Agreement, Section 29 of the Northern Ireland Act 1998 and under Assembly Standing Order 46. The Committee has a scrutiny, policy development and consultation role with respect to the Department for Enterprise, Trade & Investment and has a role in the initiation of legislation.

The Committee has power to:

- Consider and advise on Departmental Budgets and Annual Plans in the context of the overall budget allocation;

- Approve relevant secondary legislation and take the Committee stage of relevant primary legislation;

- Call for persons and papers;

- Initiate inquiries and make reports; and

- Consider and advise on matters brought to the Committee by the Minister for Enterprise, Trade & Investment.

Membership

The Committee has 11 members, including a Chairperson and Deputy Chairperson, and a quorum of five members.

The membership of the Committee is as follows:

- Mr Mark Durkan (Chairperson)

- Ms Jennifer McCann (Deputy Chairperson)*

- Mr Paul Butler**

- Mr Leslie Cree

- Mr Simon Hamilton

- Dr Alasdair McDonnell

- Mr Alan McFarland

- Mr Gerry McHugh

- Mr Sean Neeson

- Mr Robin Newton

- Mr Jim Wells***

* With effect from 20 May Ms Jennifer McCann replaced Paul Maskey as deputy chairperson.

** With effect from 20 May Mr Paul Butler replaced Mr Paul Maskey.

*** With effect from 15 September 2008 Mr Jim Wells replaced Mr David Simpson.

Table of Contents

Report

Executive Summary

Summary of Recommendations

Introduction

Key Issues and Findings

Options for Change

Conclusions

Appendix 1

Appendix 2

Appendix 3

List of written submissions to the Committee

Appendix 4

Written submissions to the Committee

Appendix 5

List of witnesses who gave evidence to the Committee

Appendix 6

Appendix 7

Appendix 8

List of other evidence considered by the Committee

Appendix 9

Other evidence considered by the Committee

Appendix 10

Purpose of the Inquiry

1. The regulatory arrangements in Great Britain (GB) and in the Republic of Ireland (RoI) allow credit unions in those jurisdictions to provide a much wider range of services to their members than credit unions in Northern Ireland are permitted to offer. The Inquiry was set up to examine the role of credit unions within the communities they serve, to identify the barriers that are preventing credit unions here from offering a wider range of services and to consider how the potential can be unlocked to permit credit unions to expand their range of services and to support them in so doing.

The Credit Union Movement in Northern Ireland

2. The credit union movement in Northern Ireland dates back to the 1960s. There are currently 181 credit unions here serving over 400,000 members. There are two main representative bodies which look after the interests of credit unions. These are the Irish League of Credit Unions and the Ulster Federation of Credit Unions.

3. Credit unions here provide core savings and loan services within limits prescribed by the Department for Enterprise, Trade & Investment (DETI) Companies Registry and which are subject to re-evaluation and change from time to time. Limits include size of individual share holding; size of deposits for those under 16 years of age; dividends payable; amount of loan advances; and percentage of loan interest chargeable.

4. Following concerns raised by the two representative bodies, the Enterprise Trade & Investment Committee (the Committee) commissioned further research into the issue and subsequently decided to undertake this Inquiry.

Expansion of the Range of Credit Union Services

5. In addition to being able to offer the services that can be offered by credit unions in Northern Ireland, credit unions in GB can offer a much wider range of services including current accounts, internet and telephone banking, electronic transfer of wages, Automated Teller Machines (ATMs), insurance, discount services, debit cards, mortgage, bill payment, direct debit, standing orders and junior savings accounts. There is strong support from the credit union movement for the proposal that credit unions in Northern Ireland should be allowed to expand their range of services to cover at least those services which credit unions in GB are able to offer. This viewpoint is strongly supported by the Committee. The Committee believes that, as a first step, credit unions here should be permitted to expand their range of services to include, at the very least, those services which credit unions in GB can currently offer (Recommendation 1).

6. In addition to being able to offer the services available to credit union members in GB, the credit union movement in Northern Ireland strongly advocates the opening up of membership to include joint accounts and group membership of credit unions. There is also strong support for credit unions that would like to reinvest assets into community development and community enterprises.

Credit Union Registration and Regulation

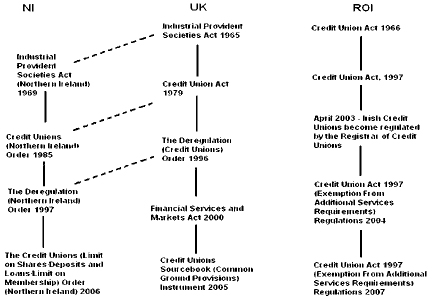

7. Many of the barriers to the expansion of credit union services here result from the way in which credit unions are regulated. Credit Unions in Northern Ireland are registered with and regulated by DETI Companies Registry under the Credit Unions (Northern Ireland) Order 1985. Credit Unions in GB are registered with and regulated by the Financial Services Authority (FSA) and, since July 2002 have come under the Financial Services and Markets Act 2000 (FSMA). As such, credit unions in GB can offer a wider range of services. Credit Unions in Northern Ireland are prohibited from offering services which come under the scope of the FSA to regulate. It is important to note that registration is seperate from regulation. Credit unions are required to register so that members can be assured that their credit union is governed by the provisions of the appropiate credit union legislation. Regulation relates more to the process of ensuring that credit unions are being managed robustly, including the fair treatment of members, within legislative requirements and the regulators guidelines.

8. The Committee considered a number of options in order to address this disparity. Not least of these was the option of the FSA delegating responsibility for the regulation of credit unions to DETI Companies Registry. The Committee found a lot of support for this option across the credit union movement including from both representative bodies and also from the British Bankers Association (BBA). However, the key stakeholder in the delegation process, the FSA, was wholly opposed to the delegation of its responsibilities. For this reason, the Committee felt that it was not in a position to recommend the option as it had little likelihood of success.

9. The Committees recommended option is for the registration of all credit unions in Northern Ireland to remain within DETI Companies Registry and for regulation of all credit unions in Northern Ireland to move from DETI Companies Registry to the FSA in order to deliver the services outlined above (Recommendation 2). The Committee endorses this option as a key element in a 'package of measures which together are designed to support the credit union movement in Northern Ireland to embrace change, to expand their services and to operate under the new regime. This package of support is outlined in the next section.

10. In making this recommendation, the Committee acknowledges that many individual credit unions are content with current regulatory arrangements and have no desire to expand the range of services they offer. The Committee is reassured in this regard, by evidence from the Association of British Credit Unions Ltd (ABCUL) coupled with assurances from the FSA, that the 'lighter touch Version 1 FSA regulation provided to credit unions that wish to provide only core services will meet the needs of these credit unions, whilst allowing others to expand under the FSAs Version 2 regulation.

11. The Committee sees the establishment of an FSA presence on the ground in Northern Ireland as key to the success of regulatory changes and expansion of credit unions services (Recommendation 3). Credit unions have an excellent working relationship with DETI Companies Registry which cannot possibly be mirrored by an organisation operating from London or Edinburgh. In order to successfully bring about the changes proposed, credit unions will need hands-on support from the FSA on a regular basis and the FSA will need time and hands-on involvement to get to know the credit union movement in Northern Ireland.

12. The continuing involvement of DETI Companies Registry would be helpful in assisting with the changeover process. DETI staff have a good working relationship with and a high level of understanding of the credit union movement.

Package of Support to Bring About Change

13. Changing from the current regulatory regime to the FSA regime will require credit union management and staff to train in the operation of the new procedures and in the provision of additional services where they decide to provide such services. For this training to be successful it will require close co-operation between the credit union movement and the FSA, supported by DETI, in the development and delivery of training programmes (Recommendation 4).

14. Changes to regulation and expansion of services will require investment in the credit union movement. The Committee recommends that a package of financial support is made available to credit unions in Northern Ireland to assist with the transitional and developmental costs associated with this change. This should include funding for training and development as well as funding for investment in new technology and equipment required (Recommendation 5).

15. The Growth Fund is part of Treasurys Inclusion Fund and is available to credit unions in GB which are regulated by the FSA. The Committee considers it reasonable that the Treasury, in taking on responsibility for regulating credit unions in Northern Ireland under the authority of the FSA, extend the Growth Fund to include Northern Ireland credit unions (Recommendation 6).

Group Membership of Credit Unions

16. There is very strong support across key stakeholders and little or no opposition to the idea that credit unions should be able to open up membership to include joint accounts and corporate accounts. This would enable couples and voluntary and community groups to open accounts in credit unions. Such a move would provide additional support for credit unions and would help small voluntary and community groups to avoid, what they may see as, excessive bank charges. The Committee sees this as being beneficial for credit unions, for their members and for the communities they serve. This facility is not yet available in GB, however HM Treasury is currently undertaking a review of relevant legislation there and it intends to consider the implications for credit unions in Northern Ireland. The Committee has recommended that credit union membership is opened up in this way as quickly as possible after the new regulatory arrangements are put into place (Recommendation 7).

Reinvestment of Assets

17. The Committee is in agreement with both credit union sponsor bodies, that the appropriate reinvestment of assets by credit unions into community development and community enterprises can bring significant benefits to communities. This can only be successfully achieved within the context of appropriate training in the intricacies of the skills and competencies required in this field, as highlighted by both the FSA and the BBA. It is therefore recommended that the FSA work with the credit union movement to assist in the development of the knowledge and skills required for credit unions to become involved in the reinvestment of assets in community development and community enterprises (Recommendation 8).

Summary of Recommendations

1. The Committee recommends that credit unions are permitted to expand their range of services to include, at the very least, those services which credit unions in GB can currently offer.

2. It is recommended that registration of Northern Ireland credit unions remains within DETI Companies Registry but that regulation of credit unions in Northern Ireland should move from DETI Companies Registry to the FSA to enable credit unions to deliver a wider range of services. This should be part of a package of interdependent measures to enable credit unions in Northern Ireland to offer a wider range of services to members. As credit unions will require additional support to introduce change and to operate under the new regime, the package of measures should include recommendations 3 to 6 in this Report.

3. In order to fully assist the Northern Ireland credit union movement to embrace the considerable change brought about by both a change in regulatory arrangements and the expansion of services and to assist in the maintenance of those services, it is recommended that the FSA open an office in Northern Ireland. This office should be staffed by people with an understanding of the credit union movement and the regulatory arrangements in place for credit unions. In order to ensure that FSA staff in Northern Ireland have a full understanding of the credit union movement in Northern Ireland it may be helpful to the FSA to apply to second staff from DETI Companies Registry in order to utilise their experience during the transition period. This would assist in the implementation of changes and in embedding the new regulatory arrangements and expanded range of services.

4. It is recommended that both DETI and the FSA work with the credit union movement to develop and implement training programmes to provide credit union staff with the knowledge and skills to operate the new regulatory arrangements and to operate additional services which credit unions are permitted to provide.

5. The changeover to the new regulatory regime and the expansion of credit union services will bring additional costs for credit unions relating both to the transition to the new regulatory regime and to the development of new services . It is recommended that DETI and the FSA work with the credit union movement to fully identify staffing, training and technology & equipment costs and to agree with HM Treasury a package of financial support to assist credit unions in implementing changes.

6. In order to bring Northern Ireland into line with funding already available to credit unions in GB, it is recommended that the Growth Fund, and any future such funding, be extended to include credit unions here.

7. It is recommended that membership of credit unions be extended to include joint accounts and group membership. The Committee understands that these facilities are not yet available to credit unions in GB, but believes that they should be introduced as quickly as possible after the new regulatory arrangements are put into place. The Committee cautions that care should be taken in developing the legislation and procedures for such arrangements so as to ensure that organisations such as commercial or speculative enterprises, which are not wholly compatible with the ethos and values of credit unions, are excluded. Such a move would be of benefit to GB credit unions as well as those in Northern Ireland.

8. The Committee believes that the appropriate reinvestment of assets by credit unions into community development and community enterprises can bring significant benefits to communities. It is therefore recommended that the FSA work with the credit union movement to identify the knowledge and skills required to successfully undertake such a task and to develop the appropriate training and structures to implement, monitor and evaluate the reinvestment of a proportion of assets by credit unions in the communities they serve.

Introduction

Background

1. The credit union movement in Ireland dates from the 1950s[1]. The first credit unions in Northern Ireland were formed in the 1960s and were operated and run as unincorporated clubs and associations[2]. The Credit Unions (Northern Ireland) Order 1985 put in place a specific statutory framework to facilitate the development and growth of the credit union movement.

2. There are two main representative bodies for credit unions in Northern Ireland. The Irish League of Credit Unions (ILCU) and the Ulster Federation of Credit Unions (UFCU). Founded in 1960, the ILCU is the larger of the two representing 525 member credit unions throughout Ireland, including 104 in Northern Ireland[3]. The UFCU was formed in 1995 and currently represents 51 member credit unions in Northern Ireland. Both the ILCU and the UFCU operate their own non-statutory and independently controlled savings protection schemes. There is a third, smaller representative body, the Tyrone Federation, which represents 13 Credit Unions in Northern Ireland. An additional 13 credit unions in the region operate totally independently. The profile of the credit union movement in Northern Ireland is summarised at Table 1.

Table 1. - Profile of the Credit Union Movement in Northern Ireland

Affiliation |

Credit Unions |

Members |

Shares |

Loans |

Net Assets |

|---|---|---|---|---|---|

ILCU |

104 |

350,000 |

£627m |

£430m |

£737m |

UFCU |

51 |

23,000 |

£24m |

£11m |

£28m |

Tyrone Federation |

13 |

10,000 |

£23m |

£8m |

£25m |

Other |

13 |

25,000 |

£26m |

£19m |

£30m |

Total |

181 |

408,000 |

£700m |

£468m |

£820m |

Source: 2006 AR 25 Annual Returns to Registrar[4]

3. In Northern Ireland, credit unions are registered with and regulated by the Registrar of Companies, Credit Unions and Industrial & Provident Societies within the DETI. In GB both registration and regulation of credit unions transferred in 2002, from the Registry of Friendly Societies to the FSA. In 2003 regulation of credit unions in the Republic of Ireland transferred from the Registrar of Friendly Societies to the Registrar of Credit Unions under the Financial Regulator. It is important to note that registration is seperate from regulation. Credit unions are required to register so that members can be assured that their credit union is governed by the provisions of the appropiate credit union legislation. Regulation relates more to the process of ensuring that credit unions are being managed robustly, including the fair treatment of members, within legislative requirements and the regulators guidelines.

4. These changes in GB and RoI have enabled credit unions in these jurisdictions to provide a wider range of services than can currently be offered in Northern Ireland. In Northern Ireland, the credit union movement provides core savings and loans services within the following prescribed limits[5]:

- Size of individual shareholding - £15,000 or 1.5% of total shareholding which ever is greater;

- Deposits up to £10,000 for those under 16;

- Dividends - maximum of 8% per annum;

- Loans advances up to £15,000 (For 'deregulated credit unions the limit is the lesser of 1.5% of total share capital or 20% of the general reserve);

- Loan interest up to a maximum of 1% per month on a declining balance basis.

5. The regulatory regimes in GB and RoI permit credit unions to provide additional services over and above those core services. Such services are not open to credit unions in Northern Ireland to provide. For example, in GB appropriately approved credit unions may act as Child Trust Fund (CTF) providers. In both GB and RoI credit unions may provide tax-advantaged savings such as an Individual Savings Account (ISA) and may also undertake other regulated activities such as insurance and mortgage services.

6. Following concerns raised by the ILCU and UFCU, the Committee commissioned further research into the issue and subsequently agreed the Terms of Reference and decided to proceed with the Inquiry at its meeting on 13th March 2008.

Terms of Reference for the Inquiry

7. The terms of reference for this inquiry were:

- Assess the current ethos, regulation and legislation of credit unions in Northern Ireland and compare these with provisions in Great Britain and Republic of Ireland;

- Compare the different services available to credit union members in Northern Ireland, Great Britain and the Republic of Ireland;

- Assess the role and contribution of credit unions in promoting the financial well-being of their members and wider community;

- Examine the legal and regulatory barriers preventing credit unions from participating in the 'business of banking and promoting financial inclusion;

- Compare the role and availability of public funding available to credit unions in Great Britain, Northern Ireland and the Republic of Ireland;

- Examine what policy development and practices have taken place since the Review of Credit Unions;

- Assess the Treasury Select Committee recommendations on credit unions; and

- Report to the Assembly on the Committees analysis and conclusions in relation to the above and make relevant recommendations.

Committee Approach to the Inquiry

8. The Committee recognises the close links between individual credit unions and the communities they serve. It also recognises the unique contribution made by the credit union movement to tackling financial exclusion through the provision and promotion of services in areas where members of communities may otherwise find it impossible to avail of any financial services. For this reason, the Committee considers it essential to explore ways in which credit unions can provide a wider range of services to those who may otherwise be financially excluded or who may, for various reasons, find themselves drawn into the path of commercial or, sometimes illegal, 'doorstep lenders charging exorbitantly high rates of interest.

9. The Committee is committed to the achievement of an outcome whereby members of credit unions in Northern Ireland are, at least, able to avail of the same opportunities and services as members of credit unions in GB. This commitment has underpinned the Committees approach to this Inquiry and forms the basis of the Inquirys recommendations.

10. In commissioning the Inquiry, the Committee recognised that there is a wide range of stakeholders with varying degrees of interest in the outcome of the Inquiry. This included those with a vested interest such as the ILCU, UFCU, individual credit unions and their members; regulatory authorities, namely the FSA and DETI Companies Registry; organisations representing the public such as the advice sector and the Consumer Council; potential competitor organisations such as banks, building societies and their representative bodies; as well as stakeholders in GB and RoI where services provided by credit unions are closer to what the Committee would like to see in operation in Northern Ireland.

11. In order to obtain and explore the views of a wide range of key stakeholders, the Committee placed notices in the local press seeking the views of interested parties and wrote to key stakeholders to obtain written submissions outlining their views. Research papers were commissioned to inform the Committees position and oral evidence was taken from a range of key stakeholders. In analysing the evidence provided, the Committee developed a number of options based on key stakeholder findings. These options were further analysed and a preferred option agreed along with a number of key recommendations to assist in the implementation of the preferred option.

12. In the course of the Inquiry, the Committee was made aware that HM Treasury intend to conduct a review of credit unions and industrial and mutual societies in Northern Ireland. While the regulation of industrial and mutual societies is outside the term of reference for this Inquiry, the Committee recognises that any changes to the arrangements for the regulation of credit unions here will raise issues for DETI in relation to the regulation of other bodies.

13. The Committee would like to express its appreciation to all those who provided written submissions to the Inquiry and to those who attended to provide oral briefings to the Committee.

Key Issues and Findings

Comparative Analysis of Credit Unions in Northern Ireland with GB and RoI

14. The ethos of the credit union movement in Northern Ireland is considered unique with a number of important founding principles which are summarised as follows[6]:

- Promoting thrift and financial awareness among the membership with an emphasis on community based self-help;

- Providing credit for the benefit of members at a fair and reasonable rate of interest;

- Membership restricted to those who meet the 'common bond qualification, usually based on geographical area or employer;

- Strong democratic decision making process, based on one-member-one-vote irrespective of size of shareholding;

- Volunteer culture - credit union board members largely perform their duties on a voluntary basis and without payment.

15. The ILCU believes the ethos of the credit union movement is well articulated by Rule 4 of the standard rules for credit unions, namely:

The objects for which the credit union is formed are:

(a) the promotion of thrift among its members by the accumulation of their savings;

(b) the creation of sources of credit for the benefit of its members at a fair and reasonable rate of interest;

(c) the use and control of members savings for their mutual benefit; and

(d) the training and education of members in the wise use of money and in the management of their financial affairs.[7]

16. Credit unions in Northern Ireland provide a core service of savings and loans to members. They do so under specific permission granted under the FSMA and within the following prescribed limits:

- Size of individual shareholding - £15,000 or 1.5% of total shareholding which ever is greater;

- Deposits up to £10,000 for those under 16;

- Dividends - maximum of 8% per annum;

- Loans advances up to £15,000 (For 'deregulated credit unions the limit is the lesser of 1.5% of total share capital or 20% of the general reserve);

- Loan interest up to a maximum of 1% per month on a declining balance basis.

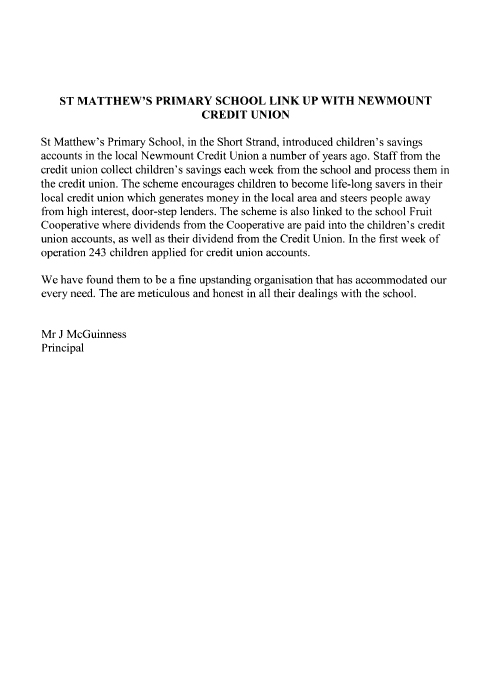

17. The benefits credit unions bring to local communities have been further highlighted by a number of respondents to the Inquiry. For example, St Mathews Primary School draw attention to credit union schemes with schools which encourage children to become life-long savers and provide a realistic alternative to doorstep lenders[8]. In its written response to the Committee, the Committee for OFMDFM stress the constructive role of credit unions in assisting families on low income to manage finances as identified in their recent Inquiry into child poverty[9]. The written submission from Housing Rights to the Committee also highlighted the positive contribution made by credit unions to promoting financial inclusion[10].

18. There are currently 181 credit unions in Northern Ireland with around 408,000 members and assets totalling approximately £820 million. Citizens Advice indicates that credit unions are considered a trusted brand in Northern Ireland[11]. This view is supported by the Consumer Council which states that credit unions:

play an increasingly important role in delivering public services, widening choice for consumers and contributing to the economic, social and cultural well-being of NI[12]."

19. Advice NI considers it vital that credit unions in Northern Ireland retain the ethos as a community provider of services to members and does not become like high street banks. It does, however recognise that the extension of services would benefit both communities and individuals[13]. The Rural Development Council (RDC) supports this view, stating that expanding the services which credit unions were able to offer would improve rural communities access to financial services[14].

20. As stated earlier, credit unions in Northern Ireland are regulated by the Registrar of Companies, Credit Unions and Industrial & Provident Societies within DETI. The Registrar maintains contact with the credit union movement through regular meetings with each of the two main representative bodies and with a user group comprising direct membership from individual credit unions including those that are unaffiliated. There is no single independent complaints body for members to bring complaints to about credit unions. DETI Companies Registry can only consider whether a complaint has breached legislation. In England and Wales, as credit unions are regulated by the FSA, members can lodge complaints to the Financial Ombudsman if they are not content with the way their complaint has been handled[15].

21. In Great Britain there are about 560 credit unions with around 500,000 members and assets totalling approximately £500 million. They range in size from large, professionally run high street operations to small community-based credit unions run from community halls. Credit unions operate in areas of economic and social disadvantage, offering an affordable alternative to 'doorstep credit and lending to people who would otherwise be financially excluded. The Deregulation (Credit Unions) Order 1996 amended the terms of the Credit Unions Act 1979, extending the notion of common bond, increasing share holding limits, introducing secured loans and relaxing borrowing limits. Credit Unions in GB can now provide members with current accounts, internet and telephone banking, electronic transfer of wages, ATMs, insurance, discount services, debit cards, mortgage, bill payment, direct debit, standing orders and junior savings accounts[16].

22. The FSA states that it is possible to discern two different models for credit unions in GB; one in which the credit union is primarily identified as a cooperative financial business; and one in which the credit union is primarily a vehicle for community development and empowerment. However the FSA states that most credit unions combine aspects of both concepts to differing extents[17]. The FSA operates two versions of deposit-taking regulation in GB. Version 1 is considered a 'lighter touch where credit unions are restricted in the amount of money lent and the length of the repayment period. There are also greater restrictions on investment and borrowing opportunities. Under Version 2 credit unions are able to provide larger loans over longer periods, can offer variable dividend savings and can borrow and invest over longer periods than under Version 1. Under Version 1 supervision by the FSA is mainly desk based with occasional visits. Under Version 2 there are enhanced reporting requirements linked to a risk-based approach to supervision[18].

23. In RoI the rules mirror those for Northern Ireland with the following three additions:

(e) the education of its members in their economic, social and cultural well-being as members of the community;

(f) the improvement of the well-being and spirit of the members community; and

(g) subject to section 48 of the Act, the provision to its members of such additional services as are for their mutual benefit.

24. Regulation in RoI is by the Registrar of Credit Unions under the Financial Regulator. They operate primarily under the Credit Union Act, 1997 (as amended) which allows the Registrar to authorise the provision of additional services by credit unions where such services are of mutual benefit to its members. This has enabled credit unions in RoI to offer services such as mortgage intermediary services, insurance services, ATMs, Bureau de Change, money transmission service, financial counselling and savings stamps.

25. The ILCU has provided a comparison (Table 2) of the services which can be offered by credit unions here, in GB and in RoI.

Table 2. - Comparison of the services provided by credit unions in NI, GB and RoI

Activity |

NI |

GB |

RoI |

|---|---|---|---|

Deposit Taking |

X |

EF83BC |

EF83BC |

Insurance Services |

X |

EF83BC |

EF83BC |

Transfer of Securities |

X |

EF83BC |

EF83BC |

Access to Government Funding |

X |

EF83BC |

X |

Group/Society Membership* |

X |

X |

EF83BC |

Participation in Government Saving Initiatives |

X |

EF83BC |

EF83BC |

Unrestricted in the Business of Banking |

X |

EF83BC |

EF83BC |

Obligation to Pay Corporation Tax on Income |

EF83BC |

EF83BC |

X |

* This issue is being considered in the current review of GB legislation |

|||

26. As stated above, credit union membership in Northern Ireland is restricted to those who meet a 'common bond. In Northern Ireland 85% of credit unions have a common bond of residing or being employed in a particular locality. Other examples of common bonds are by membership of an association or by employment. The Consumer Council would like to see a review of the 'common bond principle. It states that the current rigid controls have an adverse affect on consumers and calls for more flexibility[19]. The Deregulation (Credit Unions) Order 1996 extended the notion of 'common bond in GB.

Role and Contribution of Credit Unions in Promoting Financial Well-being

27. In Great Britain, the Financial Inclusion Taskforce sees the role of credit unions in promoting financial well-being as being very significant. Credit Unions support Government savings schemes such as Child Trust Funds and ISAs. They improve access to financial services for low income and vulnerable groups and play an important role in increasing financial inclusion. Credit unions are considered a vital source of credit and secure banking for many people on low incomes.

28. HM Treasury sees credit unions in GB as making a significant contribution to the promotion of financial well-being through supporting various Government, tax-privileged savings schemes such as the Child Trust Fund and ISAs. Treasury states that[20]:

credit unions help to increase access to financial services that meet the needs of low income and vulnerable groups and play a key role in increasing financial inclusion. They can be a vital source of affordable credit for many people on low incomes, as well as providing opportunities to bank and save securely."

29. In Northern Ireland, DETI states that membership of credit unions represents a population penetration level of 50% compared to a level of less than 2% in GB. It states that in 2006 a total of £180k was contributed to social, cultural or charitable causes by 38 credit unions[21].

30. The UFCU is concerned that existing legislative restrictions on credit unions are preventing them from investing in the wider development of communities[22]. Both Larne Credit Union[23] and Derry Credit Union draw the Committees attention to the role of credit unions in providing employment in local communities. Derry Credit Union state that they currently employ over 50 staff[24]. All key stakeholders in Northern Ireland are agreed on the invaluable work undertaken by credit unions in promoting financial well-being, particularly in isolated and disadvantaged communities.

31. The Consumer Council sees credit unions in Northern Ireland as having a role to play in encouraging savings and providing an affordable alternative to 'doorstep credit for those who may otherwise be financially excluded. This is considered particularly important as more Northern Ireland households are financially excluded compared to GB[25]. Larne Credit Union reflects the frustrations of the credit union movement here when, in their written submission to the Inquiry, they state that their plans for expansion:

"have been adversely affected by our non-relationship with the FSA and the limited powers of the NI Registrar[26]."

32. Advice NI do, however bring a note of caution to the discussion stating that credit unions must not get into a position whereby interest charges increase to levels similar to or higher than that of banks. They state that the majority of credit unions in Northern Ireland do not freeze interest on loans for members having difficulty making loan repayments and call for changes to this policy. Advice NI also cites, what it calls, instances of 'irresponsible lending by credit unions and of inappropriate collection practices. Advice NI goes on to state that credit unions should provide members who are in financial difficulties with free independent debt advice and should support them through their difficulties[27]. In this regard Citizens Advice would like to see an agreed Code of Practice for all Credit Unions covering all aspects of their business[28].

33. The Committee recognises the unique contribution that credit unions make to tackling financial exclusion through the provision and promotion of services in areas where members of communities may otherwise find it impossible to avail of any financial services. In the course of this Inquiry, committee members have been impressed by evidence of the close links between credit unions and the communities they serve.

Legal and Regulatory Barriers Faced by Credit Unions in Northern Ireland

34. The main legislative barrier faced by credit unions seeking to expand their range of services is summarised by the FSA in their written submission to the Committee[29]. The FSA considers that current legislation in GB is hampering the development of credit unions there but states that it does not appear to be quite as disadvantageous as the situation is in Northern Ireland. In July 2002 Credit unions in GB were brought under FSMA. As credit unions in Northern Ireland are regulated by DETI Companies Registry, their registration and supervision comes exclusively under Northern Ireland legislation; the FSA has no jurisdiction over the deposit-taking activities of credit unions here. Credit union legislation in Northern Ireland is underpinned by the Northern Ireland Act 1998 where reference to the Credit Unions (Northern Ireland) Order 1985 renders the registration and monitoring of credit unions in Northern Ireland a devolved matter.

35. Under current arrangements credit unions in Northern Ireland cannot participate in FSA regulated activities which come under the scope of FSMA. The scope of FSMA has recently widened to include activities such as mortgage lending and broking and general insurance broking. The FSA considers that the problem can only worsen for Northern Ireland credit unions as and when other financial services become regulated activities under FSMA. The FSA believes that any move by credit unions here to become involved in activities such as insurance broking or mortgage lending should come under FSA regulation. It would not, therefore be possible as it would overlap and possibly conflict with existing arrangements in Northern Ireland. This is an important point. What it means in reality is that the Northern Ireland Assembly does not have the authority to legislate for financial services which come under the scope of FSMA and which are currently regulated by the FSA[30]. The Committee has not, therefore, been able to consider options that would result in the making of legislation in Northern Ireland in order to allow for the widening of activities and services by credit unions.

36. Both the UFCU[31] and the ILCU[32] refer to Article 24 of the Credit Unions (Northern Ireland) Order 1985. Article 24 expressly prohibits credit unions in Northern Ireland from participating in the business of banking. Both bodies consider this to be totally inappropriate. It is stated that recent changes to legislation in both GB and RoI have removed this restriction in these jurisdictions and both the UFCU and ILCU believe restrictions should also be removed here.

37. The Committee commissioned research into HM Treasurys consultation document 'Proposals for a legislative Reform Order for Credit Unions and Industrial Societies in Great Britain. The research paper is included at Appendix 7 page 299. Treasury states that current legislation is not conducive to the running of modern organisations, placing unnecessary restrictions on the operation of credit unions which inhibit their effectiveness. Proposals are intended to create a pathway for the modernisation of the credit union movement in GB. Eight proposals are put forward to reduce the burden on credit unions. These are:

- Proposal B1: Replace the common bond" requirement for credit unions with a field of membership" test. Amendment of the legislation to replace the common bond will, it is believed, lessen financial costs and administrative inconvenience, as well as removing obstacles to efficiency, productivity, and profitability.

- Proposal B2: Reform the requirements relating to membership qualifications and rename them common bonds". The amendments under this proposal will remove the limits enforced upon membership qualifications, which are deemed to be detrimental to productivity, innovation, mergers, and efficient administration.

- Proposal B3: Reform the restrictions on non-qualifying members of credit unions. This proposal will remove the 10 percent limit on the number of non-qualifying members, allowing credit unions to set their own limits in this area, improving productivity and profitability.

- Proposal B4: Allow credit unions to admit bodies corporate, unincorporated associations or partnerships to membership. Amending the legislation in this area will bring economic and social benefits to corporate/unincorporated bodies, credit union and their members. The current legislation also negatively affects the profitability of the credit union and the long-term stability of its balance sheet. This proposal will also introduce interest bearing shares, to be issued to corporate bodies only.

- Proposal B5: Allow credit unions to offer interest on deposits, provided certain requirements are met. A credit unions inability to offer interest on deposits limits their ability to attract members. This is deemed to constitute an obstacle to productivity and profitability.

- Proposal B6: Abolish the 8 per cent per annum limit on dividends. This proposal is designed to bring parity with banks and building societies.

- Proposal B7: Repeal the attachment" requirement, which restricts withdrawal of shares. As above, this proposal is designed to bring parity with banks and building societies.

- Proposal B8: Allow credit unions to charge the market rate for providing ancillary services to their members. Again, this proposal is designed to bring parity with banks and building societies.

Availability of public funding to credit unions in GB, Northern Ireland and RoI

38. From 2006 to 2011 the Government is investing £80 million as a growth fund for credit unions and other not-for-profit lenders in England, Scotland and Wales. This has supported more than 100 lenders and to date, more than 70,000 affordable loans have been made to financially excluded clients[33].

39. Credit unions in RoI have not received any public funding to date, however they are exempt from the payment of corporation tax on income. Corporation tax in RoI is currently 12.5%.

40. Credit unions in Northern Ireland have received no public funding to date. Credit unions here are liable to corporation tax on revenue generated from investments at a rate of 19%. The ILCU states that League affiliated credit unions in Northern Ireland had contributed £3.3 million to the Exchequer in corporation tax to year-end September 2007[34]. Concern was also expressed in the course of the Inquiry that, in addition to having to pay corporation tax, credit unions are charged rates on their premises and are liable for water and refuse collection charges[35]. Both Larne Credit Union[36] and Slemish n tha Braid Credit Union[37] highlight the issue of Corporation Tax, while Derry Credit Unions written submission[38] draws attention to the fact that some credit unions pay rates while others (for example, those operating out of church halls) are not required to pay rates.

Policy development and practices that have taken place since the Review of Credit Unions in GB

41. Since the Review of credit unions, some changes have been made to develop the services provided by credit unions here. This has included approval by the Registrar for social security benefits and pensions to be paid directly into credit union accounts. Credit union members may now also repay loans and make share lodgements via Pay Point.

42. Following the collapse of Farepak, approval was given for a special category of account in credit unions which permits savings for special occasions. These accounts are not considered when deciding the eligibility criteria for loans and the savings are eligible for dividend payments.

43. The Registrar has supported the ILCU in a debit card scheme which enables members to withdraw cash at ATM and to set up direct debits and standing orders to pay regular bills[39].

44. The ILCU sees it as significant that a number of its member credit unions have begun to engage in these activities. It states that it is:

"a clear indication of the willingness and enthusiasm that exists at credit union level to develop and improve the credit union service. The Registrar has encouraged the widespread adoption of the services by credit unions subject to appropriate controls being in place."

45. Following the successful piloting of the 'Saving Gateway in GB, the scheme will be introduced on a UK-wide basis from 2010. The Savings Gateway is a cash savings account providing an incentive to save for people on lower incomes. The Government matches (pound for pound) the money deposited into the account[40].

Assessment of the Treasury Select Committee recommendations on credit unions

46. The Twelfth Report of the Treasury Select Committee acknowledges that credit unions in Northern Ireland are well developed and play an important role in promoting financial inclusion and access to affordable credit. It confirms that the current regulatory regime in Northern Ireland is preventing credit unions from expanding into other areas and recommends that Government take action to ensure that the regulatory regime supports expansion. The Report also notes that Northern Ireland credit unions have been unable to apply for Government support through the Growth Fund. It goes on to recommend that Government and the Northern Ireland Executive consider the most appropriate ways to provide Government funding and support[41].

Potential to broaden the range of services offered by credit unions

47. The broadening of the range of services offered by credit unions is supported by all key stakeholders to varying degrees and is encouraged or even considered essential by many. The FSA states that credit unions being able to offer a wider range of services would attract those sections of the population that do not normally interact with financial institutions and sees clear benefits for the consumer[42]. This is supported by UFCU who state that credit unions are constrained by the fact that they must provide services to people who would not be welcome at banks[43]. The ILCU is critical of the fact that credit unions here cannot participate in Government savings initiatives unlike those in GB and RoI. The reason is that as they are not regulated by the FSA under FSMA, credit unions are not covered by the Financial Services Compensation Scheme. This is despite the fact that both the ILCU and UFCU have their own schemes to cover members savings. It is seen as key to the future of credit unions in their role in promoting financial well-being and tackling financial exclusion that those who are excluded from other means of banking can avail of these services through credit unions. The Committee firmly believes that credit unions in Northern Ireland should be able to provide the same range of services that those in GB can offer including current accounts, internet and telephone banking, electronic transfer of wages, ATMs, insurance, debit cards, mortgage, bill payment, direct debit, standing orders and junior savings accounts. Committee members are in agreement that a solution must be found which enables credit unions to provide these services in the very near future and with the minimum of disruption to credit unions or their members.

48. A prime example of where credit unions have the potential to make a significant, long-term and lasting impact is in the area of the Child Trust Fund. The Child Trust Fund is part of the Governments strategy for saving and asset ownership. Introduced in April 2005, it is a long-term savings and investment account for children, which aims to ensure that all children have funds available to them when they reach the age of 18. Under the Fund, all children born since 1st September 2002 receive a Government payment of at least £250 as an initial endowment and children from low-income families receive a further £250. Parents and family may make further contributions and a further £250 contribution is made by Government at age 7 (£500 for low-income families). Vouchers are issued automatically following the first claim for Child Benefit and if an account is not opened within 12 months the Revenue and Customs will open a stakeholder account on the childs behalf. The problem in Northern Ireland, as highlighted by both the ILCU and the UFCU, is that Northern Ireland has the lowest percentage uptake on Child Trust Funds in the UK. This is probably not surprising considering that six percent of households in Northern Ireland have no savings or bank account compared to a UK average of three percent[44]. The Consumer Council estimates that there are £11 million of unopened Child Trust Fund payments here[45] and believes that amending the law to allow credit unions to provide additional services would help increase financial inclusion. Table 3 outlines statistics provided by ILCU for Child Trust Fund uptake across the UK at January 2007.

Table 3. - Child Trust Fund uptake by UK Region at January 2007

Region |

Percentage Child Trust Fund Uptake |

|---|---|

England |

71.5 |

Wales |

69.8 |

Scotland |

65.8 |

Northern Ireland |

63.3 |

49. Although children here are not missing out directly on Government payments due to the fact that Revenue and Customs open a stakeholder account, the intended culture of the scheme is being missed by many families who are not able to, or remain unaware of, the whole ethos of savings and investments and the objectives of the scheme. An opportunity is being missed to attract people who are financially excluded and to prevent another generation from being similarly excluded.

50. The Financial Inclusion Taskforce states that few credit unions in GB have taken up the option of administering Child Trust Fund Vouchers but that those that had have found it very useful and new members have been encouraged[46]. The British Bankers Association (BBA) does not foresee any problems with credit unions being given appropriate powers to take on the role, but are not convinced that increased supply will trigger increased demand[47]. The BBA has however, only recently taken over as the representative body of the banks in Northern Ireland and is not familiar with the size and influence of the credit union movement here. The Committee considers it likely that, given the maturity of the movement in Northern Ireland and, with appropriate support from Government, if credit unions here were in a position to administer Child Trust Fund Vouchers, uptake would increase significantly with a further positive long-term impact on financial inclusion.

51. The ILCU sees it as important that credit unions be allowed to become involved in reinvestment of assets into community development and community enterprise initiatives. In their written submission s to the Inquiry, both Dundonald Credit Union[48] and No.5 Credit Union[49] support this viewpoint. The Committee supports the investment of funds by credit unions into social economy enterprises but also notes the concerns of other stakeholders in this regard. The BBA states that:

"The longer-term investment of assets is quite a different skill set from the provision of retail financial services, and the Committee should reassure itself that the credit union sector has sufficient skills in that sphere ... It would be a challenge in some areas to match the longer-term yield from such investment to the shorter-term demand for interest on savings"[50]

52. The BBA states that it would not suggest that credit unions should stay out of that area but cautions that such an expansion would move credit unions into a field that would require sophisticated financial services and competences. The FSA agrees with this stating that:

"Any extension by a regulated institution to invest in something that it has not traditionally invested in requires an increase in financial understanding and particularly in understanding of the financial risks[51]"

53. The FSA goes on to state that there are some 'non-trivial financial risks in this type of investing.

54. Credit union membership is currently open only to individuals and only to individuals who meet the 'common bond principle. It is also the case in GB that only individuals may be members of credit unions, therefore, as stated by DETI[52], in this regard GB and Northern Ireland credit unions are on an equal footing. DETI goes on to state that corporate membership is being considered as part of a Treasury review of cooperative legislation in GB and it intends to consider the implications for credit unions in Northern Ireland of any proposed changes in GB. Both the ILCU[53] and UFCU[54] believe that this needs to be changed. At present, a husband and wife cannot open a joint account in a credit union and neither can a community group or society. The ILCU further confirmed that there is support in the community from organisations seeking group membership of credit unions[55]. This view is widely supported in written submissions to the Committee from individual credit unions including Shaftesbury Credit Union, which states that credit union legislation should be amended to permit group and society membership[56]. Orchard Credit Union states that, as a result of credit unions not being able to provide joint accounts or other types of corporate accounts:

"community groups are driven into the clutches of commercial banks and have to suffer excessive bank charges"[57]

55. ABCUL sees benefit in grant funded community groups being allowed to open accounts in credit unions, stating that:

"Not only is a service provided with the grant, but the money that is deposited in a credit union is lent out to be used in the community meanwhile. For example, local authorities giving grants to local organisations can see the benefits twofold"[58]

56. Overall, the Committee found very little opposition to the idea that credit unions should be allowed to expand their range of services and, indeed found considerable support from some unlikely sources. The BBA states that it can see no challenges or difficulties in allowing groups to open accounts in credit unions[59]. The Committee fully supports the idea that couples, groups and societies should be allowed to open accounts in credit unions.

57. The BBA states that in GB, where credit unions are already in a position to offer a wider range of services, banks do not view credit unions as a direct competitor[60] and that in GB the banks look to support credit unions[61]. DETI is keen to see an expansion of the range of services which credit unions can offer and has worked closely with the Committee during this Inquiry to ensure that the Committee has the information it needs. Indeed the Registrar has, as stated earlier, taken steps within its own remit to assist the expansion of credit union services with the direct payment of benefits, use of Pay Point and budget accounts. The Consumer Council and the advice sector are keen to see an expansion of credit union services although some caution is expressed to ensure that the scenario is avoided where credit unions become like high street banks.

58. Key stakeholders agree that the current regulatory regime is hampering the development of the credit union movement in Northern Ireland and causing missed opportunities to tackle financial exclusion. A variety of suggestions have been put forward by various stakeholders in order to tackle the problem. The Committee has considered the main suggestions in the form of options and has undertaken an appraisal of each option.

Options for Change

Overview of Options

59. In any review where options are being considered the first option to consider is to maintain the status quo or the 'do nothing option. Given the breadth and depth of support for change and expansion of credit union services and the benefits that this can bring to communities and individuals, doing nothing is not considered a viable option in this case.

60. The restrictions on credit unions and their inability to expand their services are rooted in the way in which they are regulated. Therefore options must seek to change the way in which credit unions are regulated in order to bring about the considerable changes which key stakeholders would like to see in place.

61. As stated previously, the Committee has not been able to consider options that would result in the making of legislation in Northern Ireland in order to allow for the widening of activities and services by credit unions as such activities come under the remit of the FSA. Options have therefore been considered which include the FSA to a greater or lesser extent in the regulation of credit unions in Northern Ireland. All of the options considered allow for the registration of credit unions to remain within DETI Companies Registry.

62. The preferred option must be able to deliver for credit unions, a full expansion of services including current accounts, internet and telephone banking, electronic transfer of wages, ATMs, insurance, debit cards, mortgage, bill payment, direct debit, standing orders, junior savings accounts and Government schemes such as the Child Trust Fund scheme and ISAs, in line with what is currently available in GB. The preferred option must also enable credit unions in Northern Ireland to quickly and easily take advantage of any further expansion of services in GB such as group or corporate membership.

63. Four main options have been put forward to achieve this goal. These are:

Option 1 - FSA regulatory powers delegated to DETI

Option 2 - Dual regulation shared between FSA and DETI

Option 3 - Formation, by credit unions, of a registered company through which expanded range of services is provided

Option 4 - Retention of all credit union registration within DETI Companies Registry and transfer of all credit union regultation to the FSA

64. The Departmental Solicitors Office has advised DETI that an amendment to the Northern Ireland Act 1998 would not be required in order to implement any of these options. However, a legislative consent motion would be required[62].

65. A brief explanation of each option is provided below:

Option 1 - FSA regulatory powers delegated to DETI

66. The adoption of this option would mean that HM Treasury would have to give permission for the FSA regulatory powers to be delegated to DETI Companies Registry. Under this option, DETI Companies Registry would remain the sole authority regulating credit unions in Northern Ireland, but would do so under the terms of the FSMA rather than under the Credit Unions (Northern Ireland) Order 1985.

Option 2 - Dual regulation shared between FSA and DETI

67. Under this option, credit unions that wish to provide a broader range of services, including services currently regulated by the FSA would be regulated by the FSA under the FSMA. Those who do not wish to expand their range of services would continue to be regulated by DETI Companies Registry as they are at present under the Credit Unions (Northern Ireland) Order 1985.

Option 3 - Formation, by credit unions, of a registered company through which expanded range of services is provided

68. This option was put forward by DETI in its written submission to the Inquiry[63]. It proposes that, on behalf of their affiliates, each of the sponsor bodies (ILCU and UFCU) form a separate legal entity under company law to undertake FSA regulated activities on behalf of their membership. Each credit union that wished, would in effect, become a customer of this separate company. Credit unions would still be regulated by DETI Companies Registry under the Credit Unions (Northern Ireland) Order 1985, however the separate company, offering services across a number of credit unions, would be regulated by the FSA under the FSMA.

Option 4 - Transfer of regulation of credit unions entirely to the FSA

69. This option would remove DETI Companies Registry from the regulation of credit unions in Northern Ireland. All credit unions would move to FSA regulation. Depending on the services which credit unions wish to provide, they would apply to the FSA for either Version 1 or Version 2 regulation.

Option Appraisal

Option 1 - FSA regulatory powers delegated to DETI

70. If implemented, this option would require every credit union in Northern Ireland to apply to DETI Companies Registry for either Version 1 or Version 2 of FSA regulation. It would enable credit unions that wished, to expand their range of services to fully embrace all of the services which credit unions in GB can offer. Furthermore, it would enable credit unions to further expand their range of services as and when GB legislation allowed this to happen. Credit unions here would be able to maintain their close working relationship with DETI Companies Registry while availing of the benefits currently enjoyed by credit unions in GB.

71. In DETIs view Option 1 would require amendment to both the Credits Unions (Northern Ireland) Order 1985 and the FSMA. Time scales for implementation of this option would be dictated by when Assembly time could be secured for an amending Bill and, following agreement by HM Treasury, time in Westminster would have to be secured for an affirmative resolution Order to be approved by each House of Parliament[64].

72. This option was supported by both the ILCU and UFCU. The ILCU considers this option 'workable[65] and feels that it is important that the Committee consider options whereby regulation is shared between DETI and the FSA. They state that this would be their preferred option[66]. On expanding the range of services which credit unions here can offer, the UFCU state that:

"Registry would do well to acquire regulatory powers from Westminster to extend its ability to include those matters. That would be a more acceptable scenario to the UFCU as it has an established professional relationship with local registry staff[67]."

73. The British Bankers Association felt that this option could be explored, provided different regimes are co-ordinated so that the system does not result in credit unions having an unfair advantage. The FSA are, however, wholly opposed to this option, stating that:

"We are not keen on - in fact, we would be opposed to - the middle way that would involve sharing or delegating responsibility"[68]

74. The Committee believes that, given appropriate support, this option could be made to work, however, it recognises the wholehearted opposition expressed by the FSA. In addition, there are indications that HM Treasury share the FSA view[69] and DETI has not expressed support for this option. They state that this option could have staff resource implications for the Department in terms of skills and competence to carry out its responsibilities[70]. This option has the advantage of providing full coverage under the Financial Services Compensation Scheme (FSCS), however this would come at a cost to individual credit unions in the payment of levies to the FSA. It also provides the advantage that the current regulator is retained, as is the close working relationship that credit unions have with the regulator. The Committee sees this as a distinct advantage, especially at a time when credit unions would have to come to terms with new systems of regulation and with the provision of new and, perhaps, more complex services.

Option 2 - Dual regulation shared between FSA and DETI

75. This option would require credit unions wishing to expand their range of services, to apply to the FSA to be regulated by them under Version 2. It would enable only those credit unions regulated by the FSA, to expand their range of services to fully embrace all of the services which credit unions in GB can offer. These credit unions would be in a position to further expand their range of services as and when GB legislation allowed this to happen. These credit unions would no longer have a relationship with DETI Companies Registry as they would come wholly under FSA regulation. Credit unions not wishing to expand their range of services would continue to be regulated by DETI Companies Registry and would not have a relationship with the FSA.

76. In order to implement Option 2, DETIs understanding is that no legislative changes would be required. However, any application would have to be approved by the FSA and further applications to the FSA for credit unions who wish to expand their range of services[71].

77. The ILCU would consider this their secondary option but believes that it would not be ideal for any stakeholders[72]. The UFCU is wholly opposed to this option as it believes that smaller, rural credit unions would be seen as less important[73]. As with Option 1, the FSA are, for similar reasons, opposed to this option. They state that they are not in favour of sharing or dividing responsibility between the FSA and DETI[74]. They further state that it would send out a confusing message and may lead to competitive inequality within the market in Northern Ireland[75]. DETI shares the concerns of the FSA stating that it is, fraught with danger[76]", but would consider some sort of memorandum of understanding or inter-agency agreement which allowed less complex credit unions to be regulated by DETI and larger credit unions to be regulated by the FSA[77].

78. The Committee is not opposed to this option but recognises and understands the reservations of the UFCU and ILCU and can understand how, as stated by the FSA, it could send out a confusing message to consumers. The Committee also considers it highly unlikely that approval would be gained for any application by a credit union, or credit unions, to be regulated the FSA.

Option 3 - Formation, by credit unions, of a registered company through which expanded range of services is provided

79. Under this option, all credit unions would continue to be regulated by DETI Companies Registry. Those that wish, could provide a fully expanded range of financial services through a central company which would be regulated by the FSA.

80. DETI believes that no legislative changes would be required to put Option 3 into operation. The time scale would be three working days from receipt of a properly completed application to DETI Companies Registry, followed by the time required for the FSA to approve an application. DETI points out that, under this option, Northern Ireland credit unions would not have access to the FSCS.[78]

81. As stated above, this option was proposed by DETI. It gains some support from the FSA which believes that adopting this option should not pose a problem in relation to the FSMA, although the FSA believes that some difficult legal work may need to be carried out so that the FSA-regulated activities carried out by the 'company are seen as distinct from the core credit union services. The FSA goes on to state that, if credit unions wanted to adopt this option the FSA would work constructively with them[79]. The BBA agrees that there are governance issues which would have to be explored with this option[80].

82. UFCU may have considered this option[81] but have come out against it. They believe that it could cause confusion for customers who may not understand why one credit union could offer additional services while another could not. They feel that it would be unfair to allow some credit unions to join forces to form a conglomerate[82]. They also feel that it was adding an additional, unnecessary tier to the credit union movement[83]. The ILCU was wholly opposed to this option, stating that:

"We see no advantage in that: the associated costs would far outweigh the advantages it might bring. The company would have to be set up in such a way that it would have its own staff. Extra staff would therefore have to be provided; and that situation would duplicate what the banks are doing.

Volunteers would also be at a disadvantage, because they would not be able to run the company. Therefore, professionals would be required to run the company on a day-to-day basis[84]."

83. The ILCU also feel that, as it was not necessary for credit unions in GB or RoI to go down this route, neither should it be necessary for credit unions in Northern Ireland[85].

84. The Committee recognises the legal and logistical difficulties which the adoption of this option would create. It is also clear that there is not a lot of support for the option. Furthermore, as stated by the ILCU[86] and by DETI[87], only those services regulated by the FSA would be covered by the FSCS. Any company established under this option would have to pay levies to the FSCS and individual credit unions would still be required to be part of ILCUs and UFCUs share protection schemes.

Option 4 - Retention of all credit union registration within DETI Companies Registry and transfer of all credit union regultation to the FSA

85. Under this option, all responsibility for the regulation of credit unions would transfer from DETI Companies Registry to the FSA. All Northern Ireland credit unions would come under the FSMA.

86. As with Option 1, DETIs understanding of this option is that it would require amendment to both the Credits Unions (Northern Ireland) Order 1985 and the FSMA. Again, time in both the Assembly and Westminster would be required to put this option into operation[88]. DETI goes on to state that, if the Executive and HM Treasury were to agree to this option and the FSA were to exercise policy and regulatory responsibility for credit unions registered in Northern Ireland:

"future legislative changes would apply automatically and simultaneously in Northern Ireland and in GB. NI credit Unions would need to meet FSA requirements to be authorised to operate, which would also bring with it the protection of the Financial Services Compensation Scheme."

87. Although it is not their preferred option, the UFCU state that, as long as the FSA looks after credit unions as well as DETI Companies Registry have done it should not be a problem. They state that it would be successful:

"as long as the customer - the wee man at the end of the street - has a credit union system that he can be proud of[89]."

88. The ILCU feel that the FSA is not justified in its reluctance to delegate responsibility for regulation under the FSMA to DETI Companies Registry[90]. The ILCU does not believe it is necessary for Northern Ireland credit unions to be regulated by the FSA in order to be able to offer a full range of services, stating that:

"The FSAs true position is that it will not oppose change as long as it takes the form of a complete shift of all credit unions in the Province from DETI to the FSA. That is entirely contrary to the intention of the Northern Ireland Act 1998, which was - and remains - that credit unions are a devolved matter to be dealt with by this Assembly[91]"

89. The ILCU does, however recognise that whatever outcome is agreed, the result must be that credit unions in Northern Ireland must be in a position to offer a wider range of services. They state that:

"There must be a positive recommendation that will allow credit unions in Northern Ireland to extend the range of services they can offer[92]."

90. If Option 4 is the only option, the ILCU state that they do not have a mandate from their membership to accept this option. They state:

"It will be up to us to persuade our members, if it comes to the point that that is the only option[93]."

91. ABCUL represents the interests of the majority of credit unions in GB. Their members are currently regulated by the FSA. They believe that FSA regulation works well and is not difficult to operate[94]. They state that FSA regulation is:

"one of the best things that has happened to credit unions in Britain[95]."

92. In relation to the challenges which FSA regulation brought with it, ABCUL states that the FSA has an individual relationship with each credit union. It recognises that there was a real challenge concerning the degree of face-to-face supervision and regulatory visits versus desktop supervision but goes on to state that:

"A good balance has now been reached, and quite innovative things have been done to get round some of those challenges. By and large, that relationship has been a good experience[96]."

93. The BBA supports this view, stating that:

The FSAs regulatory model - or CRED, the credit unions sourcebook - is not as onerous as some might think[97]."

94. In relation to Option 4, the BBA have expressed strong views in support. In their written submission to the Committee they state that:

Offering more complex banking services does require a robust infrastructure to support business activity. To achieve the desired level of consistency, it is suggested that all UK financial services providers should be regulated by the same body, and accordingly that credit unions in NI should be subject to the prudential supervision and consumer protection requirements of the FSA (in common with their GB counterparts, and as is already the case for banks in NI). A common supervisor would also allow credit unions to apply to extend their services and products on an individual basis, without the imposition of a one-size-fits-all solution which, in some cases, may be inappropriate[98]."

95. The FSA states that it is not seeking to take over regulation of credit unions in Northern Ireland but would not turn down the opportunity if it arose[99]. That stated, it is clear that the only other option which the FSA would support is Option 3, which does not receive support from other key stakeholders.

96. It is unclear why the ILCU is so opposed to this option to the extent that it is. The Committee recognises that this option is not preferred by the credit union movement here, which would have to come to terms with changes in the way credit unions are regulated and with changes to the personalities involved in regulation. Given the level of support expressed by ABCUL for FSA regulation, the Committee believes that, subject to a well supported settling in period, this option would succeed. The Committee does however, have some concerns in relation to this option. The Committees main concern is, that, given the number and size of credit unions in Northern Ireland, coupled with the close working relationship the movement has developed and maintains with DETI Companies Registry, the fact that FSA does not have a presence in Northern Ireland would pose real difficulties for credit unions here. The FSA has its headquarters in London and has a small office in Edinburgh. It states that it has no plans to, and will give no commitment to changing that arrangement[100]. Credit unions would have to come to terms with a completely new regulatory regime and, in addition, many would have to come to terms with the development and delivery of a whole new range of services. The complete withdrawal of current levels of support at a time of increased need would create major difficulties for credit unions. The Committee believes that, for this option to succeed, it would be necessary for credit unions to very quickly foster close working relationships with the FSA.

Conclusions

Expansion of the Range of Services which Credit Unions May Offer

97. The Committee believes that the credit union movement has a vital and increasingly important role in providing essential financial services to individuals and communities, many of which would otherwise be financially excluded. Credit unions have a unique role in promoting, maintaining and increasing financial inclusion in disadvantaged communities in Northern Ireland. For this reason, the Committee considers it essential and recommends that credit unions are permitted to expand their range of services to include, at the very least, those services which credit unions in GB can currently offer (Recommendation 1). The Committee also considers it essential that, in order to maximise the benefits that such an expansion can bring, change must happen as quickly as possible in order to allow credit unions and their members to take advantage of additional services without undue delay.

Preferred Option